Setting clear long term investment goals is key to financial security for decades. Beginners who set specific targets do better than those who just “save for later.” Ever wonder why some investors stay calm during market ups and downs while others freak out?

A surprising 65% of Americans who set clear financial targets do better than those without goals. Warren Buffett said, “Someone’s sitting in the shade today because someone planted a tree long ago.”

In my twelve years helping investors, I’ve seen a big difference. Those with detailed plans build wealth, while those without drift without making progress.

Creating a personal financial plan with specific goals turns dreams into real plans. This helps keep focus when markets change.

Quick hits:

- Retirement funding with calculated milestones

- Home purchase with timeline strategy

- Education funding with growth projections

- Legacy planning with tax considerations

Vision Planning for Multi Decade Wealth

Building wealth over many years starts with a clear vision. This vision is like a compass for your money. In 12 years, I’ve seen that those with clear goals do better than those without.

Having a clear goal is key. Instead of saying “I want to retire,” say “I need $1.2 million by age 60 for $60,000 a year.” This clear goal helps you stay focused and track your progress.

The most successful investors I’ve worked with don’t just dream about financial independence—they map it with precision, review it quarterly, and adjust annually.

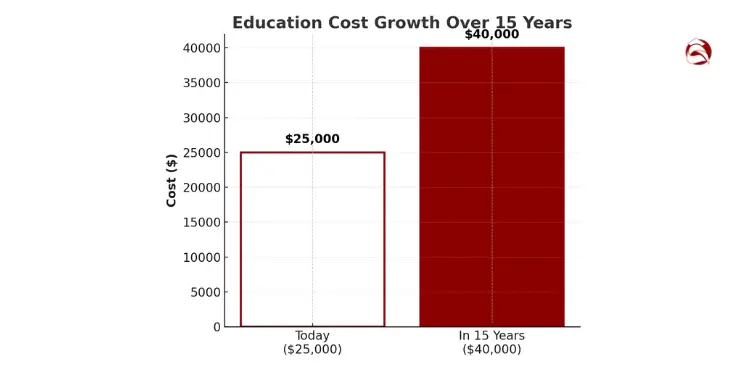

To start your wealth vision, work backward from your goals. Use inflation rates to figure out today’s investment needs. For example, a $25,000 college cost today will be over $40,000 in 15 years.

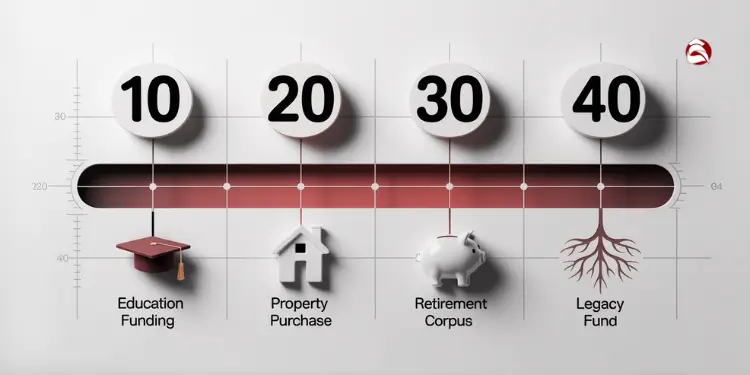

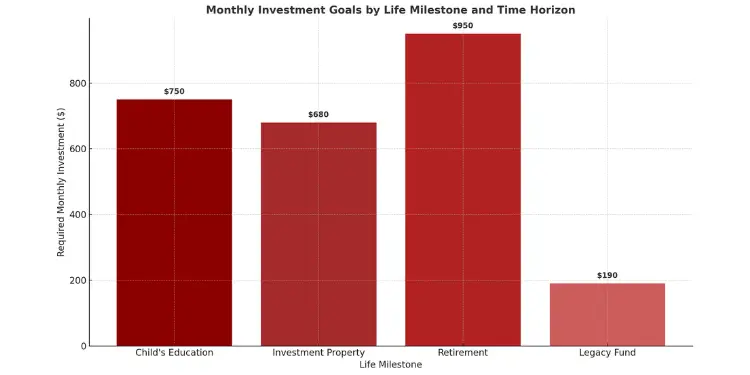

Your vision should have milestones for different times. Here’s how to set these goals:

| Time Horizon | Life Milestone | Financial Target | Required Monthly Investment |

|---|---|---|---|

| 10 Years | Child’s Education | $120,000 in 529 Plan | $750 at 6% return |

| 20 Years | Investment Property | $300,000 down payment | $680 at 7% return |

| 30 Years | Retirement | $1.2M in retirement accounts | $950 at 7% return |

| 40 Years | Legacy Fund | $500,000 for heirs/charity | $190 at 7% return |

Your vision must change with the market and your life. Review it every quarter and adjust yearly for big changes.

A good wealth vision includes:

- Specific financial targets with target dates

- Required investment amounts and expected returns

- Major life transitions mapped against investment phases

- Inflation assumptions for each goal

- Risk tolerance adjustments for different time horizons

This vision helps you make smart choices. It tells you if buying a vacation home is right or if you should save more for retirement.

Many find clarity in their vision makes daily money choices easier. It reduces worry about making the right financial decisions.

Now, write down your wealth vision this week. Even a simple page with goals and dates will help you reach your goals. By retirement, you’ll be glad you started planning early.

“Check This Out: How to Stick to Your Investment Goals“

Building Retirement Corpus with Discipline

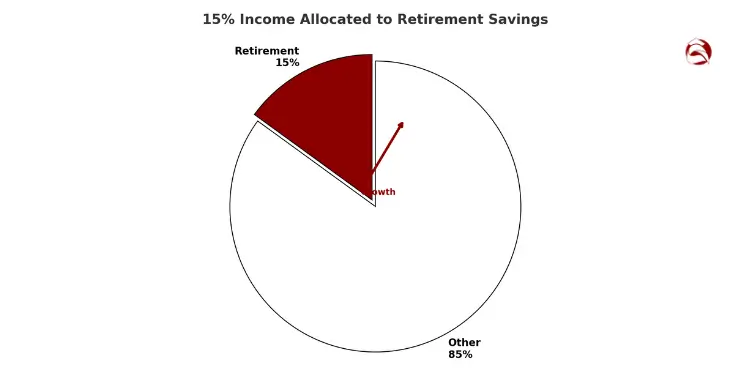

Building a strong retirement fund is key to financial security. Only 36% of non-retirees think they’re saving enough. This shows how important it is to plan well.

Start by saving 15% of your income for retirement. If that’s too much, begin with what you can. The goal is to keep saving regularly and have a clear plan.

When asked when to start saving, I say now. The sooner you start, the more time your money has to grow. Even small amounts can add up over time.

“Learn More About: How to Catch Up on Investment Goals if Behind“

Maximizing Tax Advantaged Account Contributions

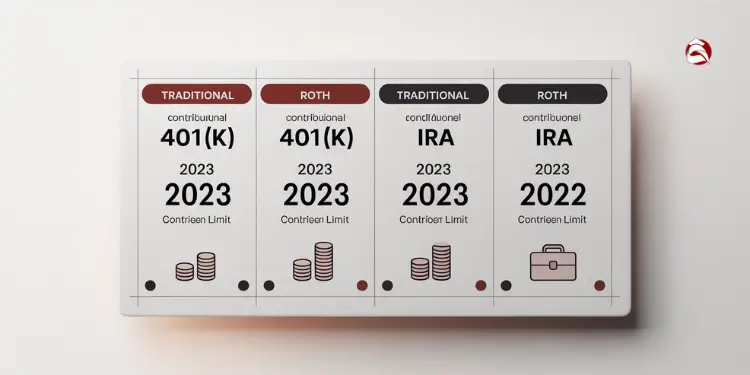

Tax-advantaged accounts are great for saving for retirement. In 2023, you can contribute up to $22,500 to a 401(k) and $6,500 to an IRA. If you’re over 50, you can add more.

First, make sure to use every dollar of employer matching in your 401(k). This is free money. Most employers match 50-100% of your contributions on the first 3-6% of your salary.

After getting the employer match, think about these accounts:

| Account Type | Tax Advantages | Best For | 2023 Contribution Limit | Access Considerations |

|---|---|---|---|---|

| Traditional 401(k) | Pre-tax contributions; tax-deferred growth | Higher current income brackets | $22,500 ($30,000 if 50+) | Penalties for early withdrawals; RMDs at 73 |

| Roth 401(k) | After-tax contributions; tax-free growth | Lower current income brackets | $22,500 ($30,000 if 50+) | Tax-free withdrawals in retirement |

| Traditional IRA | Potentially deductible; tax-deferred growth | Self-employed or supplemental savings | $6,500 ($7,500 if 50+) | Income limits for deductibility |

| Roth IRA | After-tax contributions; tax-free growth | Long-term growth; tax diversification | $6,500 ($7,500 if 50+) | Income eligibility limits; flexible withdrawals |

I suggest using both pre-tax and Roth accounts. This way, you can manage your taxes better in retirement. It helps you keep more money in your pocket.

“For More Information: Financial Goals vs Investment Goals Differences Explained“

Employing Dollar Cost Averaging Tactics

Dollar cost averaging (DCA) is a smart way to invest. It means investing a fixed amount regularly, no matter the market. This method helps you avoid making emotional decisions based on market ups and downs.

By investing the same amount every time, you buy more shares when prices are low and fewer when they’re high. This can lower your average cost and help your money grow more over time.

Vanguard’s multi-market analysis shows that disciplined dollar-cost averaging outperformed lump-sum investing in 66 % of volatile equity market scenarios, lowering entry-point risk while preserving long-term growth potential.Ref.: “Aliaga-Díaz, R. & Sokolova, A. (2023). Cost Averaging: Invest Now or Temporarily Hold Your Cash? Vanguard Research.” [!]

Here’s how to use dollar cost averaging:

- Figure out how much you can save now

- Set up automatic transfers to your retirement accounts

- Gradually increase your savings by 1% each year

- Keep going until you save 15-20% of your income

- Stay disciplined, even when the market is volatile

One client who used this strategy during the 2008 crisis ended up with more wealth than others. This shows how effective it can be.

For the best results, use dollar cost averaging with a mix of investments. This mix helps manage risk and grow your wealth over time. It’s a key part of long-term financial success.

Retirement planning is about more than just saving money. It’s about creating a steady income for your future. By saving now, you’ll have more freedom and security later.

“Further Reading: How to Adjust Investment Goals Over Time“

Funding Children Education Future Costs

Planning for your kids’ education is a big goal. It needs careful planning and regular action. Unlike retirement, education funding has a strict timeline. It ends when your child goes to college.

The cost of college keeps going up fast. Tuition rises by 5.2% each year. Knowing your time frame is key to figuring out how much to save.

College costs are very high. Public universities cost $27,940 a year. Private schools cost $57,570. Over four years, this adds up to a lot of money.

I help many families plan for college. The best way is to start early and know your options. Each choice has its own benefits.

| Education Funding Vehicle | Tax Advantages | Investment Options | Control Considerations | Contribution Limits |

|---|---|---|---|---|

| 529 Plans | Tax-free growth and withdrawals for qualified expenses; possible state tax deduction | Age-based portfolios, fixed allocation options, FDIC-insured options | Parent maintains control; minimal impact on financial aid | High limits ($16,000 annual gift tax exclusion; up to $80,000 with 5-year election) |

| Coverdell ESAs | Tax-free growth and withdrawals for qualified expenses (K-12 and college) | Wide range of investment options including individual stocks and bonds | Assets transfer to student at age 18-30 (varies by state) | Limited to $2,000 annually; income restrictions apply |

| UTMA/UGMA Accounts | First $1,100 of investment income tax-free; next $1,100 at child’s rate | Unrestricted investment options | Assets legally belong to child at age of majority | No contribution limits; subject to gift tax rules |

| Roth IRAs | Tax-free withdrawals of contributions anytime; earnings can be withdrawn penalty-free for education | Unlimited investment options | Maintains retirement purpose if education funding isn’t needed | $6,000 annually ($7,000 if over 50); income restrictions apply |

| Traditional Savings | No specific tax advantages | Unrestricted investment options | Complete flexibility for changing goals | No limits |

Creating a plan for college funding is important. It should balance with other financial needs. I suggest saving 5-15% of your portfolio for education, based on family size and retirement goals.

To figure out how much to save each month, consider your child’s age, the college type, and your expected contribution. Starting early helps a lot. Saving from birth can cut your monthly needs by almost half.

Many parents feel stressed about saving for college. But, you don’t have to save everything. Scholarships, grants, and work-study can help a lot.

Unexpected costs can mess up your college savings plan. Having a small extra amount can help. Aim to save 110-120% of what you think you’ll need.

For most families, saving for college is a 5-18 year goal. This time frame lets you invest more aggressively. As college gets closer, switch to safer investments to protect your savings.

Start planning for college today. Look into your state’s 529 plan benefits and limits. Many states offer tax breaks for contributions. Set up automatic monthly savings, even if it’s a little bit.

Creating Legacy and Estate Planning Targets

Planning for the future is more than just for you. It’s about leaving a lasting legacy that shows your values and helps your loved ones. Legacy planning changes how you invest, moving from just for you to for your family’s future.

An estate plan is like a map for your financial legacy. Right now, you can leave up to $12.92 million tax-free (2023). But, this number will drop to about $6 million in 2026. This change means many families need to plan quickly.

Legacy goals are more than just money. When helping clients, I focus on three areas:

- Financial assets – Things like money, property, and businesses

- Knowledge transfer – Passing on money smarts, family values, and business skills

- Charitable impact – Giving to causes and setting up foundations

Life changes can affect your legacy plan. Getting married, having kids, or selling a business can change what you need. It’s smart to check your plan with a financial advisor every year.

“The greatest use of life is to spend it for something that will outlast it.” – William James

Setting clear legacy goals is important. Instead of just saying “I want to leave money to my kids,” plan specifics. This could be:

- Helping your grandkids with college through 529 plans

- Planning for your business to pass on smoothly

- Setting up charitable funds to make a big impact

- Keeping the family home in the family

Each goal needs different investments. For college funds, you might choose investments that grow over 15-20 years. For giving to charity, a mix of income and growth investments works well.

Incorporating Trusts for Generational Wealth

Trusts are great for passing on wealth while keeping control. They offer tax benefits and protect against bad financial choices by your heirs.

There are three main trust types for legacy planning:

| Trust Type | Primary Purpose | Investment Implications | Best For |

|---|---|---|---|

| Revocable Living Trust | Probate avoidance, incapacity planning | Flexible allocation, can change over time | Most families regardless of wealth level |

| Irrevocable Life Insurance Trust (ILIT) | Estate tax liquidity, leverage | Premium funding strategy required | Estates approaching tax thresholds |

| Charitable Remainder Trust (CRT) | Income for life, remainder to charity | Income-focused with long-term horizon | Philanthropically-minded investors |

Each trust needs a special investment plan. For example, an ILIT needs steady income for premiums. A CRT focuses on income for life. Working with a financial advisor and estate attorney is key.

To avoid losing money to hidden fees, ask for clear fee details. These fees can add up over time.

A good first step is to make a simple worksheet. It should list:

- How much you want to leave to each person

- When you want to give it to them

- Special rules for certain people

- Who will take care of your kids

- Who will handle your estate after you’re gone

Starting a family wealth conversation is key. Talk with your family about your wishes and values. This is about more than just money.

Being open about your plans can prevent fights. Explain why you’re making certain choices. Write down these talks and update them as needed.

Legacy planning is not a one-time thing. It changes with tax laws, family needs, and your wealth. Make sure to review your plan with your advisor every year.

Begin your legacy planning by thinking about your values and how you want to share them. Then, take a step like talking to an attorney or discussing with your family. This will help you move closer to your goals.

Setting Philanthropic Investment Endowment Goals

Many investors find joy in giving to help others. After guiding clients for 12+ years, I’ve seen how giving can make a big difference. It’s not just about being generous; it’s a smart way to use your wealth.

Setting goals for giving is like planning for retirement. You need a clear plan for your charitable efforts. This plan should last long after you’re gone.

Before you start giving, make sure your own money is in order. Have enough saved for emergencies and pay off big debts. Giving should not stress you out.

Understanding Philanthropic Vehicles

There are many ways to give, each with its own benefits:

| Giving Vehicle | Minimum Entry | Tax Benefits | Control Level | Best For |

|---|---|---|---|---|

| Donor-Advised Fund (DAF) | $5,000-$25,000 | Immediate deduction, no capital gains | Medium | Beginning philanthropists |

| Private Foundation | $250,000+ | Deduction limits, excise tax | High | Family legacy planning |

| Charitable Trust | $100,000+ | Income stream, partial deduction | Medium-High | Income + giving goals |

| Direct Giving | Any amount | Standard deduction | Low | Immediate impact |

“The size of your philanthropic vehicle matters less than the consistency of your funding strategy,” I often tell clients. “A modest DAF funded regularly can outperform a large foundation that receives inconsistent contributions.”

Determining Your Sustainable Giving Capacity

Start by figuring out how much you can give each year. Giving 1-5% of your investments can make a big difference. This way, you help others without hurting your finances.

Use this formula to find out how much you can give:

Annual Sustainable Giving = (Total Investment Portfolio × Expected Return Rate) × (0.25 to 0.50)

This method helps you give from your investments’ growth, not your principal. For example, with a $500,000 portfolio earning 7% annually, you could give $8,750 to $17,500 each year.

Your advisor can help fit this into your overall financial plan. They’ll make sure your giving goals are realistic and don’t conflict with other important plans, like saving for retirement.

Maximizing Impact Through Strategic Asset Allocation

The right assets for giving can save you money and help more people. Here are some smart choices:

- Donate appreciated securities instead of cash to avoid capital gains taxes

- Utilize qualified charitable distributions (QCDs) from IRAs after age 70½

- Consider mutual fund shares with significant unrealized gains

- Explore impact investing alongside direct giving for aligned values

“I’ve seen clients double their giving impact simply by changing what they give,” I tell investors regularly. This smart way of choosing assets can greatly improve your giving.

When picking investments for your charitable funds, think about how long it will take to reach your goals. Giving like an endowment often means being more careful with your money. You might put 40-60% in bonds and the rest in stocks.

Integrating Philanthropy With Retirement and Legacy Planning

Good giving plans can help with other long-term goals. For example, trusts can give you income in retirement and then help causes you care about. Donor-advised funds can also involve your family in giving, strengthening your bond.

Here are ways to link giving with other plans:

- Name charitable organizations as partial beneficiaries of retirement accounts

- Establish a giving budget that scales with your retirement income

- Create a family mission statement that guides both investment and giving decisions

- Review philanthropic goals quarterly alongside your investment plan review

This way, your money and values stay together, now and in the future. It makes giving a key part of your wealth strategy.

“Related Topics: How to Set Realistic Investment Goals Successfully“

Practical Steps to Begin Your Philanthropic Journey

Start your giving plan with these steps:

First, pick 2-3 causes that really matter to you. Focus helps more than spreading your giving too thin. Use sites like Charity Navigator to check if organizations are well-run.

Next, decide how much to give first and how often. Even a little can grow a lot over time. Many donor-advised funds start with just $5,000.

Lastly, write down your giving goals clearly. Make them specific, measurable, achievable, relevant, and time-bound. This turns your good intentions into real change.

Remember, giving is a smart strategy for wealthy people. By setting goals now, you create a lasting legacy that shows your values and success for years to come.

“Read More: Long Term Investment Goals Examples for Beginners“

Allocating Assets Across Life Stages

Your investment plan changes as you grow older. How you spread your money across different types is key. It can make up to 90% of your long-term gains.

This choice needs to be updated often. It must fit your new goals and how much risk you can take.

Shifting from Growth to Preservation

In your early career (ages 25-40), focus on investments that grow. This helps secure your future. For goals more than 10 years away, pick growth ETFs for better returns.

When you’re at your peak earning years (40-55), mix growth with safety. Keep an emergency fund for sudden costs like medical bills.

Up to 77 % of a retiree’s final portfolio value is determined by returns earned in the first decade after retirement—a phenomenon known as “sequence of returns risk”—necessitating more conservative allocations as withdrawals begin.Ref.: “Pfau, W. (2013). Mitigating Sequence of Returns Risk. MIT Sloan Management.” [!]

As retirement nears (55-65), start moving to safer investments. The “100 minus age” rule is a guide for equity allocation. But, your own risk level might suggest different choices.

This change helps avoid big risks before you retire. It’s a key time for careful planning.

“You Might Also Like:

Rebalancing Portfolio After Major Events

Life events mean it’s time to check your investments. Changes like new jobs, inheritances, or buying a home are chances to adjust your strategy. Market ups and downs also call for rebalancing.

For goals under 3 years, choose easy-to-access funds like money market or CDs. Goals between 3-10 years do well with a mix of stocks and bonds. Keep track of your current investment mix to stay on track with your financial goals.

{kind=link}