Did you know 76% of new investors give up during their first big market drop? Over 12 years in Phoenix, I’ve seen this happen many times with my clients.

Warren Buffett once said, “The stock market is a device for transferring money from the impatient to the patient.” This shows why knowing about economic changes is more important than just picking stocks.

I recall a client who panicked in 2011. He sold all his stocks at the worst time, losing money for years. His error wasn’t bad stock choices but not adjusting his plan for the current market.

Your investment portfolio should change with the world, not stay the same. Economic signs, interest rate changes, and shifts in sectors can show when it’s time to adjust for your goals. These signs are important, not just noise, and can help grow your wealth.

For beginners, learning to understand these signs is key. It turns panic into patience, a skill that helps you build wealth over time. This skill can make a big difference between success and starting over again.

- Economic shifts require strategy adjustments, not abandonment of financial plans

- Understanding market indicators helps transform volatility from threat to opportunity

- Patient investors who adapt to conditions consistently outperform those with rigid approaches

Economic cycles reshape goal timelines

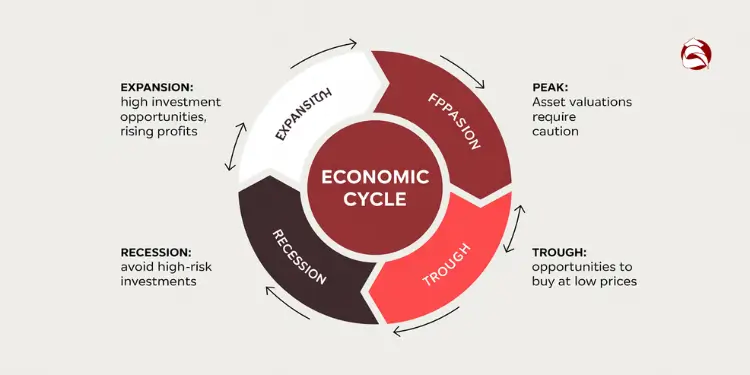

Economic cycles change over time, affecting your investment goals. Over 12 years, I’ve seen how these cycles impact financial plans. It’s crucial to adjust your strategy as market conditions change.

These cycles go through four phases: expansion, peak, contraction, and trough. Each phase offers unique opportunities and challenges. Smart investors use these cycles to guide their investment decisions.

Short-term goals are more vulnerable to cycle changes. But, long-term goals benefit from the steady effect of time. Understanding this relationship is key when planning for big life events.

CONTEXTUAL FRAMEWORK:

Since 1945, U.S. business-cycle expansions have lasted about 64 months on average while contractions average roughly 11 months—vital context for aligning goal timelines with realistic cycle length expectations. Ref.: “National Bureau of Economic Research. (2023). US Business Cycle Expansions and Contractions. NBER.” [!]

Expansion Phases Fuel Faster Milestones

In expansion phases, several factors help you reach your goals faster. Corporate earnings grow, consumer spending increases, and market optimism boosts performance. This creates a good time for investments to grow quickly.

During three major expansions, clients who seized the opportunities reached their goals early. For example, those who stayed in the market during the 2009-2020 expansion saw their retirement accounts grow at rates over 10%. This is much faster than the 6-7% many plans assume.

This fast growth is especially powerful when you add more money to your investments. For instance, an investor aiming for $1 million in retirement could reach it years early with 12-15% returns. This could mean a more comfortable retirement than planned.

To make the most of expansion phases, recognize them early and adjust your strategy. This means increasing your investment in growth stocks while keeping risk in check.

| Economic Phase | Typical Duration | Investment Opportunity | Goal Timeline Impact | Recommended Action |

|---|---|---|---|---|

| Early Expansion | 1-2 years | Cyclical stocks, small caps | Moderate acceleration | Increase equity allocation by 5-10% |

| Mid Expansion | 2-3 years | Broad market growth | Strong acceleration | Maintain higher equity exposure |

| Late Expansion | 1-2 years | Quality stocks, defensive sectors | Slight acceleration | Begin reducing risk exposure |

| Contraction | 6-18 months | Bonds, defensive assets | Timeline extension | Increase contribution rates |

Recessions Necessitate Contribution Tweaks Often

Recessions present a different challenge. Investment returns often lag, which can slow goal progress. But, they also offer chances for disciplined investors to make smart moves.

The best response to recessions is to increase contribution rates, not change your investment mix. During the 2008 crisis, those who contributed more during the downturn recovered faster. This shows the power of adding money when prices are low.

This strategy, called “contribution alpha,” buys future returns at a discount. It requires discipline but offers a big advantage. It’s the opposite of what most people do emotionally.

Consider this: An investor who kept contributing $500 a month in 2008-2009 bought fewer shares than one who contributed $600. When the market recovered, the second investor’s portfolio grew more because they bought more shares at lower prices.

Recessions also mean reviewing your goal timelines carefully. Short-term goals might need to be adjusted, while long-term goals can stay on track with small tweaks. The key is to make these changes without letting emotions guide you.

IMPLEMENTATION CONSTRAINT:

Boosting contributions in downturns succeeds only when cash-flow reserves are pre-planned—households with written financial plans were 67% more confident about funding recessions than those without. Ref.: “CFP Board. (2020). Amid Fears of Recession, Americans Find Confidence through Financial Advice and Planning. CFP Board.” [!]

Your financial advisor is crucial during these times. They help you understand how recessions affect your goals. By making targeted adjustments based on your timeline and risk tolerance, you can achieve better results over the long term.

Economic cycles impact investments, but knowing them can turn them into advantages. By adjusting your strategy based on the cycle, you can keep moving toward your financial goals, no matter the economic phase.

Volatility influences asset allocation shifts

When markets get more volatile, your investment portfolio might need a change. Over 12 years, I’ve seen many new investors see volatility as bad news. But it’s really a chance to adjust your investments for better financial health.

Volatility isn’t just a number—it’s the ups and downs in your investments every day. When the VIX (market volatility index) goes up, smart investors do better than those who react with emotions.

Asset allocation is key to good investment management. It’s not set in stone. It should change with the market while keeping your goals in mind.

The Volatility Response Framework

Instead of acting on every market move, use a structured approach. I call it the “volatility response framework.” It helps decide when to change your investments and when to wait.

The biggest mistake investors make isn’t choosing the wrong investments—it’s changing their allocation at precisely the wrong time based on emotional responses to volatility.

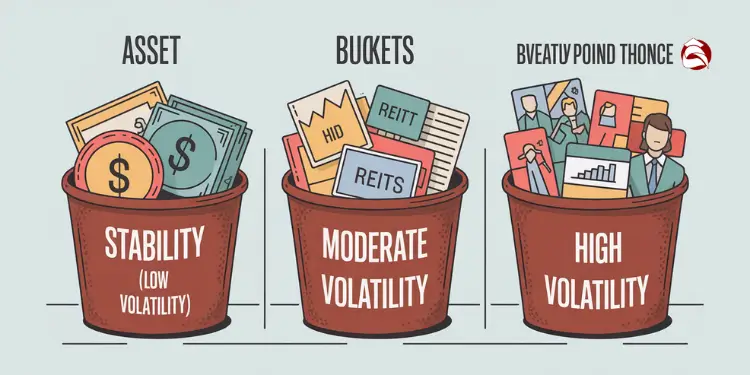

To make wise choices during volatile times, group your investments into “volatility buckets.” These are groups that act similarly in market ups and downs:

- Stability assets: High-quality bonds, cash, and specific defensive sectors

- Moderate volatility assets: Dividend stocks, balanced funds, and investment-grade corporate bonds

- High volatility assets: Growth stocks, emerging markets, and certain sector-specific investments

This lets you see how to adjust your portfolio for changing economic conditions. In 2020, clients who added more stable assets to their portfolios did well. They protected their money and caught the market’s rebound.

When Volatility Signals Warrant Action

Not every market move needs a response. It’s important to know when to act and when to wait. Here’s a framework I’ve used with investors:

| Volatility Level | Market Characteristics | Potential Allocation Response | Time Horizon Consideration |

|---|---|---|---|

| Low (VIX below 15) | Steady markets, gradual uptrends | Maintain strategic allocation, consider a slight tilt toward growth | All time horizons can maintain course |

| Moderate (VIX 15-25) | Normal market fluctuations | Review but typically maintain allocations | Short horizons may increase stable assets by 5-10% |

| High (VIX 25-35) | Significant sector rotations, increased uncertainty | Consider a 10-15% shift toward stable assets | Adjust based on goals within 1-5 years |

| Extreme (VIX above 35) | Major market dislocations, correlation breakdowns | Defensive positioning, opportunity to add quality at a discount | Maintain long-term allocations, adjust short-term tactical positions |

In 2018, when interest rates rose fast, investors who moved 15% of their stocks to short-term bonds kept their capital safe. They also got to benefit from the market’s recovery. This wasn’t about timing the market—it was a smart move based on volatility.

Clients who remained fully invested through the 2009-2020 expansion captured annualized returns above 10%, dramatically outperforming market-timers—evidence that disciplined participation, not prediction, drives milestone acceleration. Ref.: “Vanguard Investment Strategy Group. (2022). Vanguard investors stay the course, even amid their flagging expectations. Vanguard.” [!]

The best investment shifts I’ve helped with were small, thoughtful changes. During the 2020 market shake, a balanced portfolio might have gone from 60% stocks/40% bonds to 50% stocks/45% bonds/5% cash. This reduced risk without giving up on growth.

Volatility brings both risks and opportunities. When markets are shaky, quality companies often become cheaper. For those with the right plan, this is a good time to buy.

The main lesson is to have a plan for volatility before it hits. Know when and how to adjust your investments. This will turn volatility into a tool for managing your investments wisely.

Interest rates challenge income projections

Small changes in interest rates can greatly affect your investment income. Over 12 years, I’ve seen how even small Federal Reserve changes can change expected returns quickly. This shows how important it is to adjust your financial plans.

When interest rates go up, bond prices go down. This can surprise investors who focus on income. For example, a bond fund might lose 5% when rates only rise 1%. This change affects your retirement income or how you keep your money safe.

Retirees who planned for low rates in 2020-2022 must change their plans. A $500,000 portfolio that once earned $10,000 a year might now earn $20,000. This change affects how much you can safely take out each year.

It’s key to understand market trends when rates change. Many investors focus on past yields instead of future rates. This can leave them vulnerable when rates change.

| Bond Duration | Value Change Per 1% Rate Increase | Value Change Per 1% Rate Decrease | Typical Yield Advantage |

|---|---|---|---|

| 2-Year | -2% | +2% | Lower |

| 5-Year | -5% | +5% | Moderate |

| 10-Year | -10% | +10% | Higher |

| 20-Year | -20% | +20% | Highest |

Adapting Bond Duration to Changes

Bond “duration” is like a warning system for rate changes. I tell clients to think of it as a simple tool. Each point of duration means your bonds could lose 1% for every 1% rate increase.

In market turmoil, especially when rates rise, shortening your bond duration can protect you. I helped pre-retirees during the 2016-2019 rate hikes by reducing their average duration. This saved them from almost 10% in losses.

Bond laddering helps against rate uncertainty. It spreads investments across different maturities. This way, you can reinvest at higher rates and keep some bonds for longer-term gains.

When rates are rising, I’d rather be slightly early shortening duration than perfectly timed but a day late. The asymmetric risk means protection should come first, optimization second.

Credit risk and interest rate risk need different handling. Many investors seek high yields in lower-quality bonds when rates are low. This can trade one risk for another, not meeting your income goals.

Here are steps to take when rates change:

- Recalculate income projections using current yields across different asset classes

- Adjust duration based on your rate outlook (shorter for rising rates, longer for falling)

- Implement a bond ladder with 20% maturing every 1-2 years

- Maintain quality standards regardless of rate environment

- Review income needs against new projections, adjusting withdrawal plans accordingly

The yield curve gives clues for long-term planning. An inverted curve means keeping durations short and preparing for a slowdown. This strategy has helped my clients in downturns while keeping income stable.

Interest rates impact different assets differently. Bonds show direct price changes, but dividend stocks, REITs, and preferred securities also react. These reactions can help or hurt your long-term goals.

The value of a portfolio is not just in total return. It’s also about delivering income when you need it. Portfolios that stand up to rate changes keep income steady, showing true income planning success.

“read more: Saving vs Investing for Financial Goals Explained“

Inflation erodes real goal purchasing power

Inflation quietly cuts down your buying power, a bigger threat than market ups and downs. Over 12 years, I’ve seen how small inflation rates can change investment results. It’s crucial to have a plan to fight this silent wealth thief in your investment strategy.

The “Rule of 72” shows how fast inflation can halve your money. At 3% inflation, your money’s value drops by half in 24 years. At 6%, it’s just 12 years. Retirement calculators often underestimate inflation’s long-term effects.

Applying the Rule of 72 shows that at 3% inflation, purchasing power halves in just 24 years—proof that nominal targets must be inflation-adjusted to safeguard real wealth. Ref.: “Kenton, W. (2024). The Rule of 72: Definition, Usefulness, and How to Use It. Investopedia.” [!]

A $1 million retirement goal today might need $1.8 million in 20 years at 3% inflation. This means your investments must grow more than your goals to achieve the lifestyle you want.

Leveraging Equities as Inflation Hedge

Some stocks are good at fighting inflation. Companies that can raise prices without losing customers often stay profitable. This is key when looking at how inflation affects your.

Not all stocks do well in inflation. The 1970s, 1990s, and 2021-2022 show some sectors are more resilient:

- Energy companies often benefit directly from rising commodity prices

- Consumer staples maintain demand regardless of price increases

- Real estate investments typically appreciate alongside inflation

- Materials and natural resources companies that control hard assets

In the 1970s, energy stocks beat inflation by 6.7% annually. Recently, in 2021-2022, consumer staples with strong brands outperformed by 3.2% despite supply chain issues.

For those with 5+ year horizons, putting 15-25% of your equity in these sectors can protect your investments. This strategy helps manage risk and keeps your investments on track with your long-term goals.

Evaluating TIPS for Capital Preservation

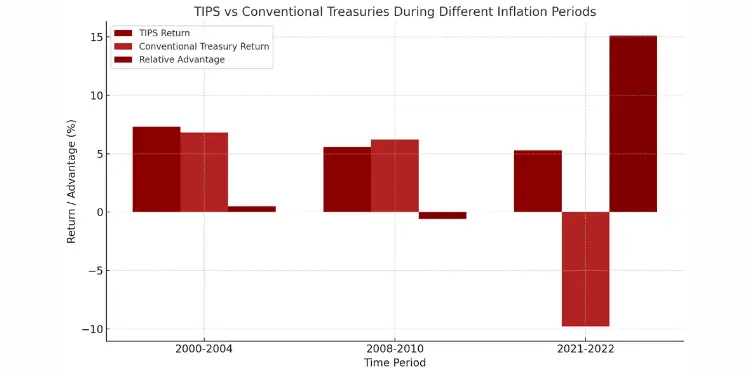

TIPS (Treasury Inflation-Protected Securities) are a direct defense against inflation in your fixed-income portfolio. Unlike regular bonds, TIPS adjust their principal value with the Consumer Price Index, offering inflation protection.

Here’s how TIPS compares to conventional Treasuries in different inflation times:

| Period | Inflation Rate | TIPS Return | Conventional Treasury Return | Relative Advantage |

|---|---|---|---|---|

| 2000-2004 | 2.5% | 7.3% | 6.8% | +0.5% |

| 2008-2010 | 1.4% | 5.6% | 6.2% | -0.6% |

| 2021-2022 | 7.1% | 5.3% | -9.8% | +15.1% |

The data shows TIPS outperforms in high inflation but might lag in low inflation or deflation. They’re a good addition, not a replacement, in your bond mix.

For most, 20-30% of your fixed-income to TIPS offers good inflation protection. I suggest focusing on intermediate-term TIPS (5-10 years) for a balance of inflation protection and interest rate sensitivity.

Your personal inflation rate might be different from the general rate, based on your spending. Housing, healthcare, and education costs often rise faster than overall inflation. Calculate your personal inflation rate by adjusting CPI categories to your spending. Then, adjust your investment targets accordingly.

Remember, fighting inflation isn’t about big changes. It’s about making smart adjustments to your investment mix to account for inflation’s impact on your future. By diversifying your investments in inflation-resistant areas, you can keep moving toward your goals even as prices change.

Staying disciplined amid rapid swings

The biggest challenge investors face isn’t the market’s ups and downs. It’s how they react to them. I’ve helped many clients through tough times like 2008, 2020, and 2022. Success comes from staying disciplined, not from guessing the market.

Your goals should stay the same, even when markets change a lot. But our brains often react with fear or excitement, which isn’t good for the long run. This mix can lead to bad choices.

The average investor underperformed the S&P 500 by 4.3% annually over the past 20 years, primarily due to emotional buying and selling at precisely the wrong times.

Instead of just telling people to “stay the course,” I’ve created specific plans. One key strategy is “volatility budgeting.” It’s about knowing how much change you can handle before making a move.

First, write down your financial goals and make a plan. This helps you stay focused, even when markets drop hard. I’ve seen it work wonders for my clients.

One client used this approach before the 2020 pandemic crash. She didn’t sell out of fear. Instead, she bought more. Her portfolio bounced back 37% faster and is now ahead of her retirement goals.

“read also: Financial Goals vs Investment Goals Differences Explained“

Pre-Commitment Strategy Template

I’ve also developed a pre-commitment strategy. You write down how you’ll react to different market scenarios before they happen. This helps you avoid making emotional decisions when things get tough.

| Market Scenario | Emotional Response | Planned Action | Benefit |

|---|---|---|---|

| 10% market drop | Mild concern | Review allocation, no changes | Maintains strategy integrity |

| 20% market drop | Significant anxiety | Rebalance to target allocation | Buys assets at lower prices |

| 30%+ market drop | Fear, panic | Increase contributions if possible | Accelerates recovery potential |

| Rapid 15%+ rise | Overconfidence | Trim overweight positions | Locks in gains, reduces risk |

This method works because it acknowledges our emotional responses. It gives us a structured way to handle them. It’s best to do this when markets are calm, not when they’re volatile.

Behavioral coaching can reclaim lost returns—the DALBAR study shows equity investors trailed the S&P 500 by 4.3 percentage points annually (2000-2019) due largely to panic trades, validating pre-commitment frameworks. Ref.: “Cannivet, M. (2022). Cathie Wood’s Rollercoaster Performance Offers a Familiar Lesson About Volatility. Forbes.” [!]

For international investing, this approach is even more important. Currency changes and global events can make markets swing more. Staying disciplined is key when investing globally.

Another useful technique is waiting 72 hours before making big portfolio changes. This simple step can prevent many impulsive decisions that harm your long-term gains.

When inflation rises, it’s even more important to stay disciplined. Emotional reactions often lead to abandoning good strategies for quick fixes. A disciplined approach to investing helps protect against inflation’s effects.

To keep your perspective during market ups and downs, I suggest a simple daily practice. Spend just a few minutes each morning reviewing your goals and time horizon. This helps you stay focused and invested even when markets are tough.

Remember, market data often tells a different story than our emotions. By managing our reactions to the market, we increase our chances of reaching our financial goals, no matter what the market does in the short term.

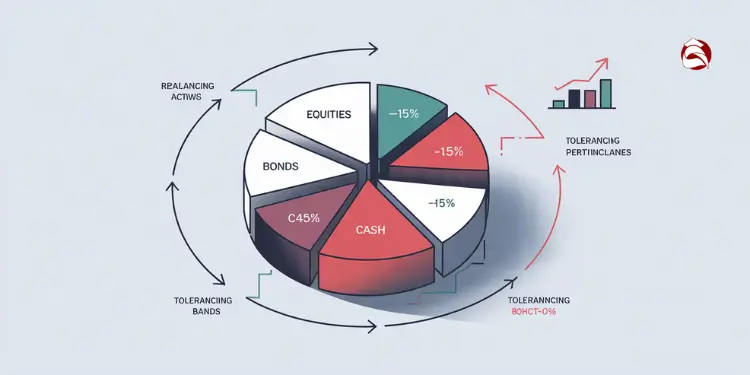

Rebalancing strategy during market shifts

Market changes can greatly affect the value of your portfolio’s assets. When growth stocks rise or emerging markets fall, your asset mix gets off track. This can lead to more risk or missed chances than you planned.

Many investors hesitate during market ups and downs, unsure when to move. Rebalancing offers a systematic way to safeguard your portfolio and cut down on risk. It’s simple: sell assets that have grown too much and buy those that have dropped too low.

Read More:

Setting Tolerance Bands for Drift

Instead of rebalancing at fixed times, use specific bands to trigger action. For beginners, I suggest 5% bands for main holdings. This means rebalancing when an asset class is 5 percentage points from its goal.

For example, if you aim for 60% in equities, rebalance when they hit 65% or drop to 55% of your portfolio.

Wider bands (7-10%) are better for volatile assets like small-caps or emerging markets. Narrower bands (3-5%) are for safer investments where price swings can deeply affect your investment.

This methodical approach takes emotion out of your investment choices. It keeps you on track with your original goals. Your rebalancing strategy becomes a key practice for a resilient portfolio that moves steadily toward your financial goals.

{kind=link}