Builders risk insurance is key for protecting construction sites. It keeps your investment safe from unexpected problems.

Builders risk insurance protects a project’s labour, materials, and profit while work is under way. According to a March 2025 market study, global builders-risk premiums reached ≈ USD 5.36 billion in 2024 and are projected to climb to USD 8.75 billion by 2033.

NAIC 2024 market-share filings also show a steady uptick in policy take-up on commercial starts. The coverage, therefore, is now treated as a baseline risk-transfer tool rather than a ‘nice-to-have’.

Do you worry about hidden dangers? A recent NAIC survey showed 70% of new buildings have this insurance.

The NAIC says it’s a smart choice. I’ve seen clients feel better after getting coverage.

Builders risk insurance provides time-bound protection for construction projects by covering labor, materials, and anticipated profit against physical damage and specified perils from the moment materials arrive until project completion. Global premiums reached approximately USD 5.36 billion in 2024 and are projected to climb to USD 8.75 billion by 2033, while NAIC filings indicate over 70 % of new builds now secure this coverage as a baseline risk-transfer mechanism.

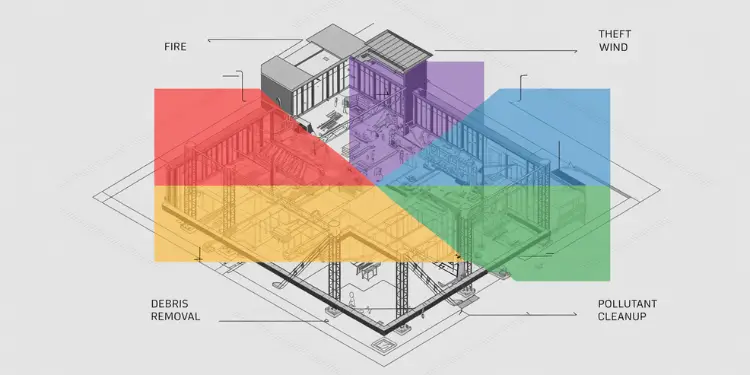

Coverage typically includes fire, theft, wind, debris removal, pollutant cleanup, and optional cyber-interruption endorsements, with specialized endorsements available for off-site modular components, soft costs, and profit overhead. Standard forms exclude employee theft, workmanship defects, and design flaws without endorsements; contractors and stakeholders should verify policy declarations, sub-limits, and endorsements to ensure alignment with lender, government, and investor requirements.

Quick hits

- Satisfies lender draw-schedule requirements.

- Shields against climate-driven events (flood, wildfire, convective storm).

- losses that pushed 2024 catastrophe claims past USD 135 billion.

- Covers off-site modular components in transit or storage.

- Optional cyber-incident and ransomware endorsements protect on-site digital equipment.

Coverage scope for builders risk policies

I’ve seen teams miss important job site dangers. This can lead to unexpected repair costs. Builders risk policies protect against damage from fires, theft, or wind.

They help keep your budget safe from sudden problems. Your insurance company can cover key materials, giving you peace of mind. Policies filed since late 2024 can extend to debris removal, pollutant clean-up, and limited cyber interruption where construction IoT devices are hacked, provided the cyber sub-limit is scheduled.

Most builders risk policies are written on an “all-perils” basis—covering any cause of loss unless explicitly excluded—enabling broad debris removal, pollutant cleanup, and cyber‐interruption protection. Ref.: “Building the Right Builders Risk Policy. (2011). Building the Right Builders Risk Policy. IRMI.” [!]

Materials fixtures and temporary structures covered

Coverage now routinely applies to factory-built wall panels, 3-D-printed concrete sections, and temporary EV-charging pods stored within 100 ft of the site. They also protect storage trailers and other support structures. This helps keep your project moving smoothly.

The goal is to protect your investment from the start. Every piece brought to the site is covered.

Excluded perils contractors must address

Some risks need special coverage. Things like employee theft or poor workmanship are often not included. You might need to add extra coverage for these risks.

Most 2025 forms also exclude cyber events (e.g., malware in on-site BIM servers) and design defects unless a re-work endorsement is purchased. Things like employee theft or poor workmanship are often not included.

It’s wise to talk to your risk manager or agent about this. They can help you get the right coverage for your project. Every contractor faces different risks, depending on their work.

| Coverage Element | Typical Inclusion |

|---|---|

| Fire Damage | Included |

| Stored Materials | Optional Endorsement |

| Employee Theft | Usually Excluded |

| Defective Work | Excluded Unless Negotiated |

| Flood / Storm Surge | Often Excluded or High Deductible |

| Cyber Interruption | Endorsement-Only |

Ask your agent if your builder’s policy covers all the risks at your site.

Contractors must negotiate endorsements to include exclusions such as employee theft and design defects, which standard forms omit by default. Ref.: “Understanding Builder’s Risk Insurance Coverages and Exclusions. (2021). Understanding Builder’s Risk Insurance Coverages and Exclusions. Construction Executive.” [!]

“Read More: general liability insurance essentials“

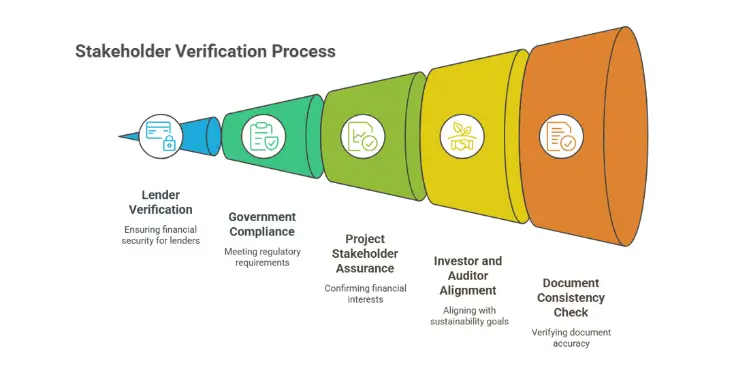

Stakeholders that demand builders risk certificates

Lenders often want a record of builders risk insurance before releasing funds. This document helps them feel safe about unfinished work and dangers on-site. If borrowers skip this, financing can stall.

Government agencies might ask for it if the project touches public roads or follows municipal codes. They want to protect taxpayer money and make sure the right liability limits are set.

Property owners, contractors, and sub-contractors also need proof. They all have a financial interest in the project’s success. A simple email or meeting can clear up any doubts.

Property owners, contractors, and sub-contractors also need proof. They all have a financial interest in the project’s success. A simple email or meeting can clear up any doubts.

Institutional investors and ESG auditors increasingly request proof of builders-risk insurance to verify resilience against climate-related loss, aligning with broader sustainability disclosures.

Then, check any loan or contract paperwork. Make sure the names on the insurance match the actual roles. This avoids confusion later on.

Mis-naming insured parties in loan documents can void coverage; strict alignment between policy declarations and contract roles is mandatory. Ref.: “The Best 101 Guide to Builders Risk Insurance. (2023). The Best 101 Guide to Builders Risk Insurance. US Assure.” [!]

“Related Articles: commercial auto insurance coverage“

Builders risk policy period inception to completion

Remember when your new construction coverage starts. It often begins when materials arrive or work starts. This coverage protects your project from start to finish.

How long it lasts depends on your project and local rules. It might end when the home is ready for people to move in. Builders risk coverage keeps you safe until the very end.

Managing Extensions for Weather Delays

Bad weather can mess up your plans. I’ve seen people ask for extra time because of rain or snow. Extensions give you more time to finish your project.

It might end when the home is ready for people to move in. Builders risk coverage keeps you safe until the very end. If the owner begins ‘soft-opening’ operations before full completion, an early-occupancy endorsement can bridge the gap until permanent property insurance attaches.

NAIC (2022) says to keep records of delays. Use forecasts from the National Weather Service to support your requests.

| Extension Reason | Typical Duration | Resource |

|---|---|---|

| Snow or Flood Forecast | Up to 30 Days | National Weather Service |

| Severe Storm Impact | 2–4 Weeks | FEMA Reports |

Read More:

Calculating completed value and soft costs

Every builders risk insurance plan includes direct building costs and overhead. I’ve seen people miss these important details. Soft costs are things like design fees, permits, and loan interest.

They keep your project going if something unexpected happens. Some policies let you add overhead, increasing the total insured amount.

Covering profit overhead and system testing

You can also add profit coverage to protect your expected profit. Overhead costs, like on-site management or safety checks, can be included too. Testing coverage helps if you need to fix specialized systems before finishing the project.

“You Might Also Like: cyber insurance for small business resilience“

Using escalation clauses for material inflation

Material prices can go up suddenly. An escalation clause helps protect you from these price jumps. It adjusts the insured amount to match rising material costs.

Some policies let you add overhead, increasing the total insured amount. Copper wire alone rose 8.6 % year-over-year through Q4 2024; escalation clauses indexed to ENR or PPI saved many projects from six-figure overruns.

This can save you money if lumber or wiring prices increase at the last minute.

| Soft Expense | Coverage Benefit |

|---|---|

| Architect Fees | Helps recoup professional design costs |

| Permit Costs | Protects funds spent on mandatory approvals |

| Loan Interest | Offsets financing charges during construction |

“Related Topics: workers compensation insurance explained“

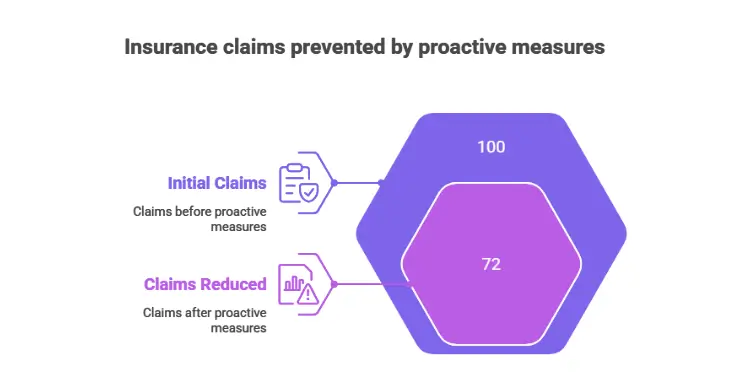

Preventing claims with proactive site controls

Deploying AI-equipped drones for nightly patrols, coupled with IoT moisture sensors inside framed walls, reduced theft and water claims by up to 28 % in 2024 pilot programmes. Fencing the area, using bright lights, and security cameras make it harder for troublemakers. Keeping materials in a locked trailer or room also helps a lot.

This means fewer insurance claims. It makes renewal talks easier. A secure site is good for everyone’s peace of mind.

By reducing claims, you save money. This can lead to better insurance rates. For tips on keeping your site safe, check out these best practices. It helps protect your work and keeps your finances stable.

Emerging parametric and alternative structures

Parametric builders-risk policies pay a predefined amount once a trigger—such as wind speeds of ≥ 80 mph within 5 km of the site—is recorded. Because payment is based on the trigger rather than an itemised loss adjustment, funds reach the project faster and help restart work after severe events.

Hybrid alternatives, including owner-controlled insurance programmes and captives, can also be layered with traditional builders-risk coverage to address large deductibles or excluded perils.

{kind=link}