Business vehicle coverage keeps your company safe from big money losses. Knowing why it’s important is key when personal policies don’t cover work.

Imagine your delivery truck crashes and causes $50,000 in damage. A scary fact: 73% of small businesses don’t have enough vehicle protection. This leaves owners on the hook for the costs.

I’ve seen many business owners find out their personal policies don’t cover work accidents. One client had to pay $80,000 in claims after an employee hit another car during work.

This insurance is like a shield for your money. It keeps your company safe, covers cars driven by employees, and handles big claims that could ruin your business.

Quick hits

- Covers liability beyond personal policy limits

- Protects against employee driving incidents

- Shields business assets from lawsuits

- Includes hired and non-owned vehicle coverage

Coverage for business owned vehicles

Business-owned vehicles need special insurance that personal policies don’t offer. If your company has cars, trucks, or trailers, commercial auto insurance is the right choice. It protects these vehicles for business use.

Many business owners think their personal auto policy covers company vehicles. But it doesn’t. Commercial vehicle insurance is needed for vehicles your business owns, leases, or uses often.

Commercial coverage is flexible. You can tailor protection for each vehicle in your fleet. You can pick different coverage levels based on:

- Vehicle value and replacement cost

- Age and condition of the vehicle

- How often you use it for business

- Safety ratings and risk factors

- Type of cargo or equipment transported

This way makes sense financially. A new delivery truck needs full coverage. An older pickup for occasional use might need basic protection.

Commercial auto insurance covers damage from accidents, theft, and weather. It also protects against liability if your vehicle causes damage or injuries.

You can adjust coverage for each vehicle. This helps match protection with your budget for all vehicles.

Next step: Make a list of all vehicles your business owns or uses. Note their values, how often they’re used, and any coverage gaps. This will help you decide on the right protection levels.

Read More:

Protection against third party liability

Accidents where your company vehicles harm others or their property are a big risk. Commercial auto insurance protects your business from huge lawsuits. I’ve seen small businesses face huge claims from accidents that seemed minor.

Third-party liability is a big danger for any business with vehicles. One accident can lead to huge medical bills, legal fees, and property damage claims. Without the right coverage, these costs can hurt your business and personal wealth.

Most states require a minimum of liability insurance. But these amounts are often not enough. Commercial insurance offers higher limits because business owners know the risks. It’s not just about the vehicles; it’s about protecting everything you’ve worked for.

Bodily Injury and Property Coverage

Bodily injury coverage helps when your vehicle hurts someone. It covers medical costs, lost wages, and pain-and-suffering claims. Serious injuries can lead to huge hospital bills, and disability claims can last for years.

Property damage coverage pays for damage to other items your vehicle hits. This includes cars, buildings, cargo, and equipment. Auto insurance helps whether your truck hits a fancy car or crashes into a store.

I suggest getting liability limits higher than the state minimum. Legal settlements often go beyond basic coverage. Many businesses start with $1 million per occurrence. This protects both your business and personal assets from lawsuits.

Safeguard drivers employees and assets

Commercial auto insurance does more than fix cars. It also protects your team and what they need to work. Every time your team drives for work, they face risks. The right insurance keeps them and your stuff safe.

Many business owners forget about this important protection. But it’s key. It pays for medical bills, replaces stolen stuff, and helps when employees use their cars for work.

Medical Payments for Injured Drivers

Medical payments coverage helps right away after an accident. It pays for hospital bills and treatment for anyone hurt in your vehicle. No fault needed—it pays no matter who was at fault.

This coverage pays for emergency room visits and more. It helps everyone in the vehicle, not just your team. I suggest having enough money set aside for medical costs, as they keep going up.

This coverage works with workers’ comp but gives quicker access to money. Medical bills don’t wait for long claims or fault findings.

Personal Effects and Equipment Loss

Regular auto insurance won’t cover lost business stuff. Your laptop, tools, or client materials need special protection. Personal effects coverage is key here.

Make a list of what your team takes with them. Include computers, tools, and more. Make sure your insurance can cover these costs. Don’t forget about seasonal or extra gear.

This coverage helps with theft, damage, and weather loss. Check your policy limits every year as costs change.

Hired and Non-Owned Auto Coverage

When employees use their cars for work, your business is covered. This coverage helps when personal insurance doesn’t. It protects your business from big claims.

Hired auto covers rental cars. Non-owned covers personal cars used for work. Both keep your business safe from big claims.

It’s important to know when employees can use their cars for work. Your insurance should match your business rules to avoid gaps.

“Check Out: What is the purpose of accident insurance?“

Compliance with state minimum requirements

Driving commercial vehicles without the right insurance can lead to big problems. I’ve seen businesses get fined, have their licenses taken away, and even shut down. This is all because they didn’t have enough insurance.

Each state has its own rules for commercial auto policy. These rules are much higher than what you need for a personal car. The liability limits can be anywhere from $25,000 to $100,000, depending on where you are.

Just because you have insurance for your personal car doesn’t mean it covers your business. Commercial auto insurance needs to be stronger because business vehicles are riskier. You can find out what your state’s commercial auto requirements are online.

Some states want more than just basic liability coverage. They might ask for personal injury protection, uninsured motorist coverage, or higher limits for property damage. Your insurance company can help, but it’s smart to check on your own.

Meeting state minimums helps you stay legal, but it might not be enough for your business. I suggest looking up your state’s Department of Insurance for the latest rules. Their websites have the minimum coverage amounts and what happens if you don’t meet them.

But remember, just meeting the minimums is only the first step. These amounts usually aren’t enough for growing businesses. Think about how much risk your business really has and choose coverage that fits.

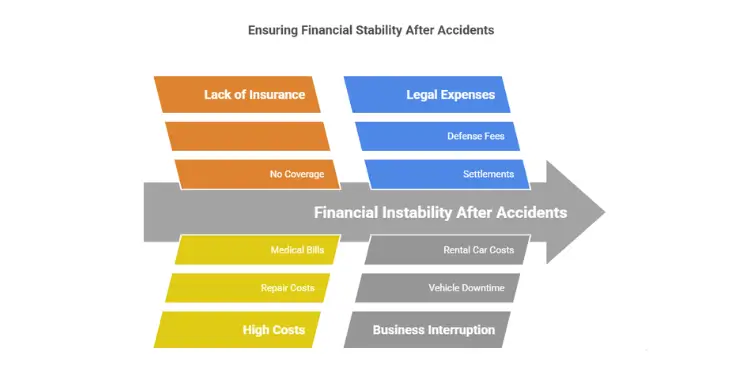

Financial stability after accident damages

Smart business owners know that commercial auto insurance keeps them stable in tough times. Without it, one big accident can empty your business’s bank account. You might have to cut back on equipment or staff.

Small companies often go bankrupt after a big crash. The repair, medical, and legal costs add up quickly. Your monthly premium becomes your lifeline when these expenses come in.

Here’s what commercial auto insurance cover when accidents happen:

- Vehicle repair and replacement costs

- Medical bills for injured drivers and passengers

- Legal defense fees and court settlements

- Business interruption expenses during vehicle downtime

- Rental car costs while your fleet gets repaired

Choosing the right coverage limits is key. Don’t just meet the state minimums. Think about your business’s total value and yearly income when setting limits.

Auto coverage should match your risk level. If you carry expensive equipment, your insurance needs to reflect that. Companies with many drivers face different risks than those with just one truck.

I’ve seen businesses recover quickly from total-loss accidents with good insurance. Others struggled for months with not enough coverage.

Your auto insurance helps keep your cash flow steady during hard times. Instead of selling assets or taking loans, you can file a claim. This keeps your business running smoothly and protects your employees’ paychecks.

Check your coverage every year as your business grows. What works for three vehicles might not be enough for ten. Insurance companies have tools to help you figure out the right limits for your business.

Remember: good commercial coverage is cheaper than one big lawsuit. Set limits that protect your business’s assets, not just your vehicles.

Cost control through tailored policy options

Smart business owners know how to save money on commercial auto insurance. You can pick the right coverage for each vehicle. This depends on its value, age, and how often it’s used.

A new delivery truck needs lots of protection. But an older work van might only need liability coverage.

Related Topics:

Deductible Choices and Fleet Discounts

Choosing a higher deductible can lower your monthly payments. If you can handle $1,000 expenses, you’ll save money. Someone with $250 deductibles will pay more.

Insuring many vehicles together can save 10-15% on premiums. This is called a fleet discount.

Business auto policies are different from personal ones. They offer flexible coverage levels. This way, commercial auto insurance fits your budget and protects your business.

Driver training and safety equipment can also save you money. These discounts add up with fleet savings.

It’s important to match coverage with your risks. Commercial auto insurance will cover what you need. It lets you skip extra coverage you don’t need.

Work with agents who know your business. They can help you save money.

Check your policy every year. As your vehicles or business needs change, update your coverage. This keeps your protection good and your costs low.

{kind=link}