Creating a solid financial plan for your first property doesn’t have to be scary. Did you know 40% of first-time buyers go over budget because they forget important costs? “The difference between homebuyers who sleep well and those who don’t often comes down to proper financial preparation,” my mentor always said.

After helping hundreds of new buyers, I’ve seen how a good spending plan changes anxiety to confidence. Most Americans underestimate closing costs by $5,000-$10,000, says the National Association of Realtors.

Knowing the whole financial picture means understanding hidden costs of buying a house that surprise many. Your prep today stops payment shock tomorrow.

My clients who spend one evening on their numbers get better mortgage terms and negotiate stronger.

Quick hits:

- Calculate true monthly payment obligations

- Factor in all closing expenses

- Plan for maintenance and repairs

- Consider neighborhood-specific property taxes

- Prepare emergency housing fund reserves

List all upfront home purchase expenses

Before you get your new home, you’ll face many upfront costs. These costs are more than just the down payment. In Greenville, I’ve seen deals fall apart because buyers didn’t know about these costs. Let’s look at what you need to budget for before you make an offer.

The first step is figuring out how much house you can afford. You’ll need to get pre-approved by a lender. They’ll check your income, debt, and credit score to see how much you can borrow. This step helps you avoid falling in love with homes that are too expensive.

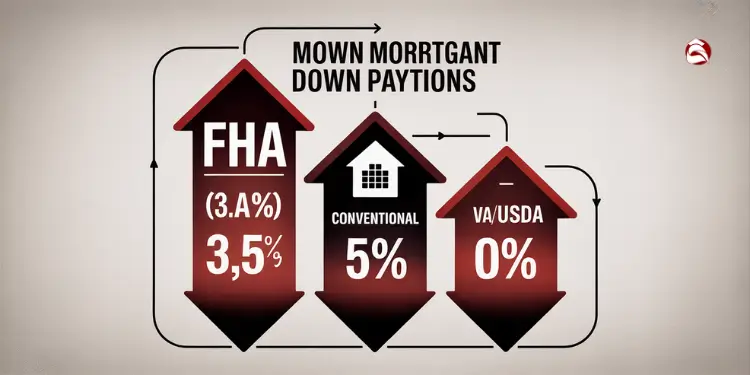

Your down payment is usually the biggest cost. You might think you need 20% down, but you have other options:

- FHA loans: Typically require 3.5% down

- Conventional loans: Usually start at 5% down

- VA loans: May offer 0% down for qualifying veterans

- USDA loans: Can provide 0% down in eligible rural areas

Putting less than 20% down means you’ll pay for private mortgage insurance (PMI). This adds to your monthly payment. Your mortgage rate also depends on your down payment. Generally, a bigger down payment gets you a better rate.

“Check This Out: Cost breakdown buying house for first time buyers

Include Inspection, Appraisal, and Closing Fees

There are many professional services needed during the home buying process. A home inspection costs $300-$500 and finds any problems. I’ve seen clients save thousands by finding issues early.

The appraisal costs $450-$650 and checks if the home’s value matches the price. If it’s lower, you might need to pay more, negotiate, or walk away.

Earnest money shows you’re serious about your offer. It’s usually $1,000-$5,000 and becomes part of your down payment if the sale goes through. But, it’s at risk if you back out without a good reason.

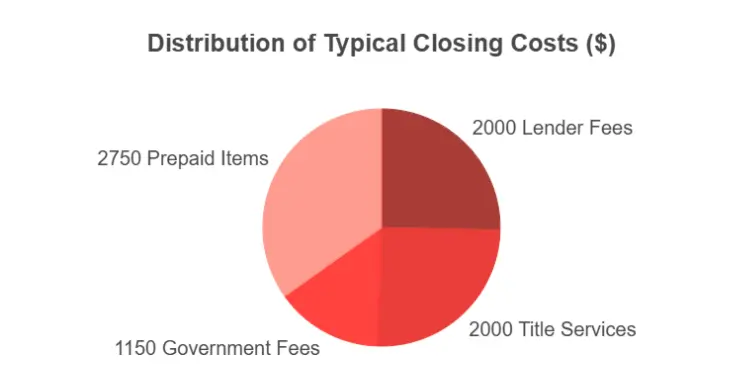

Closing costs are many and surprise first-time buyers. They’re 2-5% of your loan amount and include:

| Closing Cost Category | Typical Range | What It Covers | Can It Be Negotiated? |

|---|---|---|---|

| Lender Fees | $1,000-$3,000 | Application, origination, credit report | Sometimes |

| Title Services | $1,500-$2,500 | Title search, insurance, settlement | Rarely |

| Government Fees | $800-$1,500 | Recording fees, transfer taxes | No |

| Prepaid Items | $1,000-$4,500 | Insurance escrow, tax escrow, interest | No |

Don’t forget to budget for moving costs, which can be $800 for local moves or $5,000+ for long-distance moves. You might also need money for changing locks, utility deposits, and repairs before moving in.

Moving expenses can vary widely. On average, a local move costs about $1,250, while long-distance moves average $4,890 for a 2–3 bedroom home. These figures can fluctuate based on distance, home size, and additional services required. Ref.: “Moving Cost Calculator for Moving Estimates | Moving.com.” [!]

The best first-time buyers make a detailed budget two months before making offers. This way, they avoid last-minute money scrambles that can ruin deals.

A home affordability calculator can help you plan your budget. But, remember to include all upfront costs. This will help you figure out how much you can spend on your home.

When you get loan estimates, check the closing costs section carefully. Some lenders offer credits to help with these costs. This might be a good deal if you’re short on cash but can handle a slightly higher monthly payment.

“Related Articles: How to determine home buying budget for beginners

Add recurring mortgage related obligations

When you buy a home, your monthly payment is more than just the price. It includes other costs that affect how much you can spend. Knowing these costs helps you figure out how much house you can afford before you make an offer.

The mortgage world uses PITI to talk about your monthly payment. Let’s break it down:

- Principal: This part pays down your loan balance.

- Interest: The fee for borrowing money, based on your rate and credit score.

- Taxes: Monthly property taxes held in escrow until due.

- Insurance: Homeowners insurance to protect your property.

Your interest rate greatly affects how much house you can afford. A 0.5% difference can change your monthly payment by $100 or more. So, improving your credit score before applying for a mortgage can save you thousands.

Even a 0.5% change in mortgage interest rates can significantly impact monthly payments. For instance, on a $300,000 loan, a 0.5% increase can add approximately $84 to the monthly payment, totaling over $30,000 more over a 30-year term. Ref.: “Mortgage Closing Costs Explained: How Much You’ll Pay – Forbes.” [!]

If you put down less than 20% of the home price, you’ll need to add Private Mortgage Insurance (PMI). This costs 0.5% to 1% of your loan amount annually, split into monthly payments. On a $300,000 loan, that’s an extra $125-250 monthly until you have 20% equity.

Many areas have Homeowners Association (HOA) fees that can affect your budget. I’ve seen buyers in Greenville communities pay $200 to $400 monthly for these fees. Always check these costs before deciding how much you can afford.

Homeowners Association (HOA) fees can range from $200 to $400 monthly, depending on the community and amenities offered. These fees are typically non-negotiable and can increase over time, affecting long-term affordability. Ref.: “What are Mortgage Closing Costs? – NerdWallet.” [!]

| Payment Component | Typical Cost Range | Payment Frequency | Budget Impact |

|---|---|---|---|

| Principal & Interest | Varies by loan amount | Monthly | Core payment determined by home price and interest rate |

| Property Taxes | 0.5-2.5% of home value annually | Collected monthly in escrow | Varies significantly by location |

| Homeowners Insurance | $800-1,500 annually | Collected monthly in escrow | Required by lenders |

| PMI (if down payment | 0.5-1% of loan amount annually | Monthly | Temporary until 20% equity reached |

| HOA Fees (if applicable) | $200-400 monthly | Monthly | Permanent expense, may increase annually |

When figuring out how much to spend on a home, follow the 28/36 rule. Your mortgage payment shouldn’t be more than 28% of your monthly income. And your total debt payments shouldn’t be over 36%.

If your income is not steady, use the lowest amount you’ve made in the past few months as your budget. You can always add more to your savings or other goals if you make more in a month.

One strategy I’ve seen work is “payment practice.” For three months before buying, save the difference between your rent and your expected mortgage payment. This builds savings and checks if you can handle the higher payment.

Remember, your lender will tell you how much you can borrow. But you don’t have to spend that much on a home. Being careful with your budget helps you deal with unexpected expenses and prevents you from being “house poor.”

“Related Articles: House hacking first home guide for new buyers

Estimate yearly maintenance and repairs cost

Homeownership costs more than just your monthly mortgage. You’ll also face maintenance costs that renters don’t have. This includes fixing leaks, replacing carpets, and updating appliances.

Set aside 1-3% of your home’s price each year for upkeep. For a $300,000 home, that’s $3,000 to $9,000 yearly. This means $250 to $750 each month. Newer homes usually need less money, but older homes might cost more.

Home maintenance costs can be substantial. Research indicates that homeowners spend about £627 monthly on upkeep, which is approximately two-thirds of the average mortgage payment. This highlights the importance of budgeting for ongoing maintenance. Ref.: “Home maintenance costs reach two thirds of average mortgage – The Times.” [!]

This budget isn’t just for emergencies. It also covers regular tasks like cleaning gutters and mowing the lawn. Having a special “home maintenance account” helps keep these costs separate from your emergency fund.

“Related Articles: Essential home buying budget checklist for new buyers

Factor HVAC, Roof, and Appliance Lifespan

Big home systems have set lifespans. Planning for their replacement is key. Without a plan, you might end up paying high interest rates for new systems.

Your HVAC system lasts 15-20 years and costs $5,000 to $10,000 to replace. Roofs last 20-30 years and cost $8,000 to $20,000. Appliances need replacing every 10-15 years, costing $4,000 to $8,000 for a kitchen and laundry set.

Start a “home systems fund” by dividing the cost by the system’s life. For example, if your furnace costs $6,000 and has 10 years left, save $600 a year or $50 monthly. This makes big expenses easier to manage.

Major home systems have varying lifespans and replacement costs. For example, HVAC systems last 15–20 years and can cost $5,000–$10,000 to replace, while roofs last 20–30 years with replacement costs ranging from $8,000 to $20,000. Planning for these expenses is crucial for long-term home maintenance. Ref.: “10 different types of roofing – and how to pick the best one for your home – Homes & Gardens.” [!]

| Home System | Average Lifespan | Replacement Cost | Annual Savings Needed | Monthly Contribution |

|---|---|---|---|---|

| HVAC System | 15-20 years | $5,000-$10,000 | $333-$667 | $28-$56 |

| Roof | 20-30 years | $8,000-$20,000 | $267-$1,000 | $22-$83 |

| Water Heater | 8-12 years | $700-$2,000 | $58-$250 | $5-$21 |

| Major Appliances | 10-15 years | $4,000-$8,000 | $267-$800 | $22-$67 |

| Exterior Paint | 5-10 years | $3,000-$6,000 | $300-$1,200 | $25-$100 |

“Check This Out: How to track home buying expenses during the process

Budget Yearly Property Tax Increases

Property taxes rarely stay the same. They usually go up 2-3% each year. Sometimes, reassessments can cause bigger jumps.

Plan for a 4% annual increase in property taxes to be safe. For a $3,000 tax bill, that’s $120 more the next year. This helps avoid surprises when tax bills come.

Property taxes have been on the rise. Between 2022 and 2023, homeowners saw an average increase of 4.1% in property taxes, with some areas experiencing up to a 31% hike. This trend can impact long-term housing affordability. Ref.: “Here’s where U.S. homeowners pay the most — and least — in property taxes – CBS News.” [!]

Homeowners insurance also goes up 3-5% yearly. This is due to inflation, claims, and risk changes. These small increases can add hundreds to your monthly costs over time.

Some places offer tax breaks for primary homes. Check with your county tax assessor for these programs. First-time buyers often get extra breaks.

Remember, tax increases can change your monthly payment if you have an escrow account. Your mortgage servicer will adjust your payment yearly to cover these increases. This can change your payment even with a fixed-rate mortgage.

Read More: How to budget for closing costs in advance

Allocate buffer for unexpected contingencies

Creating a financial buffer for unexpected things is very important when buying a home. I’ve helped many first-time buyers for nine years. They often face surprises that can stress them out.

It’s wise to save 3-5% of your home’s price for unexpected costs. For a $300,000 home, that’s $9,000 to $15,000. This money helps when surprises happen.

First-year homeowners often face costs they didn’t expect. Things like foundation problems or water damage can happen. Even a big tree might need to be removed after a storm.

Life can also throw surprises. Job changes, medical bills, or family emergencies can affect your mortgage payments. It’s smart to have an emergency fund for 3-6 months of housing costs before buying a home.

One of my clients in Greenville didn’t want to save for a buffer. She wanted to use all her money for the down payment. But, she faced a job change and a big plumbing problem three months later. Her buffer saved her from a bad situation and kept her credit score safe.

When planning your budget, use the 28% Rule. This means your mortgage shouldn’t be more than 28% of your income. FHA loans let you go up to 31%. Staying within your budget makes your home more affordable.

Before getting a mortgage, think about your spending habits. Do you have other debts you could pay off first? Paying off debts can lower your monthly costs and help with housing expenses.

| Contingency Type | Recommended Amount | Covers | Timeline |

|---|---|---|---|

| Home Repair Buffer | 3-5% of purchase price | Structural issues, appliance failures, emergency repairs | Immediate access |

| Emergency Fund | 3-6 months of housing costs | Job loss, medical issues, family emergencies | Separate from repair fund |

| Annual Maintenance | 1-2% of home value yearly | Regular home maintenance, minor repairs | Ongoing contribution |

| Rate Change Buffer | 2-3 months of payment difference | Adjustable rate increases, tax/insurance changes | Before first adjustment period |

Smart buyers save for a down payment and a contingency fund at the same time. Automatic transfers to separate accounts help. Even small weekly amounts add up and teach you to save.

A lower interest rate can save you money over time. Every 0.25% less interest can save thousands. These savings can help fund your contingency without stretching your budget.

Having a contingency plan gives you peace of mind. When a big home maintenance issue comes up, you’ll be ready. This buffer turns unexpected problems into manageable ones.

Read More: How to stick to home buying budget without fail“

Prioritize spending categories by importance

Smart homebuyers know that not all budget categories are the same. When I help first-time home buyers, I teach them to make a budget that works. It’s not just about numbers; it’s about where your money goes.

Your budget should match your financial situation and goals. You need to decide which expenses are must-haves and which can wait. Let’s look at how to do this well.

Apply Needs Wants Tradeoff Method

Understanding the difference between needs and wants is key to a good budget. The needs vs wants tradeoff helps you decide how much house you can afford.

First, sort all expenses into three groups:

- Non-negotiable needs: Mortgage, taxes, insurance, utilities

- Important needs: Maintenance, HOA fees, emergency repairs

- Wants: Cosmetic upgrades, new furniture, landscaping

I’ve helped many clients sort their priorities. This helps avoid disappointment and financial trouble later.

Remember, your lender cares about your monthly payments, not your furniture. Focus on the basics first, then on looks.

Many find the 50/30/20 rule helpful for homeowners. It suggests:

- 50% for fixed costs (mortgage, taxes, insurance)

- 30% for variable expenses and small upgrades

- 20% for savings and emergencies

If this doesn’t fit, try the 60/30/10 rule. The exact numbers don’t matter as much as the discipline.

When you’re tight on money, make smart tradeoffs. Maybe choose a longer commute for a cheaper area. Or pick a smaller home with room to grow. Delaying cosmetic fixes can help you make a bigger down payment.

| Budget Category | Priority Level | Example Items | Typical Percentage |

|---|---|---|---|

| Mortgage & Insurance | Highest | Principal, interest, taxes, insurance | 28-33% of income |

| Maintenance Reserve | High | HVAC service, roof repairs, plumbing | 1-3% of home value annually |

| Utilities & Services | Medium-High | Water, electricity, internet, trash | 5-10% of income |

| Home Improvements | Medium | Paint, flooring, fixtures | Variable based on needs |

| Décor & Furnishings | Low | Furniture, window treatments, art | Defer until essentials covered |

A calculator can show how much home you can afford. But it can’t decide what’s important to you. That’s where budgeting comes in.

I helped a couple who wanted a home in a certain school district. They used the needs-wants method to find a smaller home that needed updates. They budgeted for repairs first and planned for looks later.

Remember, your budget should be flexible. What you want now might become a need later. And what you need now might be something you can wait on.

The secret to a good budget is knowing what’s important to you. This way, buying a home is easier and less stressful in the long run.

Read More:

Synchronize budget timeline with buying process

To know how much house you can buy, you need a timeline. Make a 6-month plan that matches your homebuying steps. This will help you manage your money better.

First, use a home affordability calculator to figure out your budget. In the first two months, save for your down payment and closing costs. This is the start of your financial journey.

Next, months 3-4 are for getting pre-approved for a mortgage. This will help you know how much you can spend. You’ll see what price range is right for you.

Months 5-6 are for saving for earnest money, inspection, and closing costs. This way, you’ll have enough money when you find a house. It’s important to save for all the costs.

Keep your savings in a special account for buying a home. I use the EveryDollar app, but a simple spreadsheet works too. It’s key to have a plan for all the costs of buying and keeping a home.

Check your budget every week as you move forward. This way, you won’t run out of money for something important. With a good plan, you’ll be ready for every step of buying a home.

{kind=link}