Commercial property insurance protects your business from big disasters. It keeps your physical stuff safe from things that could ruin your business fast. Did you know a big problem could take away all your hard work in no time?

Every day, over 200 American businesses face fires. Stores lose about $62,360 on average, and offices lose around $27,027.

“Insurance doesn’t cost—it pays,” my mentor used to say. After helping Idaho Falls business owners for ten years, I see how it saves them from big losses.

Commercial property insurance acts as a shield against theft, natural disasters, and accidents. It’s key for any business with lots of stuff. Without it, one big loss could hurt your business a lot.

Commercial property insurance provides financial indemnity for direct physical loss or damage to buildings, tenant improvements, and business personal property arising from insured perils such as fire, theft, vandalism, and specified weather events. Coverage is structured under either named-peril or all-risk forms, with valuation options of replacement cost, actual cash value, or agreed value; coinsurance clauses (typically 80–100 % of current replacement cost) impose proportional penalties when limits are inadequate, making periodic professional appraisals essential to maintain full recovery capacity.

Premium determination is driven by location-related hazards (fire protection class, crime index, catastrophe zone), construction characteristics (age, materials, fire-resistance rating), loss-history severity and frequency, and installed protective systems (sprinklers, alarms, security monitoring). Risk mitigation credits of 5–15 % per system are available; conversely, underinsurance or adverse loss experience can trigger surcharges or coverage restrictions. Claims require prompt notification, comprehensive photographic and documentary evidence, and substantiated repair estimates to ensure accurate settlement.

Quick hits:

- Guards against fire, theft, storm damage.

- Covers buildings, equipment, inventory items.

- Maintains business continuity after losses.

- Protects against liability claims too.

- Satisfies lender and lease requirements.

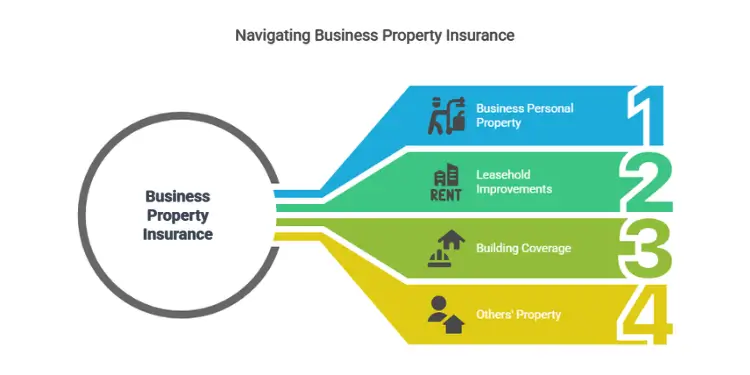

Coverage for buildings and business contents

Commercial property insurance protects your business. It covers the buildings and the things inside that keep your business running. I’ve helped Idaho Falls business owners for ten years. I know how important it is to understand what your policy covers.

When you buy commercial property insurance, you get two main protections. One is for your building and the other is for what’s inside. It’s important to know what each covers before you sign.

Building Ordinance or Law Coverage Importance

Standard policies cover your building as it is. But, if local codes have changed, you need special coverage. This is called building ordinance coverage.

I worked with a restaurant owner whose building was damaged by fire. The policy covered the repairs, but she had to pay $75,000 to meet current codes. This is why building ordinance coverage is so important.

This coverage helps with three big costs that regular policies don’t cover:

- The cost to demolish undamaged parts of your building.

- The loss of value from parts that must be demolished.

- The increased cost of construction to meet current codes.

Without this coverage, you could face big financial problems after damage. Most buildings over 10 years old don’t meet today’s codes. When you rebuild, you must bring everything up to code, not just the damaged parts.

Without ordinance or law coverage, you may bear the full cost of code-based repairs—especially critical in properties older than 10 years. Ref.: “IRS Commercial Property Ordinance Coverage Essentials (2025). Insurance Premium Factors.” [!]

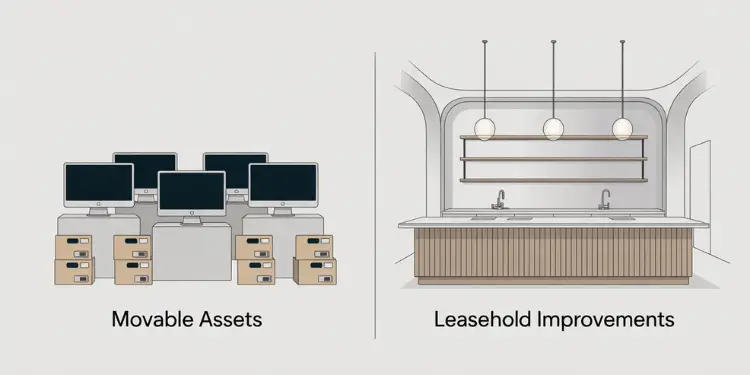

Business Personal Property Versus Improvements

Business personal property (BPP) includes things you’d take with you if you moved. This includes furniture, equipment, and even digital assets in some cases. Your insurance protects these items, whether they’re in your building, temporarily removed, or in transit.

Leasehold improvements are permanent changes you’ve made to a rented space. This could be custom lighting, built-in shelving, or special flooring. Even though these are part of the building, you’re usually responsible for insuring them if your lease says so.

The difference between movable property and improvements matters. While your computer equipment loses value quickly, custom cabinetry might keep its value or even go up in value.

| Coverage Type | What’s Protected | Special Considerations | Common Exclusions |

|---|---|---|---|

| Building Coverage | Structure, completed additions, permanently installed equipment, outdoor fixtures | Building ordinance coverage needed for code upgrades | Land, foundation, underground pipes |

| Business Personal Property | Furniture, inventory, equipment, electronics | Coverage extends to property temporarily off-premises | Vehicles, employee property, digital data (without endorsement) |

| Tenant Improvements | Custom installations, built-in fixtures, renovations | Responsibility determined by lease agreement | Improvements made without landlord permission |

| Others’ Property | Leased equipment, customer property in your care | Requires specific endorsement in most policies | Items covered by other insurance policies |

Remember, commercial property insurance doesn’t cover financial losses from business interruption. If a fire damages your building and equipment, your policy covers repairs and replacement. But it doesn’t cover lost income while you’re closed. For that, you need business interruption coverage as a separate endorsement or policy.

When you look at your policy, pay attention to how your insurer defines “building” versus “contents.” Some items, like window treatments or removable floor coverings, might be unclear. I suggest making a detailed inventory with photos of all your business property. This way, you can clearly see what’s considered building components versus business contents.

Read More:

Perils protected including fire theft vandalism

Commercial property insurance shields your business from many dangers. It’s key to know what your insurance protects against. This is as important as knowing what assets it covers.

There are two main types of commercial property insurance. “Named perils” lists specific dangers your policy covers. “All-risk” or “special form” policies cover all dangers, except those listed as not covered.

Named perils coverage protects against common threats like:

- Fire and smoke damage.

- Lightning strikes.

- Windstorm and hail.

- Explosion.

- Theft and vandalism.

- Vehicle damage (when someone crashes into your building).

- Sprinkler leakage.

- Sinkhole collapse.

- Volcanic action.

When theft happens, it’s not just about the stolen items. Your insurance also covers damage to your property. This includes broken windows or damaged locks.

“The difference between named perils and all-risk policies becomes most apparent when filing a claim. With named perils, the burden falls on the business owner to prove the damage resulted from a listed peril. With all-risk, the insurer must prove an exclusion applies.”

All-risk policies offer more protection but exclude some dangers. Most policies don’t cover:

- Flood damage.

- Earthquake damage.

- War and nuclear hazards.

- Normal wear and tear.

- Insect and vermin damage.

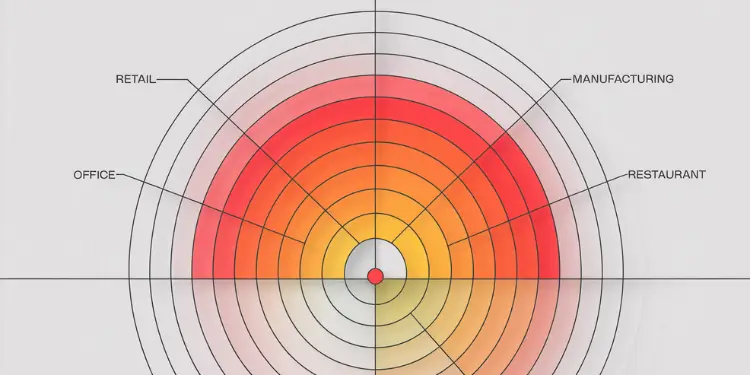

Different businesses face different dangers. Retailers worry about theft, while manufacturing facilities fear fire. Restaurants are concerned about fire and water damage.

| Business Type | Primary Peril Concerns | Secondary Peril Concerns | Recommended Coverage |

|---|---|---|---|

| Retail Store | Theft, Vandalism | Fire, Water Damage | All-Risk with Theft Endorsement |

| Office Building | Fire, Water Damage | Theft of Electronics | Named Perils with Technology Rider |

| Manufacturing | Fire, Explosion | Equipment Breakdown | All-Risk with Machinery Coverage |

| Restaurant | Fire, Smoke | Water Damage, Theft | All-Risk with Business Interruption |

When looking at your policy, check how theft coverage is explained. Some policies have limits or need certain security measures.

I tell clients to assess their peril risks carefully. This depends on their location, industry, and operations. A business in Florida needs different protection than one in Idaho. A warehouse storing electronics needs different theft protection than an office building.

Commercial property insurance works best when you know what’s covered and what’s not. This helps find gaps in coverage that might need extra policies or endorsements.

Policy valuation methods replacement versus actual

Commercial property insurance has two key ways to value your property. This can mean getting the full cost to replace it or a lower value based on its age. Knowing this can help your business bounce back faster after a loss.

When you file a claim, your insurance might pay in two ways. You might get the cost to replace your property or its actual cash value. It’s important to know which to avoid surprises.

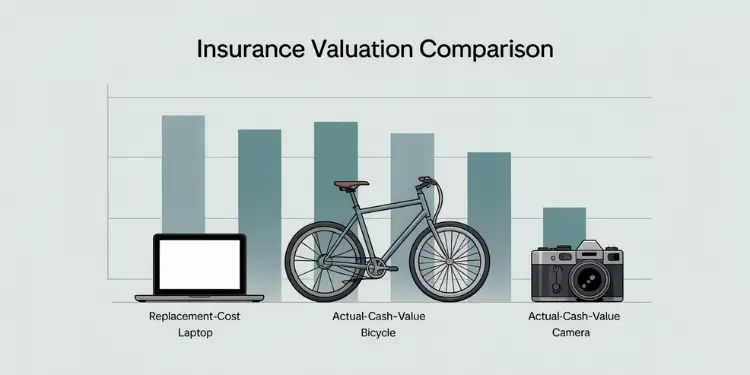

Replacement Cost Valuation

Replacement cost coverage means getting new items to replace what’s lost. This doesn’t count depreciation. So, if your old equipment is damaged, you get new ones.

For example, if a storm damages your store’s roof for $75,000, you get the full $75,000 (minus your deductible). This method protects you fully but costs more.

| Property Item | Age | Original Cost | Replacement Cost Payout |

|---|---|---|---|

| Office Furniture | 7 years | $12,000 | $15,000 |

| Computer Systems | 3 years | $25,000 | $28,000 |

| HVAC System | 10 years | $30,000 | $42,000 |

Actual Cash Value

Actual cash value (ACV) works differently. It calculates the cost to replace your property and then subtracts depreciation. This means you get a lower payment that reflects your property’s used value.

Using our roof example, if the $75,000 roof was 10 years old when damaged, an ACV policy might pay $25,000. The insurer figures you’ve used two-thirds of the roof’s life, so they deduct that from the replacement cost.

ACV policies cost less but might not cover all your costs. I’ve seen businesses need loans to cover the difference between what they got and what they needed.

Actual Cash Value (ACV) subtracts depreciation from replacement cost, often leaving policyholders under-funded after a loss. Ref.: “Hillock Insurance Agency (2025). What is a Coinsurance Clause? Hillockins.com.” [!]

Agreed Value Option Versus Coinsurance

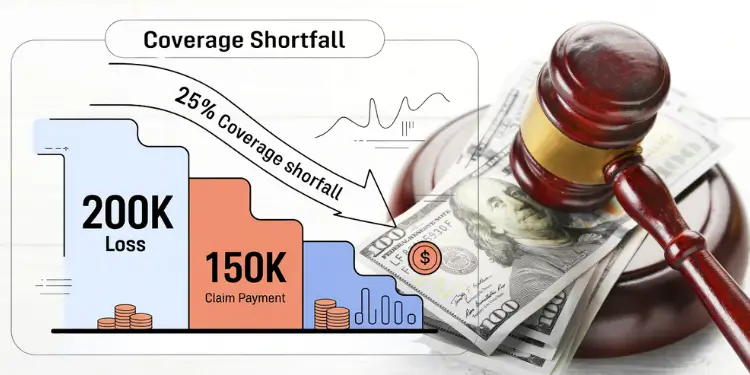

Commercial property policies also have coinsurance clauses. Coinsurance means you must insure your property for at least 80-90% of its value. If you don’t, you face penalties when filing a claim.

For example, if your building is worth $1,000,000 and you need 80% coverage, insure it for at least $800,000. If you only insure it for $600,000 and have a $100,000 loss, you’ll get less.

($600,000 ÷ $800,000) × $100,000 = $75,000

This means you’d get only $75,000 for your $100,000 loss. You didn’t meet the coinsurance requirement.

The agreed value option is an alternative. For more money, you can agree on a specific value for your property. The insurer promises to pay up to that amount without penalties.

This option gives you certainty about claim payments. It’s good for businesses with unique or hard-to-value assets, even if it costs more.

Choosing the Right Valuation Method

When picking a valuation method, think about a few things:

- Your financial ability to absorb partial losses.

- The age and condition of your business property.

- How quickly you would need to replace damaged items.

- Your budget for insurance premiums.

Most businesses choose replacement cost for full protection. But if your property is old and you plan to replace it soon, ACV might be better.

The agreed value option is best for businesses with special equipment or historic buildings. It’s worth the extra cost for the certainty it offers during claims.

Coinsurance requirements and penalty avoidance

Coinsurance clauses are a big deal in commercial property insurance. They can leave you with less protection than you think. It’s important to know about them to avoid big problems.

Coinsurance means you must insure your property for a certain percentage of its value. This is usually 80%, 90%, or 100%. It helps make sure you’re paying the right amount for your risk.

If you don’t meet the coinsurance requirement, you’ll face penalties. These penalties can cut down your claim payment a lot. This is true even for small losses.

Failing to meet your policy’s coinsurance percentage (often 80–90%) triggers a pro‑rata penalty, significantly reducing claims payouts. Ref.: “Next Insurance (2024). What is Coinsurance in Commercial Property Insurance? NextInsurance.com.” [!]

How Coinsurance Penalties Work

Let’s say you own a building worth $1,000,000. Your policy requires 80% coinsurance. So, you need at least $800,000 in coverage.

If you only have $600,000 in coverage and lose $200,000, you might think you’ll get the full $200,000. But, the coinsurance penalty changes that.

| Coinsurance Formula Component | Value | Explanation |

|---|---|---|

| Amount of Insurance Carried | $600,000 | Your actual coverage amount |

| Amount of Insurance Required | $800,000 | 80% of property value |

| Coinsurance Ratio | 75% | $600,000 ÷ $800,000 |

| Loss Amount | $200,000 | Cost to repair damage |

| Claim Payment | $150,000 | $200,000 × 75% |

In this case, you’d only get $150,000 for your $200,000 loss. This is because you only had 75% of the needed coverage. The coinsurance clause makes you share the cost of the missing coverage.

Strategies to Avoid Coinsurance Penalties

There are ways to avoid these penalties. The main thing is to keep your coverage up to date with your property’s value. This means not just its original value, but its current worth.

- Conduct regular professional appraisals – Property values change over time. Get a professional appraisal every 2-3 years.

- Update coverage after improvements – Any big changes to your property need a coverage review right away.

- Consider an agreed value endorsement – This lets you skip coinsurance for a year if you agree on your property’s value upfront.

- Account for business growth – As your business grows, so does your coverage needs.

- Review policy annually – Meet with your agent every year to make sure your coverage matches your property’s value.

Commercial property insurance is key for your business. But, it only works if you set it up right. Many business owners find out they’re underinsured after a loss.

The most expensive insurance policy is the one that doesn’t pay when you need it because of an avoidable coinsurance penalty.

Coinsurance Compliance Checklist

- Check your policy’s coinsurance percentage (usually 80%, 90%, or 100%).

- Find out your property’s current replacement cost value.

- Figure out the minimum coverage needed (property value × coinsurance percentage).

- Compare your current coverage to the minimum needed.

- Adjust coverage if it’s too low.

- Keep records of all valuations and coverage choices.

Remember, property insurance only protects you if you have enough coverage. Inflation, building code changes, and rising construction costs can create a gap if you’re not careful.

By understanding coinsurance and managing your coverage, you can avoid big surprises. These surprises can happen right after you’ve suffered damage.

Premium determinants location construction protection

The cost of protecting your commercial real estate through insurance is influenced by specific determinants. Savvy business owners can learn to navigate these factors. This gives you more control over your premiums.

Insurance carriers assess risk through three primary lenses when setting your premium:

- Location factors – Proximity to fire stations, crime rates in your area, and natural disaster zone designations

- Construction quality – Building materials used, age of structure, roof type and condition

- Protection measures – Fire suppression systems, security features, and risk management protocols

Your property’s value and replacement cost affect your premium. A $5 million building costs more to insure than a $500,000 one. Commercial property premium pricing factors extend beyond just value.

Location plays a big role that many business owners underestimate. Properties in flood zones, hurricane-prone coastal areas, or regions with high wildfire risk face higher premiums. Urban areas with elevated crime rates may increase your costs, while proximity to a fire station can reduce them.

Insurance is all about risk assessment. The more you can demonstrate that your commercial property presents a lower risk profile, the more leverage you’ll have in negotiating favorable premium rates.

Fire Suppression and Security System Credits

One of the most effective ways to reduce your commercial insurance premium is by investing in protective systems. Insurance carriers offer substantial credits—essentially discounts—for properties equipped with modern fire suppression and security systems.

These protective measures not only safeguard your physical assets but also translate directly into premium savings. Most carriers provide credits ranging from 5% to 15% per system, depending on the quality and comprehensiveness of your protection strategy.

| Protective Measure | Typical Discount | Installation Cost Recovery | Additional Benefits |

|---|---|---|---|

| Automatic Sprinkler System | 10-15% | 3-5 years | Reduced fire damage extent |

| Central Station Fire Alarm | 5-10% | 2-4 years | Faster emergency response |

| Security System with Monitoring | 5-8% | 3-4 years | Theft deterrence |

| Water Flow Detection | 3-5% | 1-2 years | Minimizes water damage |

I’ve seen clients recover their investment in these systems through premium savings alone. Not counting the additional benefit of preventing losses. When upgrading your property, keep detailed records of all improvements and certifications to ensure you receive every credit you deserve.

Loss History Effect on Renewal Premiums

Your claims history significantly impacts future premiums. Insurance carriers typically review the past 3-5 years of your loss history when determining renewal rates. A clean record can lead to preferred pricing, while multiple claims may trigger surcharges or even make coverage difficult to obtain.

The severity and frequency of claims both matter. One large claim might be viewed more favorably than multiple small claims, as the latter suggests ongoing operational issues. When a loss occurs, consider these strategic approaches:

- Evaluate whether the claim amount significantly exceeds your deductible.

- Consider handling very small losses out-of-pocket to preserve your loss history.

- Implement preventive measures after any claim to demonstrate risk management.

- Document all improvements made following a loss to share with your insurer.

Implementing a maintenance program can prevent many common claims. Regular roof inspections, plumbing system checks, and electrical system reviews help identify issues before they cause damage requiring an insurance claim.

Some types of commercial real estate naturally face higher claim frequencies. Retail properties with high foot traffic, for example, often experience more liability claims than warehouses with limited public access. Understanding the typical loss patterns for your property type helps you implement targeted prevention strategies.

While you can’t change your past claims, you can take control of future ones. I recommend creating a risk management plan that addresses your property’s specific vulnerabilities. This proactive approach not only protects your assets but also positions you favorably with insurers at renewal time.

Check out the below:

Filing claims and documenting property damage

When disaster hits, knowing how to file a claim is key. Commercial property insurance guards your business. But, you must follow the right steps after damage.

First, call your agent right away. Most policies need you to tell them within 24-48 hours. Take photos from different angles before you start cleaning.

Make a list of damaged items with when you bought them and their value. I’ve seen claims denied because of bad documentation. Keep all receipts for emergency fixes, as insurance covers these costs too.

Ask for at least three repair quotes from licensed contractors. This makes your claim stronger.

Get ready for the adjuster’s visit by organizing your papers. Show them everything—don’t skip minor damage. Read your policy so you know what’s covered.

Don’t accept the first settlement offer too quickly. Insurance starts with low estimates. If the offer is too low, ask for details and be ready to negotiate with proof.

The smartest thing? Make a property inventory before disaster strikes. Use digital tools to record your assets with photos, descriptions, and values. Keep this info in the cloud where damage can’t reach it.

Remember, insurance protects your investment. But, your help in the claims process is what really matters in recovery.

{kind=link}