Creating a solid joint home buying budget is the first step for couples buying a home together. It helps get better mortgage terms and keeps the relationship strong. Did you know 78% of American couples feel more stressed when buying a home?

I’ve helped many couples with their first home purchase. Money talks are key. “The couples who succeed aren’t the richest,” says mortgage expert Elaine Rodriguez. “They’re the ones who talk openly about money.”

Even if couples have money, knowing all the costs is important. This helps them deal with surprises and challenges together. Understanding the complete cost breakdown of buying a home is vital.

Most buyers only think about down payments. But there are hidden costs of buying a house that can hurt budgets and relationships. These costs can surprise even the most ready couples.

Quick hits:

- Combine finances wisely, not fully

- Save 3-5% more than the purchase price

- Have weekly money talks before looking

- Keep separate emergency funds for housing

- Write down all money agreements clearly

Align shared financial goals early

Starting to buy a home together needs a solid plan. In nine years, I’ve seen couples get stuck because they didn’t plan together. It’s not about being the same with money. It’s about having a common goal that respects both of you.

Before looking at houses, have a “financial vision” talk. Pick a quiet place like a café or park. This helps you talk openly about what’s important to you both.

Write down your dream home in five years. Think about where you want to live, how big it should be, and what it must have. When you share, you might find big differences. One couple realized they had different timelines for buying a home.

Then, talk about money. Decide how much you can spend each month. Figure out what you really need versus what you want. Knowing this helps you know how big a mortgage you can handle.

Write down what you agree on. Include your savings plan, when to start looking for houses, and when to move. This plan helps avoid fights when you start looking.

Discuss Lifestyle Plans Timeline Priorities Together

Buying a home is for now and the future. Think about your short-term needs and long-term dreams. Will you have kids or need space for aging parents?

Make lists of what you must have versus what you’d like. This helps you decide where to spend your money. One couple decided they wanted a shorter commute more than extra space.

Mortgage calculators are a good start, but they don’t cover all your costs. If you love to travel, you might need a smaller mortgage. But if you rarely eat out, you can spend more on a house.

These talks take about 90 minutes but save a lot of fights later. They also make your relationship stronger by showing you respect each other’s goals.

Lenders look at your joint finances when deciding on rates and approval. So, having clear goals early makes you stronger applicants. This helps you make a decision faster when you find the right house.

“You Might Also Like: How to determine home buying budget for beginners“

Calculate combined debt income affordability ratios

Smart couples know the importance of debt-to-income calculations when house hunting. They avoid budget disasters by doing this. Lenders check your finances closely before approving a loan.

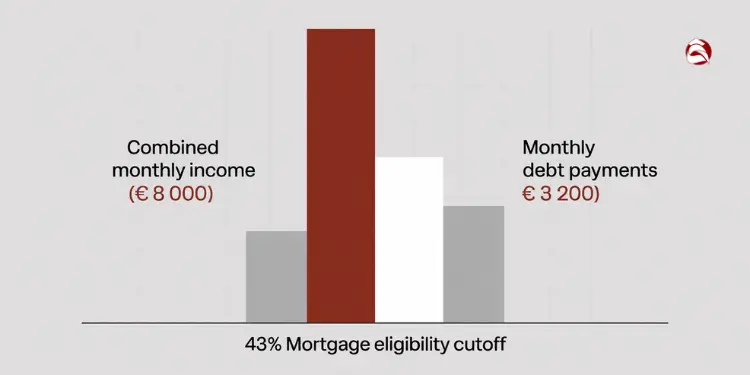

When figuring out how much house you can afford, lenders look at your debt-to-income ratio (DTI). This ratio is very important. Most loans want your total debt to be less than 43% of your income.

To find out how much you can buy, start by adding your incomes. Include salaries, bonuses, alimony, and investment income. Self-employed couples should use the average of their last two years’ income after expenses.

Then, find out your current DTI. This shows how much of your income goes to debt each month. The house price to income ratio also helps see if a home is affordable.

“Explore More: Signs you are not ready to buy house yet“

Include Student Loans Car Payments Accurately

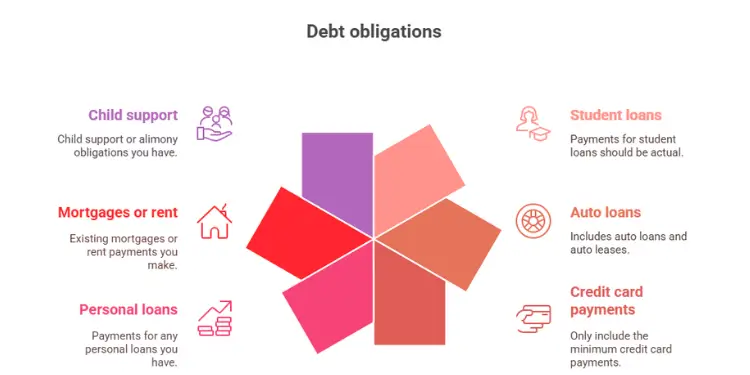

When figuring out your DTI, be very accurate. Couples often underestimate their debt by $300-400 a month. This can cut your home budget by $50,000 or more. List every monthly debt, including:

- Student loan payments (use actual payment amounts, not estimates)

- Auto loans and leases

- Minimum credit card payments (not what you typically pay)

- Personal loans

- Existing mortgages or rent

- Child support or alimony obligations

Don’t guess these amounts – use your actual statements. For variable payments like credit cards, use the minimum payment on your latest statement. For student loans in deferment, lenders usually calculate 0.5-1% of the balance as your monthly payment.

Now, do the math: add all your monthly debt payments and divide by your combined income. Then, multiply by 100 to get your DTI percentage. For example, if you have $3,000 in monthly debt payments and $10,000 in monthly income, your DTI is 30%.

“The 43% DTI rule isn’t just a suggestion – it’s the maximum allowed for most qualified mortgages under federal regulations. Some loan programs may stretch to 50%, but they typically come with higher interest rates and additional requirements.”

IMPLEMENTATION CONSTRAINT:

Under federal Qualified Mortgage rules, lenders cannot approve most loans if the borrower’s total debt-to-income ratio exceeds 43 %; surpassing this cut-off typically forces borrowers into higher-cost non-QM products or denial. Ref.: “Consumer Financial Protection Bureau. (2020). Qualified Mortgage Definition under the Truth in Lending Act (Regulation Z): General QM Loan Definition. CFPB.” [!]

To find out how much mortgage you can afford, subtract your current DTI from the lender’s maximum (usually 43%). This shows how much of your income is left for a mortgage. For example, if your current DTI is 30%, you have 13% left for a mortgage payment.

Remember, your mortgage payment must cover principal, interest, taxes, and insurance (PITI). Many first-time buyers forget to include property taxes and homeowners insurance. These can add hundreds to your monthly payment.

Use an affordability calculator to find a specific price range. Most online calculators let you input your income, debts, down payment, and interest rate. I recommend trying different interest rates to see how they affect your budget.

The biggest mistake couples make is ignoring future expenses. If you’re planning big changes in 2-3 years (like having kids or changing careers), include these in your calculations. A mortgage that’s okay now might be too much later.

“Read More: How to organize finances before buying house successfully“

Choose equitable down payment contributions

Buying a home together can be tough, but figuring out the down payment is the hardest part. In nine years, I’ve seen it cause more stress than anything else. It gets even harder when one person has a lot more money.

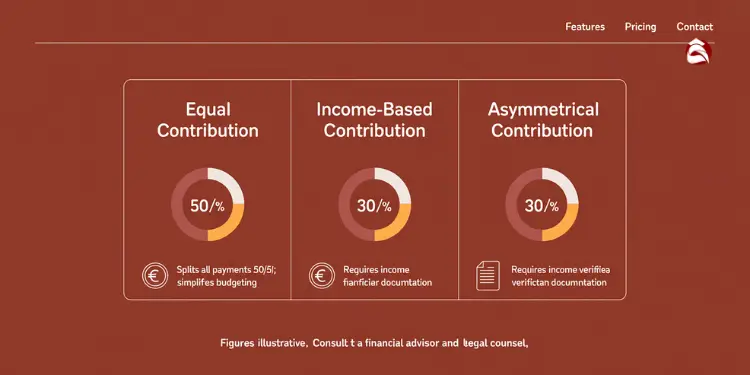

Finding a way to split the down payment that works for both of you is key. Many think a 50-50 split is the only fair way, but there are other options. What’s fair for you will depend on your situation.

I’ve helped couples find three ways to split the down payment that work well. Each method has its own benefits, depending on your money and relationship. Let’s look at these options to see which might be best for you.

| Contribution Approach | How It Works | Best For | Financial Considerations | Legal Implications |

|---|---|---|---|---|

| Equal Dollar Contributions | Both partners contribute the exact same amount regardless of income differences | Couples with similar financial situations or those who prefer straightforward accounting | May strain the lower-earning partner; might require a smaller total down payment | Simplifies ownership documentation (50-50 split) |

| Proportional to Income | Each partner contributes based on their percentage of total household income | Couples with significant income disparities who want to maintain proportional fairness | Often allows for larger total down payment; reduces financial strain on lower earner | Requires clear documentation of ownership percentages |

| Asymmetrical Contributions | One partner contributes substantially more than the other | Situations where one partner has significantly more savings or received a gift/inheritance | Maximizes down payment; may reduce monthly mortgage payments | Absolutely requires legal documentation of ownership stakes |

The equal contribution method is good for couples with similar money. Each person puts in the same amount, making a 50-50 split. But, it can be hard for the partner with less money.

Proportional contributions are based on income. If one partner earns 60% of the income, they pay 60% of the down payment. This way, income differences are considered, making it fair for couples with big income gaps.

Asymmetrical contributions mean one partner gives a lot more money. This can make your down payment bigger and lower your monthly payments. But, you must document it well to protect both sides.

Protect Each Partner Legally Via Agreements

It’s important to write down your agreement, no matter the method. I’ve seen disputes that could have been avoided with the right paperwork. This is very important for unmarried couples who don’t have the same legal rights as married couples.

For unmarried couples, I always suggest a legal agreement. It should cover:

- Each partner’s ownership percentage based on contributions

- How mortgage payments will be split

- Process for handling property sale if the relationship ends

- Buyout procedures if one partner wishes to keep the home

- How appreciation or depreciation will be handled

Even married couples should talk about big money differences. Decide if the bigger contributor wants to be repaid or if it’s a gift. This avoids future problems.

One client put in 80% of the down payment from an inheritance. We made an agreement that she would get that percentage of the sale price. This protected her money and gave her partner fair equity for his contributions.

Don’t wait until closing to talk about money. Start discussing early, write down your agreement, and have a lawyer check it. This small step can save a lot of trouble in your shared home journey.

Remember, different loans have different down payment rules. Your lender can explain how this affects your payments and interest rate.

The most successful homebuying couples I’ve worked with are those who prioritize transparency and fairness over rigid equality. They recognize that equitable contributions might not mean identical dollar amounts.

Choosing a fair way to split the down payment and documenting it well can avoid a lot of stress. This lets you focus on enjoying your new home together.

“Learn More About: Why budget before buying your first home matters“

Set joint emergency fund for surprises

When you buy a home together, it’s key to have an emergency fund. Homeownership brings new surprises that renters don’t face. I’ve seen many couples face unexpected repair costs that hurt their finances and relationship.

Make a special emergency fund for your home. It should cover three months of housing costs and $5,000 for repairs. Some clients have faced $4,200 HVAC costs soon after buying their home.

Fannie Mae advises homeowners to keep 3 – 6 months of household expenses in cash reserves to cushion job loss, medical bills, or major repairs. Ref.: “Fannie Mae. (2022). SMART HOMEBUYING: Tips on Building Your Cash Reserves. Fannie Mae.” [!]

Start saving for this fund before you look for a house. Keep adding to it each month after you buy. Use an emergency fund calculator that’s set for homeowners.

Keep your emergency fund in a high-yield savings account. Both partners should have access but need two signatures to take out money. This stops impulsive spending and ensures both partners agree on emergency decisions. Mortgage payments are a big part of your income—don’t let repairs add stress.

“The difference between homeowners who thrive and those who struggle often comes down to preparation. A robust emergency fund isn’t just financial protection—it’s relationship insurance.”

Make a clear plan for what’s a home emergency versus a cosmetic update. This helps avoid fights when something breaks. True emergencies include:

- Water heater failures

- Roof leaks or damage

- HVAC system breakdowns

- Plumbing emergencies

- Electrical system failures

Don’t confuse cosmetic updates with emergencies. Your loan and interest rate didn’t account for these surprises.

| Emergency Category | Typical Cost Range | Response Timeline | Financial Impact |

|---|---|---|---|

| Major Roof Repair | $800-$3,000 | Immediate | High (prevents water damage) |

| HVAC Replacement | $3,500-$7,000 | 1-3 days | High (affects livability) |

| Plumbing Emergency | $500-$2,000 | Same day | High (prevents water damage) |

| Electrical Failure | $400-$1,800 | Same day | High (safety concern) |

Check and refill your emergency fund every quarter. Remember, annual taxes and insurance are predictable, but surprises aren’t. Couples with good emergency funds feel less stressed and have stronger relationships during crises.

Keep your mortgage payments under 28% of your income. This lets you save for emergencies without debt. Being ready for repairs is as important as making your mortgage payments.

The widely-used 28/36 affordability rule caps housing costs at 28 % of gross monthly income and total debt at 36 %, aligning with most underwriting models. Ref.: “Kagan, J. (2024). 28/36 Rule: What It Is, How to Use It, Example. Investopedia.” [!]

Include your emergency fund plan in your home buying budget checklist. This step can make homeownership a source of pride, not stress. Private mortgage insurance and other costs are just the start—surprises test your financial strength.

“Further Reading:

Plan decision making process for disputes

Even couples with perfect credit scores can disagree on their housing budget. I’ve seen partners clash over paying off the mortgage faster or making a larger down payment to avoid PMI costs.

Make a plan for solving disputes before you start looking for homes. First, figure out how each partner likes to handle money. Decide on spending limits (usually $200-500) that need both of you to agree before buying something non-essential.

Include a 48-72 hour wait for big decisions about how much to spend on a house. This helps avoid making choices based on emotions. Remember, your total monthly debt affects how much house you can buy. Every $100 in monthly payments means you can buy $20 less house.

Have a 30-minute budget check-in every month. Talk about property taxes, insurance, savings, and upcoming bills. Each person should share one financial worry and one success to discuss. This keeps the focus on finding solutions.

If you keep arguing about the mortgage or the type of property, think about getting help from a financial advisor. Many couples I’ve worked with find that taking turns making the final decision helps keep things balanced and respectful.

Download my “Financial Dispute Resolution Worksheet” below. It has helped many of my clients figure out how much house they can afford while keeping their relationship strong.

{kind=link}