The business owners policy helps small companies by covering many things at once. I’ve seen many Idaho Falls business owners struggle with different insurance policies. This can leave big holes in their protection.

Did you know 75% of U.S. small businesses don’t have enough insurance? And 40% have no insurance at all?

One client told me last year, “My BOP saved my shop when that pipe burst—I’d have lost everything with my old patchwork coverage.” This way of getting insurance saves 10-15% and makes things easier.

A good businessowners policy protects your stuff, keeps you safe from lawsuits, and helps you keep making money when you can’t work. Over the last ten years, I’ve seen it save many local businesses from big financial losses.

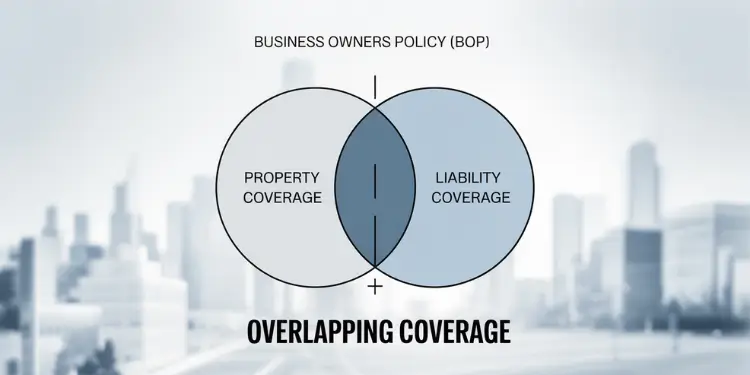

A Business Owners Policy (BOP) is a pre-packaged insurance solution combining general liability, commercial property, and business-interruption coverages for small to mid-sized businesses. Eligibility is typically limited to firms with ≤100 employees, annual revenue ≤$5–10 million, and <25,000 sq ft per location, with low-to-moderate industry risk. The policy provides first-party property replacement-cost coverage up to stated limits, third-party liability protection of $1–2 million per occurrence, and up to 12 months of actual-loss-sustained business income protection, while eliminating common inter-policy gaps.

Endorsements such as cyber liability, professional liability, equipment breakdown, or employment-practices liability can be appended to tailor coverage; premium pricing is driven by location, industry classification, claims history, and loss-control measures. Multi-policy bundling, higher deductibles, and documented safety programs reduce annual outlay by 10–25 % versus purchasing coverages separately.

Quick hits:

- Combines multiple coverages into one package.

- Saves money over separate policy purchases.

- Eliminates dangerous protection gaps automatically.

- Simplifies renewal and claims processes.

- Customizable for specific industry needs.

Bundling Property and Liability Coverages

When you put business property and liability insurance together in a BOP, you get a strong shield for your company. This smart move makes managing insurance easier and can save you money. I’ve helped many Idaho Falls business owners switch, and they feel a big relief right away.

A Business Owners Policy is key for every small business. It protects your stuff—like buildings, inventory, and equipment—against dangers like fire and theft. It also covers the things inside your buildings.

The liability part helps if someone gets hurt or if your product damages something. It pays for legal costs and settlements. This could be if someone slips in your store or if your ads hurt another company’s business.

Insurers offer better rates when you bundle these coverages. You also save time because you only have one policy to deal with.

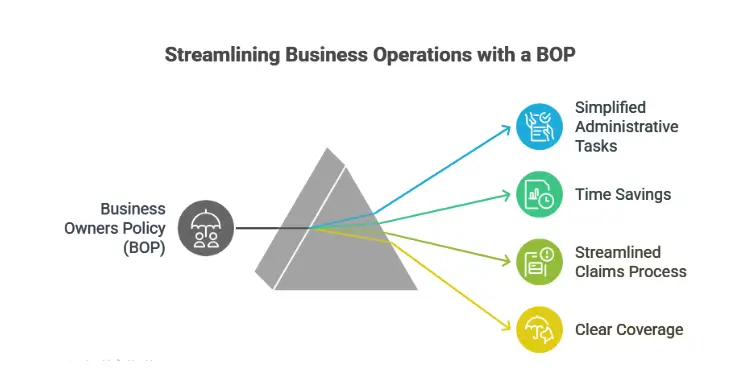

Single Policy Simplifies Administrative Tasks

Having a BOP makes things easier for your business. You won’t have to keep track of many policies anymore. You’ll have one policy to handle everything.

This saves you a lot of time. Business owners save 3-5 hours every quarter by switching to a BOP. You’ll make one payment, remember one renewal date, and keep one set of documents.

When you have a claim, a BOP makes things simpler. You won’t have to deal with different insurance companies. Instead, you’ll work with one adjuster who takes care of everything.

Imagine water damage that hurts your inventory and a customer. With separate policies, it can be hard to figure out who pays. But with a BOP, it’s clear who covers it all.

| Aspect | Separate Policies | Business Owners Policy | Business Impact |

|---|---|---|---|

| Premium Payments | Multiple due dates | Single payment schedule | Improved cash flow management |

| Policy Administration | 2-3 different contacts | One insurance relationship | Reduced communication complexity |

| Claims Process | Multiple adjusters | Single claims handler | Faster resolution times |

| Coverage Gaps | Common between policies | Eliminated by design | Fewer denied claims |

| Annual Time Investment | 12-20 hours | 4-6 hours | More focus on core business |

When you look at your business insurance, see if you can bundle your policies. Most small businesses can get a BOP. The benefits, like saving time and money, are worth it.

When you talk to your agent, ask about a bundle for your business. A good BOP should fit your business well and make managing insurance easier.

Read More:

Eligibility Criteria for Small Businesses

Small businesses need to meet certain rules to get a Business Owner’s Policy. Not every company can get this special coverage. Knowing these rules early can save a lot of time and trouble.

Insurance companies make BOPs for businesses with low risks. Now, more businesses can get this affordable option than before.

Revenue and Square Footage Thresholds

Insurance companies look at your business’s size and money when deciding if you qualify. They check:

- How much money your business makes each year. Some say under $5 million, but others go up to $10 million for certain types of businesses.

- How big your business places are. They can’t be over 25,000 square feet each.

- How many people work for you. It’s usually under 100 full-time workers.

These rules can change based on what kind of business you have and who you talk to. For example, small shops usually qualify, but big factories might not.

Last month, I helped a local bakery owner. She was denied because her sales were a bit too high for one company. But we found another that was okay with up to $7 million in sales for food businesses.

“The insurance industry has recognized that many small businesses operate with higher revenues today while maintaining relatively simple risk profiles. This has led to more flexible eligibility standards for Business Owner’s Policies across the board.”

Industry Risk Classifications Accepted Today

Insurance companies also look at how risky your business is. The type of business you have matters a lot:

| Risk Level | Typical Industries | BOP Eligibility | Special Considerations |

|---|---|---|---|

| Low Risk | Professional services, retail stores, small contractors | Excellent | Minimal additional requirements |

| Moderate Risk | Restaurants, small manufacturers, auto repair | Good | Higher premiums, additional underwriting |

| High Risk | Hazardous materials, high-value products | Limited | Often ineligible for standard BOPs |

| Recently Added | Food trucks, small healthcare, tech startups | Improving | Eligibility expanding annually |

The insurance world has changed a lot in recent years. More businesses can get business owners insurance now. If you were turned down before, it’s worth trying again.

I recently got a policy for a small urgent care clinic. Just three years ago, they would have had to pay more. This shows how insurance companies are more open to new business ideas.

To see if your business can get an owner’s policy, have these ready when you talk to an agent:

- How much money your business makes each year from tax filings

- How big your business places are

- What your business does

- How many people work for you

- Any losses your business has had in the last few years

With this info, you’ll know if an owner’s policy is right for your business. If not, a good agent can help find other ways to protect your business.

Standard Inclusions Across Insurer Offerings

Knowing what a Business Owners Policy covers is key. It helps you see if it’s right for your business. Most BOPs have similar protections, making them great for small business owners.

Property protection is the main part of every BOP. It keeps your building, stuff, and equipment safe from damage. This includes things like computers and furniture.

Most BOPs offer to replace damaged items without taking off for depreciation. This can save a lot of money, like when you need to buy new computers.

| Core BOP Component | What It Covers | Typical Limits | Common Exclusions |

|---|---|---|---|

| Property Protection | Building, equipment, inventory | Up to policy limits | Flood, earthquake |

| General Liability | Third-party injuries, property damage | $1-2 million | Professional errors |

| Business Income | Lost revenue during closure | 12 months of coverage | Planned closures |

| Employee Dishonesty | Theft by employees | $10,000-$25,000 | Theft by owners/partners |

General liability is another key part of BOPs. It protects your business from claims by others. This can save your business from big problems.

Business income coverage is also standard. It helps if you have to close because of damage. For example, if a fire hits your store, this coverage helps pay for things like rent and salaries.

Most policies offer this coverage for up to 12 months. This usually gives businesses enough time to get back on their feet.

Other standard parts include:

- Valuable papers coverage (protecting important documents)

- Accounts receivable protection (covering uncollectible amounts due to record loss)

- Limited off-premises property coverage (for equipment used away from your location)

- Electronic data protection (covering costs to restore lost information)

Most BOPs also cover employee dishonesty, but limits are usually low. If you handle a lot of cash or have valuable inventory, you might need more coverage.

“The true value of a BOP lies in its all-in-one approach to protecting small businesses. It fills gaps that separate policies might leave.”

Check these standard parts against your business to see if you need more. While BOPs are great for most small businesses, your specific needs might require extra coverage.

Optional Endorsements Expanding BOP Protection

Beyond the standard protections in a BOP, optional endorsements offer tailored coverage for specialized risks your business may face. These add-ons integrate seamlessly with your existing policy, eliminating the need for separate insurance purchases in many cases.

As a business insurance advisor, I’ve seen firsthand how the right endorsements can make the difference between recovery and financial disaster after an unexpected event. Let’s explore the most valuable options to consider.

Data Breach and Cyber Liability Protection

With digital threats increasing daily, cyber protection has become essential for businesses of all sizes. A data breach endorsement typically covers:

- Customer notification costs following a breach

- Credit monitoring services for affected individuals

- Legal defense if customers sue after their data is compromised

- Forensic investigation expenses to determine breach scope

For businesses storing customer information, I recommend at least $100,000 in cyber coverage. If you process payments or handle medical records, consider limits of $250,000 or higher.

Business Interruption Coverage

Business interruption insurance provides critical financial support when operations halt due to covered property damage. This endorsement replaces lost business income during the restoration period, helping you meet ongoing expenses like payroll and rent.

When evaluating business interruption coverage, pay attention to the “restoration period” – typically 30, 60, or 90 days. For businesses with specialized equipment or unique inventory, longer restoration periods offer better protection.

“Nearly 40% of small businesses never reopen after a disaster, often because they lack adequate business interruption coverage to sustain them through the recovery phase.”

Professional Liability Endorsements

Service-based businesses face unique risks when clients claim financial harm from mistakes or negligence. Professional liability endorsements (sometimes called errors and omissions coverage) protect against claims alleging:

- Negligent professional services

- Failure to deliver promised results

- Errors or omissions in your work

- Incomplete or inadequate advice

This protection is valuable for consultants, real estate agents, insurance brokers, and similar professionals whose advice could impact clients’ financial wellbeing.

Employment Practices Liability Insurance

EPLI endorsements shield your business from claims involving workplace conduct issues. With the average employment claim costing over $75,000 to defend and settle, this protection has become increasingly important even for businesses with just a few employees.

These endorsements typically cover claims related to:

- Wrongful termination

- Discrimination (age, gender, race, disability)

- Sexual harassment

- Hostile work environment

Equipment Breakdown Coverage

Formerly called boiler and machinery coverage, equipment breakdown protection pays for repairs when mechanical, electrical, or pressure systems fail. Standard property coverage typically excludes these events, creating a significant gap for businesses relying on specialized equipment.

This endorsement is valuable if your business depends on:

- HVAC systems

- Refrigeration units

- Manufacturing equipment

- Electrical systems

Additional Valuable Endorsements

| Endorsement Type | Protects Against | Ideal For | Typical Cost Impact |

|---|---|---|---|

| Hired & Non-owned Auto | Liability from employee-driven vehicles | Businesses with delivery or client visits | 5-10% premium increase |

| Outdoor Signs | Damage to exterior signage | Retail and restaurant businesses | 2-5% premium increase |

| Spoilage Coverage | Loss of perishable inventory | Food retailers and restaurants | 3-7% premium increase |

| Inland Marine | Property in transit or off-premises | Contractors and mobile businesses | 7-15% premium increase |

When evaluating which endorsements to add to your BOP, I recommend focusing on your specific operational vulnerabilities. The right combination of endorsements creates a policy that truly addresses your business’s unique risk profile.

Remember that your BOP combines business property and business liability insurance in a foundational package. These endorsements build upon that foundation to create protection tailored to your specific needs.

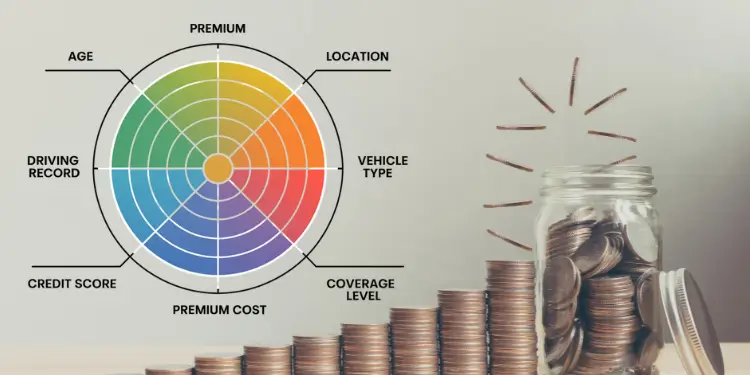

Premium Pricing Factors and Savings Strategies

Many things affect your Business Owner’s Policy premium. Knowing these can help you save a lot. It’s important to understand what affects your BOP costs.

Where your business is located is very important. Businesses in cities pay 30-40% more than those in rural areas. For example, a store in downtown Los Angeles might pay more than one in suburban Idaho.

Your business type also matters a lot. Offices usually pay less, but restaurants and contractors pay more. This is because some businesses are riskier than others.

Your claims history is very important. Insurers look at your claims from 3-5 years ago. Having no claims can save you a lot of money in the long run.

| Premium Factor | Impact Level | Potential Savings | Business Owner Control |

|---|---|---|---|

| Location | High | 5-10% | Limited |

| Industry Type | High | Varies | Limited |

| Claims History | High | 10-25% | Moderate |

| Building Features | Medium | 5-15% | Moderate |

| Loss Control Programs | Medium | 3-15% | High |

What your building is like also matters. New buildings with good fire systems can save you 5-15% on premiums. Insurers see these as ways to lower risks.

Loss Control Programs Reducing Premiums

Having loss control programs is good for your business and can lower your insurance costs. It shows insurers you’re serious about safety, which can lead to lower premiums.

Security systems are a simple way to save money. Installing alarm systems can save you 5-10% on your business owner’s policy. They help prevent theft and alert you to emergencies.

Training your employees is also smart. Many insurers give discounts for safety training. This can save you 3-8% on premiums.

Keeping your equipment in good shape is another way to save. Regular checks on things like electrical and HVAC systems can save you money. They also help prevent big problems.

- Increasing your deductibles can save you 10-15%. But, you need to have enough money for the higher deductibles when you make a claim.

- Getting multiple policies from the same company can save you 5-15%. It’s worth combining your insurance.

- Check your coverage every year. As your business grows, your insurance needs might change. This ensures you’re not paying for too much.

- Work with an insurance agent who knows your industry. They can find discounts and options just for your business.

Increasing deductibles can save 10–15% on premiums but requires readiness to cover higher out-of-pocket costs. Ref.: “Business.com. (2025). How to Save Money on Business Insurance. Business.com.” [!]

Getting help from insurance experts who know Business Owner’s Policies is a good idea. They can help you find the right coverage and save money. They know how to tailor a BOP to your business’s needs.

Don’t just look for the cheapest policy. You want to find a balance between good coverage and affordable prices. This balance changes as your business grows and changes.

“Check out the below: Do I need life insurance for my family?“

Application Process and Policy Renewal Steps

Getting a business owners policy is easy and quick. First, gather important info like how much money your business makes, what you own, and how many people work for you. Most companies let you apply online, but talking to an agent can help you get better coverage.

After you apply, you’ll hear back in 1-3 business days. Once you get approved, read your policy carefully. This is important to know what your policy covers and what it doesn’t.

Renewing your policy happens every year. You’ll get a notice 30-60 days before it ends. Renewing your policy is a chance to make sure it fits your business’s needs.

When it’s time to renew, think about any big changes in your business. This could be new places, buying new stuff, or hiring more people. These changes might mean you need to update your policy. Many companies give discounts for businesses with no claims.

If you’re new to business insurance, ask for quotes every 2-3 years. Don’t change insurers too often to avoid gaps in coverage. Renewal is a good time to check if your deductibles and limits are right for your business.

{kind=link}