The journey to buy a house starts with knowing your finances. It’s not just helpful; it’s key to getting good mortgage deals. It also helps avoid surprises when buying a home.

Did you know getting your finances ready 6-12 months before can help a lot? With U.S. home prices at $419,200 in early 2024, being ready is more important than ever.

“Your overall financial health is what lenders look at most,” says the Consumer Financial Protection Bureau. In my nine years helping first-time buyers, I’ve seen it. Those who budget well before buying get better rates and face fewer problems.

This guide makes tough financial tasks easy. You’ll learn how to impress lenders and feel confident when buying a home.

Quick hits:

- Track spending for three full months

- Document all income sources thoroughly

- Pay down high-interest debt first

- Build emergency savings beyond downpayment

- Gather tax returns from previous years

The national median sales price reached $419,200 in Q1 2024—up 27 % in five years—highlighting why early financial prep is essential for first-time buyers Ref.: “U.S. Census Bureau & U.S. Department of Housing and Urban Development. (2025). Median Sales Price of Houses Sold for the United States (MSPUS). FRED.” [!]

Assess current income and expenses

Before you buy a home, check your money first. I’ve helped many first-time buyers. They often don’t know how much they spend each month.

This mistake can stop your homebuying dream. To know how much house you can buy, you need to know your money’s path.

“You Might Also Like:

Track Spending with Budgeting Apps

Use apps like Mint or YNAB to track your spending. Do this for 60 days. It shows where your money really goes.

These apps show the truth about your spending. One client thought she spent $200 on dining out. But it was really $475. This changes how much house she could buy.

These apps help you find extra money for your home buying budget checklist. Many first-time buyers find $200-$300 to save each month.

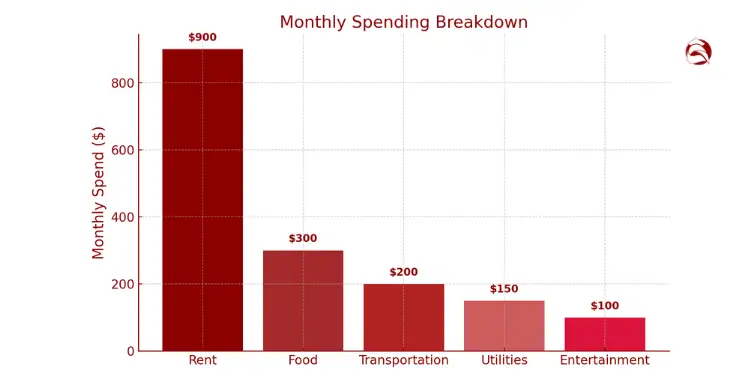

Identify Unavoidable Monthly Obligations Cost

Make a list of monthly costs you can’t avoid. Include rent, utilities, and loans. Be honest about what you really spend.

After taxes, see how much you have left. This is your base for a mortgage payment.

Lenders look at your total housing costs. They want it to be less than 28% of your income. If you can handle $1,500 in housing costs but pay $1,200 now, you know what to look for in a house.

This step is key to buying a home. It helps you know what price range to look for. It also keeps you from falling in love with homes that are too expensive. When you talk to lenders, you’ll be ready and know what you can afford.

Federal Qualified-Mortgage rules cap total debt-to-income (DTI) at 43 %. Crossing that line usually disqualifies borrowers from prime-rate loans and triggers costly alternatives Ref.: “Consumer Financial Protection Bureau. (2021). Regulation Z §1026.43(e) Debt-to-Income Requirements. Federal Register.” [!]

Pay down high interest debts

High-interest debt is a big problem when you want to buy a home. It limits how much you can spend on a house. It also takes money away from your down payment.

Lenders look closely at your debt-to-income (DTI) ratio. This ratio shows how much of your income goes to debt. They want it to be 43% or less.

But, if you can get your DTI below 36%, you’ll get better interest rates. This can save you up to $50,000 over 30 years. It’s like getting a new car for free!

Credit card debt is very bad for buying a home. Interest rates on these cards are high, 18-24%. This makes you look riskier to lenders and takes money from your down payment.

“The fastest way to improve your mortgage terms isn’t saving more—it’s owing less. Every $100 in monthly debt payments eliminated potentially increases your home purchasing power by $15,000-$20,000.”

Before deciding, think about paying off high-interest debt. A client of mine paid off a $5,000 credit card balance. This improved her DTI ratio and got her a lower interest rate. She saved $87 a month, over $31,000 in the loan’s life.

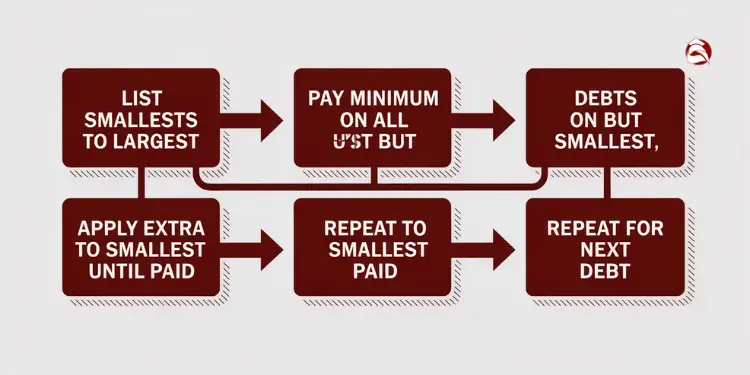

Strategize Debt Snowball Repayment Plan

I’ve helped many first-time buyers with their finances. The debt snowball method is very effective. It gives you quick wins to keep you motivated.

Here’s how to use the debt snowball method:

- List all debts from smallest to largest balance (regardless of interest rate). Include the minimum payment for each.

- Pay minimum payments on everything except the smallest debt.

- Direct every extra dollar in your budget toward that smallest debt until it’s completely paid off.

- Roll that entire payment (minimum plus extra) into attacking the next smallest debt.

- Repeat until all debts are eliminated or reduced to a manageable level.

For those with many high-interest debts, consider a personal loan at a lower rate. This can simplify payments and lower your interest rate. But, make sure not to add new debt while paying off the loan.

Keep track of your debt reduction each month. Check your free credit report from annualcreditreport.com every quarter. This ensures your credit report is accurate, which is important for mortgage applications.

Reducing debt not only helps with your mortgage but also gives you more money for unexpected expenses. This makes it easier to handle surprise costs without using credit cards. It helps you reach your long-term financial goals as a homeowner.

“Learn More About: Essential single income home buying budget strategies“

Build dedicated home purchase savings

Creating a savings plan just for your home is key. It stops you from using house money for other things. Keep your home savings separate from your daily money.

First, figure out how much you need for your mortgage. Conventional loans might need only 3% down. FHA loans ask for 3.5%. Some loans, like VA or USDA, might not need any down payment.

For example, on a $300,000 home, you might need $9,000 for down payment. Also, think about closing costs, which can be 2-6% of the loan amount. This adds $6,000-$18,000 to your savings goal.

Saving 20% ($60,000 on a $300,000 home) can save you money each month. Your total savings goal should be at least $15,000 for a $300,000 home. Saving more is always good.

Putting down less than 20 % triggers private mortgage insurance (PMI), typically adding $30 – $70 per $100 k borrowed each month until you reach 20 % equity Ref.: “Freddie Mac. (2025). Breaking Down Private Mortgage Insurance (PMI). Freddie Mac.” [!]

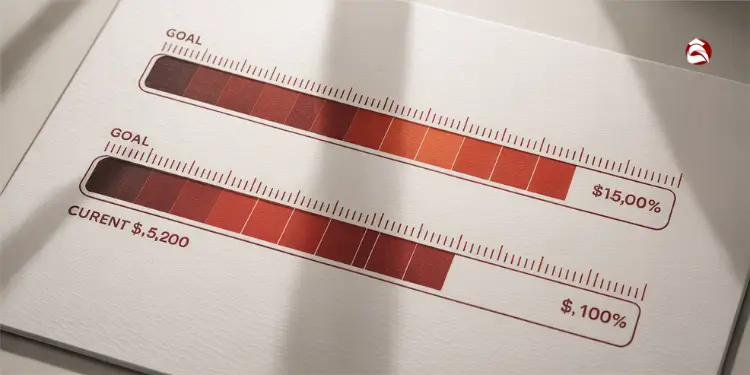

Automate Transfers to Dedicated Account

Successful homebuyers make saving automatic. Set up transfers to your home savings account right after you get paid. This way, you save before you spend.

Even small transfers of $200 every two weeks add up to $5,200 a year. To save $15,000, you could do this in under three years. The key is to be consistent with these transfers.

Top online high-yield savings accounts now pay roughly 4.75 – 5.15 % APY—about ten times branch-bank averages—so parking your down-payment fund there can add hundreds in risk-free interest each year Ref.: “Ngo, S. (2025). Best High-Yield Savings Accounts for June 2025. Bankrate.” [!]

Allocate Windfalls Toward Down Payment

Unexpected money can help you save faster. Use all extra money like tax refunds, bonuses, or side hustle earnings for your home savings.

One client saved $8,000 in six months with her tax refund, bonus, and side hustle money. Unexpected money can help you reach your goal faster. Always put it in your home savings first.

Choose High Yield Savings Vehicle

Where you save your down payment is important. Regular savings accounts pay very little interest. But, high-yield savings accounts can earn 4-5% APY.

For saving 1-3 years, high-yield savings are great. For longer, CDs or Treasury bills might offer more but keep your money safe. Don’t risk your down payment in stocks or cryptocurrencies.

Also, keep an emergency fund for 3-6 months of expenses. Buying a home without this fund is risky. You’ll need it for unexpected costs like repairs.

Boost credit score for mortgage

Boosting your credit score before applying for a mortgage is very important. In nine years, I’ve helped many first-time buyers save thousands by improving their credit. This can save you a lot of money.

Your credit score affects the interest rate you get from lenders. Many buyers don’t know how much this can save. For example, a 640 score can save you 0.5-1% in interest compared to a 740 score.

This small difference can mean saving $30,000-$60,000 on a $300,000 mortgage. That’s enough to buy new furniture or fund future home improvements.

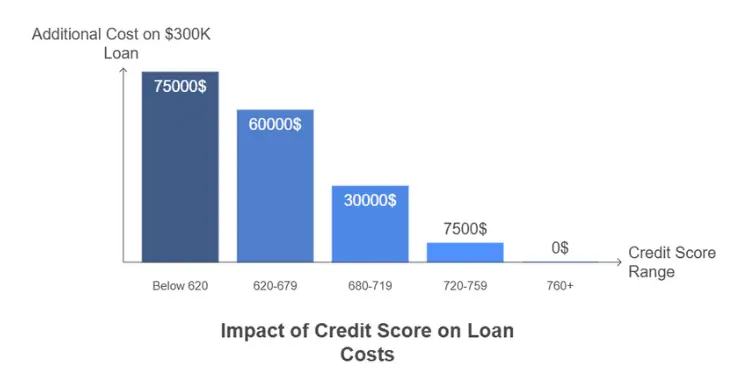

Understanding Credit Score Requirements

Most mortgage lenders want a credit score of at least 620. But, just meeting this minimum doesn’t get you the best rates. To get the best rates, you need a score above 760.

If your score is below 620, start improving it before you look for a house. Payment history is 35% of your FICO score. So, make sure to pay on time for at least six months.

Strategic Credit Improvement Tactics

First, get your current FICO score. This is the score lenders use. Many credit card companies offer free scores, or you can buy one from myfico.com.

After you know your score, use these tips:

- Pay down credit card balances to below 30% of available credit on each card

- Avoid applying for new credit in the 6 months before mortgage application

- Check your credit report for errors (present in roughly 20% of reports)

- Keep old credit accounts open to maintain your credit history length

- Continue making all payments on time throughout the homebuying process

Remember, lenders will check your credit again just before closing. A late payment or new credit account can hurt your loan approval or rate lock.

Timeline for Credit Improvement

If your score needs a lot of work, start improving 6-12 months before you look for a house. Credit improvement takes time, but three months of good habits can make a big difference.

If you already have a score above 700, keep up the good work. Avoid any negative marks. The house price to income ratio you can afford will improve with each credit score improvement.

| Credit Score Range | Typical Interest Rate Impact | PMI Requirement | Additional Cost on $300K Loan | Recommended Action |

|---|---|---|---|---|

| Below 620 | May not qualify | High PMI or FHA required | $75,000+ | Delay purchase, focus on credit repair |

| 620-679 | +0.75-1.25% | Higher PMI premiums | $45,000-$75,000 | Aggressive credit improvement plan |

| 680-719 | +0.25-0.75% | Moderate PMI premiums | $15,000-$45,000 | Target specific improvement areas |

| 720-759 | +0-0.25% | Lower PMI premiums | $0-$15,000 | Maintain good habits |

| 760+ | Best available rates | Lowest PMI premiums | $0 | Shop multiple lenders for best deal |

Once your credit score is as high as it can be, don’t accept the first mortgage offer. Shop around with at least three lenders. Each lender has slightly different criteria, and comparing offers can save you thousands in interest and fees.

Remember, private mortgage insurance (PMI) rates also depend on your credit score. A higher score means lower insurance premiums. This can save you money if you put less than 20% down.

Document reliable income verification sources

Having the right income documents is key for your mortgage. It shows lenders you can make payments over time. In my nine years helping first-time buyers, I’ve seen delays because of missing paperwork.

Start getting your income documents ready three months before you apply for pre-approval. This shows you’re financially ready and speeds up the process. Having your documents ready also makes you feel more confident when you start your mortgage application.

Gather Pay Stubs and Tax Returns

For W-2 workers, lenders need specific documents to check your job and income. Start by getting your last two pay stubs. These show your current income and how much you’ve made so far this year.

Then, get your W-2 forms from the last two years. These forms show your yearly income and taxes. You’ll also need your federal tax returns from the last two years. These returns give lenders a full view of your finances, including any extra income.

I suggest making a folder for these documents. It can be physical or digital. Make sure to label everything clearly. This will help you a lot when your lender asks for more information.

“Check This Out: How to track home buying expenses during the process“

Record Freelance or Side Income

Self-employed buyers need to show more proof of income. You’ll need your business tax returns from the last two years and detailed profit and loss statements. Lenders might also ask for a letter from your accountant about your business income.

Freelancers or those with side jobs should track all their income. Use a spreadsheet to show how much you make from different sources. Most lenders want to see two years of this income before counting it.

If you get alimony, child support, or regular payments, collect proof of these for at least 12 months. Knowing what documents you need can help first-time buyers avoid delays.

Download statements from the last two months for all your financial accounts. This includes checking and savings accounts, retirement funds, and investments. These statements help show you have enough money for a down payment and other costs.

| Income Type | Required Documentation | Minimum History | Special Considerations |

|---|---|---|---|

| W-2 Employment | Recent pay stubs, W-2 forms, tax returns | 2 years | Job changes in same field generally acceptable |

| Self-Employment | Business tax returns, profit/loss statements, accountant letter | 2 years | Income averaged over 24 months; declining income scrutinized |

| Freelance/Gig Work | Income tracking spreadsheet, bank statements showing deposits | 2 years | Must show stability and consistency |

| Alimony/Child Support | Court order, bank statements showing deposits | 12 months | Must continue for at least 3 years after mortgage approval |

| Investment Income | Account statements, tax returns showing dividend history | 2 years | Only counted if expected to continue for 3+ years |

Remember, different lenders might ask for different documents. But having these key documents ready shows you’re serious and responsible. This makes your mortgage process smoother and shows lenders you understand the commitment of owning a home.

“Related Topics:

Consolidate financial records for lender

Putting together a neat financial package for your mortgage shows you’re ready to buy a home. I’ve seen buyers get approval in 48 hours with good documents. But others waited weeks because their documents were messy.

Begin by making a digital folder three months before you apply. Put tax returns, pay stubs, bank statements, and debt info in subfolders. Lenders want to see how much you can afford based on your money situation.

Your package should have:

• Two years of tax returns with all schedules and W-2s

• Recent pay stubs covering 30 days

• Two months of statements from all financial accounts

• List of debts with account numbers and balances

• Proof of your down payment savings goal

Self-employed buyers need extra records like profit/loss statements and business tax returns. Any big deposits need a clear reason—unexplained money worries lenders.

If you’re using gift funds for your down payment, include a letter from the donor saying it’s a gift. Also, have a document explaining any credit problems or job gaps.

Keep everything organized until closing day. Being ready speeds up approval and helps you manage your money better. With everything in order, you’ll feel confident at open houses, knowing what you can afford.

{kind=link}