Knowing the difference between needs and wants is key to smart home buying. It helps you make choices that fit your budget. Many buyers regret their choices because they mixed up wants with needs.

About 58% of Americans with credit card debt don’t have a plan to pay it off. They often choose wants over needs. I tell my clients, “Your mortgage approval sets the ceiling, but your actual comfort zone lives several steps below that number.”

I’ve helped over 200 first-time buyers. I see how important it is to know the difference when you’re on a budget. The choice between a starter home and a forever home adds to the challenge. My approach helps separate must-haves from nice-to-haves.

Quick Hits:

- Identify true non-negotiable housing requirements

- Rank optional features by importance

- Stay below maximum mortgage approval

- Consider long-term financial implications

- Make data-driven compromise decisions

Defining non negotiable living requirements

Starting to buy a home means knowing what you must have. Before looking at any houses, make a list of what you can’t live without. This list helps you decide what’s right for you.

Make a simple checklist with two columns: “Must Have” and “Nice to Have.” In the “Must Have” column, list only what you need every day. These are things that make a house work for your family.

Use a written “Must-Have vs Nice-to-Have” wish list before touring any homes. Freddie Mac data show that buyers who formalize priorities early shorten their search time and reduce decision regret.Ref.: “Freddie Mac. (2024). Making a Homebuying Wish List. My Home by Freddie Mac.” [!]

This step is key. Maria knew she needed a house with ground-floor access, two bedrooms, and a short commute. This helped her find a home in three weeks, not three months.

Space, Bedrooms, Bathrooms: Family Needs

Your family’s size and daily life shape your space needs. Figure out the minimum number of bedrooms for now and the next 3-5 years. For example, a third bedroom is a must for teenagers of different genders.

The number of bathrooms is also key for peace at home. A couple might do with one, but kids need more, and so does morning routine. Think if you really need more than one full bathroom.

Other spaces are also important. Do you need a home office for work? Is a yard for kids or pets a must? Does someone need a house on one level because of health issues?

| Family Situation | Essential Space Requirements | Common Mistakes | Budget Impact |

|---|---|---|---|

| Working parents with infant | 2 bedrooms, home office space, proximity to childcare | Underestimating storage needs for baby equipment | 10-15% premium for dedicated office space |

| Family with teenagers | 3+ bedrooms, 2+ bathrooms, study space | Ignoring need for separate study areas | 20-25% increase for additional bathroom |

| Multi-generational household | Bedroom on main floor, wider doorways, accessible bathroom | Overlooking accessibility features | 5-30% premium for accessible features |

| Remote workers | Dedicated office space, reliable internet service area | Assuming any spare room works as an office | 8-12% premium for homes with dedicated office |

Accessibility and Commute Time Limits

Set clear limits on where you can live and how long it takes to get there. Long commutes can make life stressful. Decide how far you can travel to work, school, and shops.

The IRS standard mileage rate for 2025 is 70 ¢ per mile—up from 58 ¢—so a 10-mile daily commute now adds roughly $140 each month in vehicle costs (20 workdays).Ref.: “Internal Revenue Service. (2025). Standard Mileage Rates. IRS.gov.” [!]

For many, school zones are a must. If your kids go to certain schools, you must live nearby. This might mean private schools or complex travel plans.

Think about special needs that affect where you can live. My client needed an elevator in every home. Another family had to be close to a doctor’s office.

Also, think about how you’ll get around. Do you need public transit or parking for your cars? Will you use rideshare or walk to places?

Your checklist is your first guide when looking at homes. Talk about it with your agent before seeing any houses. This saves time and helps avoid falling for a house that doesn’t meet your needs.

“Discover More: Must have home buying budget tools for buyers“

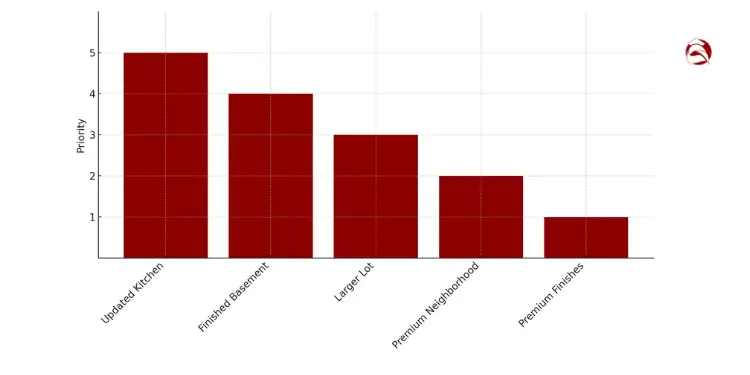

Ranking desirable but optional features

Knowing what to spend on optional features is key. First, list what you must have. Then, decide which “nice-to-haves” are really important to you. Ask yourself, do these features make your life better or just impress others?

Make a list of optional features you want, from 1 to 10. This helps you see what really matters. For example, a client wanted a home office but only used it twice a month. This was a waste of money.

Think about what you’ll enjoy now and later. A big lot might look good now but is it worth the upkeep? Be honest about your lifestyle when choosing:

- Updated kitchen with premium appliances

- Hardwood floors throughout

- Larger lot size or specific yard features

- Finished basement or bonus rooms

- Premium neighborhood amenities

- Architectural details or premium finishes

Your priorities should match your needs now and later. For example, a three-car garage might be too much for you. But it could be useful for storage or a workshop. When buying a house, extra features can cost more than you think.

“Learn More About: How to reduce debt before buying house effectively“

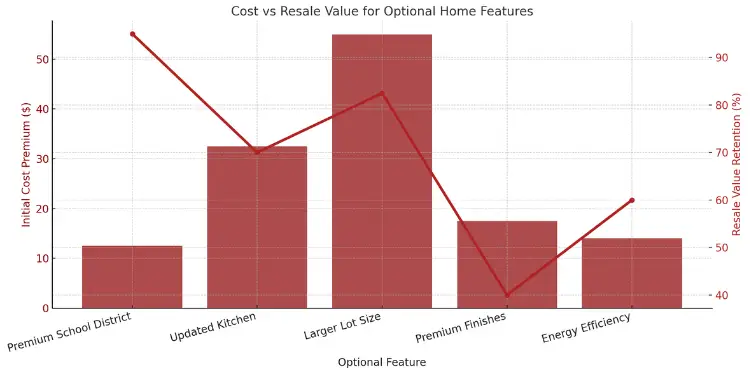

Future Resale Value Market Considerations

Think like an investor when buying a home. Some features always cost more, no matter the market. For example, 63% of buyers pay more for homes in good school districts, even without kids.

Features like waterfront views or mountain views are usually better investments. They hold their value longer than fancy kitchen designs. When choosing, balance what you want with what the market wants.

From my nine years helping first-time buyers, the best resale features are broad appeal ones. You can change flooring, but you can’t move your house or make your lot bigger.

| Optional Feature | Initial Cost Premium | Resale Value Retention | Buyer Appeal | Recommendation |

|---|---|---|---|---|

| Premium School District | 10-15% higher | Very High (90-100%) | Universal | Top priority if budget allows |

| Updated Kitchen | $15,000-$50,000 | Moderate (60-80%) | High | Worth investment if dated |

| Larger Lot Size | $10,000-$100,000+ | High (75-90%) | Varies by region | Better in growing areas |

| Premium Finishes | $5,000-$30,000 | Low (30-50%) | Subjective | Lowest priority for budget |

| Energy Efficiency | $8,000-$20,000 | Moderate (50-70%) | Growing | Increasingly important |

Think about now and later when ranking features. A big lot might need a lot of work but could be worth it. Energy-efficient features cost more upfront but appeal to those watching their budget.

Your ranked list helps you make choices when you have to cut costs. Clients who know what they want make quicker decisions. This helps avoid spending on things you don’t really need.

“The biggest regret I hear from homeowners isn’t about features they compromised on, but about overspending on features they rarely use while sacrificing location or fundamental structure.”

Remember, trends change. What’s popular today might not be tomorrow. Focus on features that will always be wanted, not just the latest trends.

“Further Reading: Free home buying budget worksheet for download“

Setting price caps for tradeoffs

Smart homebuyers set price caps for optional features to keep their budget in check. Without these limits, emotional choices can ruin your budget plan. I’ve seen many first-time buyers spend $50,000 more than planned for features they thought were nice but not essential.

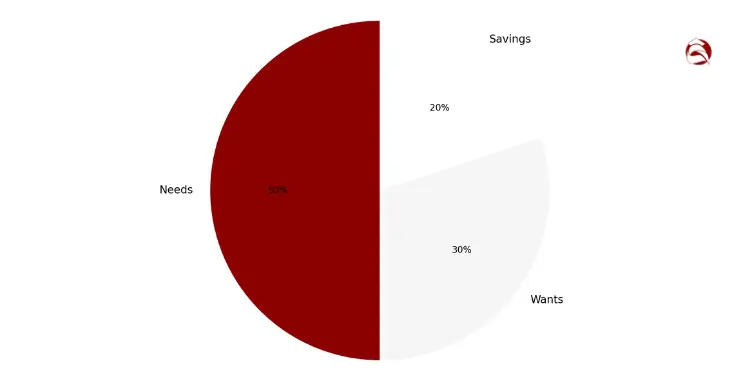

The 50/30/20 rule is a good way to balance needs and wants. It means 50% of your income goes to needs, 30% to wants, and 20% to savings or debt. This rule helps you pay for basic housing costs first, then think about extra features.

The CFPB-endorsed 50-30-20 framework directs 50 % of take-home pay to needs, 30 % to wants, and 20 % to savings or debt—an evidence-based ceiling for optional-feature spending.Ref.: “Consumer Financial Protection Bureau. (2022). Analyzing Budgets. CFPB.” [!]

Before looking at homes, make a detailed spreadsheet for optional features. This is your price cap worksheet. It shows how much extra you’re willing to pay for each feature. For example:

- How much more would you pay for an extra bedroom? $15,000? $25,000?

- What’s the premium school district worth to you in actual dollars?

- Is a renovated kitchen worth $10,000 more or $30,000 more?

- How much would you pay for a shorter commute time?

Use percentages of your total budget instead of fixed amounts. This way, your budget grows with your price range. For example, a garage might be worth 5% more, while granite countertops might be worth 1-2% more.

| Feature | Percentage Value | Dollar Value ($300K Home) | Monthly Payment Impact |

|---|---|---|---|

| Finished Basement | 5% | $15,000 | $80-90 |

| Updated Kitchen | 3-4% | $9,000-12,000 | $50-70 |

| Extra Bedroom | 7-8% | $21,000-24,000 | $110-130 |

| Premium Location | 10-15% | $30,000-45,000 | $160-240 |

This exercise helps you understand the real value of features. One client saved $42,000 by realizing a finished basement was worth $15,000, not more.

Every $10,000 increase in price adds $50-60 to your monthly payment. This helps you decide if extra features are worth the cost over 30 years.

Your home buyers needs and wants checklist is very useful. It keeps you focused on what’s important when you start to fall in love with a home.

The size of your down payment affects how much house you can buy. Buyers often choose between a large or small down payment. A bigger down payment can help you afford more features while keeping your monthly payments low.

“The most successful budget check happens before you ever step foot in a property. Once emotions get involved, financial discipline becomes ten times harder to maintain.”

Understanding your house price to income ratio is also key. Experts say your home should cost between 3-5 times your annual income. This ratio helps you avoid overspending, even when tempted by nice features.

Your price cap worksheet is vital during negotiations. It prevents you from spending too much on multiple features. Bring this document to every showing and use it when making offers. This simple tool has saved my clients thousands of dollars and avoided a lot of stress over nine years in Real Estate.

“Related Topics: Essential home buying budget checklist for new buyers“

Researching neighborhoods meeting priorities best

When looking at neighborhoods, using data helps find the best fit for you. In nine years of helping first-time buyers, I’ve seen neighborhood choice is often the toughest part. A good plan for checking neighborhoods can help avoid mistakes and make sure your home fits your needs now and later.

I suggest making a list to compare neighborhoods based on what matters most to you. This way, you can turn feelings into numbers, making your choice clearer. The best buyers I’ve worked with spend as much time on neighborhoods as they do on houses.

School Ratings Versus Distance Sacrifices

For families, good schools are a must. Buyers often choose schools over bigger houses or closer locations. This choice is important to think about.

Choosing a top school district costs more. Homes in these areas are 20-25% pricier. For a $300,000 home, that’s an extra $60,000-$75,000.

Think if the better schools are worth the extra cost. Some families find homes in lower-rated districts with special programs are better for their kids. Others might choose to spend their money differently, like on a bigger down payment.

A 2024 Realtor.com analysis found homes near top-rated elementary schools list at a 78.6 % premium, underscoring why location often outweighs cosmetic upgrades in long-term value.Ref.: “Realtor.com Research. (2024). School Housing 2024 Report. Realtor.com.” [!]

Crime Statistics and Insurance Impact

Safety matters a lot. A safe area might cost more in insurance, up to 40% more. This extra cost surprises many first-time buyers.

Look at crime stats from different places. Police websites and social media groups offer insights. Insurance agents can give you a quote before you buy.

One client saved $1,200 a year by picking a home just outside a high-crime area. The houses were similar, but the insurance was cheaper.

“Read More: Balancing needs vs wants home buying on a budget“

Walkability Amenities and Lifestyle Fit

Walkability is key for many buyers, like young people. Being able to walk to shops and parks saves money and improves life.

One family chose a smaller home in a walkable area over a bigger house. They saved $4,200 a year on gas and car costs. They also didn’t need two cars.

Walkable areas also mean more community events and friends. This is hard to put a price on, but it’s valuable.

| Neighborhood Factor | High Priority Impact | Medium Priority Impact | Low Priority Impact | Financial Consideration |

|---|---|---|---|---|

| School Quality | May require 20-25% higher budget | Consider specific programs vs. overall rating | Look at private options if budget allows | $50,000-75,000 premium on average home |

| Crime Statistics | Directly affects daily safety and security | Research trend lines, not just current rates | Consider security system investments | 30-40% higher insurance premiums |

| Walkability | Enables car-free lifestyle options | Provides convenience and community access | Enhances resale appeal to future buyers | $3,000-5,000 annual transportation savings |

| Commute Distance | Affects daily quality of life and time | Consider public transit options | Evaluate work-from-home flexibility | $0.58 per mile in vehicle costs plus time value |

Your research should narrow down neighborhoods to 3-5 options. This focused search helps avoid falling in love with the wrong house.

Remember, neighborhoods don’t change much quickly. Spending time on research is key to being happy with your home choice.

“You Might Also Like:

Making data driven compromise decisions

After finding out what you need and want, and researching areas, you’re ready to make choices. I’ve seen many buyers forget their plans when they see houses. This can lead to regret.

Make a decision matrix to score each house based on your criteria. When it’s hard to choose, look back at your needs and wants list. Don’t make quick decisions.

Your final checklist should have:

1) Check if your needs are met

2) See how many wants you get

3) Make sure it fits your budget

4) Think about if it will work for you in the future

5) Trust your gut

Money matters a lot in this process. Saving 20% can save you money on your mortgage. But, deciding to buy now or wait depends on your situation. Closing costs also vary, from 1.5% in the Midwest to 4% in the Northeast.

One client used a 1-3-5 rule for choosing lots and houses. They’d give up one extra feature for three must-haves or five top wants. This helped them make choices without getting stuck.

This method helps you buy a house that makes you happy and is smart financially. You’ll get a home that fits your life without spending too much.

{kind=link}