Your investment goals shape your portfolio more than any market guess. Clear financial goals are the base for building wealth. Think about how your plan changes when saving for retirement versus a home in three years.

A big 65% of Americans with clear financial goals do better than those without. I’ve seen many new investors stay strong during tough times. Those without goals often sell at the worst times.

“Investing is about spending now for a future goal,” says advisor McGregor. This view changes how you pick assets and how much risk you take.

In twelve years with Phoenix clients, I’ve seen beginners with clear goals build stronger portfolios. Their life situations, not market guesses, guide their asset mix.

Quick hits:

- Time horizons dictate risk tolerance

- Goals create accountability during volatility

- Specific targets yield measurable progress

- Personal circumstances outweigh market predictions

Defining Personal Financial Goals And Timeframes

Before picking an investment, know what your money needs to do and by when. Many investors skip this step and end up losing money. Your financial goals are the key to every investment choice.

“Step 1. Ask yourself: What am I trying to achieve? Your financial goals are the ‘why’ of investing,” McGregor says. This question is the first step in building a good portfolio.

Start by listing your goals. These could be saving for retirement, buying a home, or paying for education. Then, think about three important things:

- Your time horizon: When will you need the money for each goal?

- Your risk tolerance: How much market change can you handle?

- Your liquidity needs: Do you need to use this money soon?

These answers will help you decide what to invest in and how to organize your financial portfolio. Different timeframes need different strategies.

Setting Short Term Liquidity Safety Targets

For goals in 0-3 years, focus on keeping your money safe. These are your “sleep-at-night” funds—money you can’t afford to lose.

Short-term goals include:

- Emergency reserves (3-6 months of expenses)

- Major purchases in 36 months

- Taxes you need to pay soon

- Education costs in the near future

For these goals, choose safe and easy-to-access options. High-yield savings and Treasury bills are good choices, with returns of 4-5% (as of December 2024).

The 3-month U.S. Treasury bill averaged 4.27 % in December 2024, confirming the current yield range cited for ultra-safe cash reserves.Ref.: “Board of Governors of the Federal Reserve System (2025). 3-Month Treasury Bill Secondary Market Rate (Series TB3MS). FRED.” [!]

Be specific about your needs. Don’t just say “emergency fund.” Calculate how much you need monthly and for how many months. This helps avoid not saving enough for important needs.

| Short-Term Goal | Target Amount | Timeframe | Suitable Vehicles |

|---|---|---|---|

| Emergency Fund | $10,000-30,000 | Immediate access | High-yield savings, money market |

| Home Down Payment | $20,000-100,000 | 1-3 years | CDs, Treasury bills, short-term bonds |

| Major Purchase | $5,000-50,000 | 6-24 months | Short-term bond funds, T-bills |

| Tax Payments | Varies by situation | 3-12 months | High-yield savings, money market |

Planning Long Horizon Wealth Accumulation Objectives

For goals 10+ years away, your investment strategy changes. With a long-term view, you can handle market ups and downs for bigger returns.

Long-term goals include:

- Retirement funding (often 20+ years away)

- College education for young children

- Legacy planning or wealth transfer

- Major lifestyle upgrades planned for distant future

The main difference is how you view market changes. For long-term goals, market drops are chances, not threats. This changes which assets are right for you.

Investors who separate short and long-term goals make better choices during market ups and downs. Knowing your short-term needs are safe lets you see market downturns as buying chances for long-term goals.

“The single greatest edge an investor can have is a long-term orientation.”

To plan for long-term goals, start with your target amount and date. For example, if you need $1 million for retirement in 30 years, use investment calculators to figure out monthly contributions.

Remember, your financial situation changes over time. What’s a long-term goal today might be a short-term one later. Your investment strategy should change as these timeframes get shorter, focusing on keeping your money safe as the goal date gets closer.

By defining your short-term needs and long-term goals, you create a plan for every investment choice. This clarity keeps your financial plan in line with your life goals, not just chasing returns.

Matching Risk Tolerance With Asset Allocation Choices

Risk tolerance and asset allocation are key to a good investment plan. As a portfolio manager for over 12 years, I’ve seen many investors leave good plans behind. They did this because they didn’t know how much risk they could handle.

Understanding your risk tolerance is not just about feeling scared. It’s about picking investments you can stick with, no matter what the market does.

Studies show that how you mix your investments can explain about 90% of your returns over time. Your mix will depend on how much risk you can handle and how long you can wait to see returns.

Long-term research on 82 large pension plans found that asset-allocation policy explains 91.5 % of quarterly return variability, dwarfing timing and security selection effects.Ref.: “Brinson, G. P., Singer, B. D., & Beebower, G. L. (1991). Determinants of Portfolio Performance II: An Update. Financial Analysts Journal.” [!]

If you have a long time to invest, you might choose more stocks. Stocks can be riskier in the short term but often do better over time.

If you’re worried about market ups and downs, bonds might be a better choice. The goal is to find a mix that fits your investment goals and how you feel about risk.

Using Risk Profiling Questionnaires Effectively

Most places give you risk questionnaires to start. These tools are good but don’t tell the whole story. They don’t show how you’ll really feel in tough times.

Academic testing reveals that few recognised, valid, and reliable risk-tolerance instruments exist, meaning standard questionnaires can mis-diagnose investors’ true comfort with volatility.Ref.: “Grable, J. & Lytton, R. (1999). Financial Risk Tolerance Revisited: The Development of a Risk Assessment Instrument. Financial Services Review.” [!]

Good risk assessment looks at both facts and feelings. Facts include your time horizon, job stability, and savings. Feelings include how you react to market changes and past investment experiences.

To get a better picture, try these scenario tests:

- How would you react if your portfolio dropped 20% in three months?

- Would you keep adding money during a long market downturn?

- Have you sold investments too soon because of market drops?

These questions can show more about your risk tolerance than any formal test. Many people think they can handle more risk until they face it.

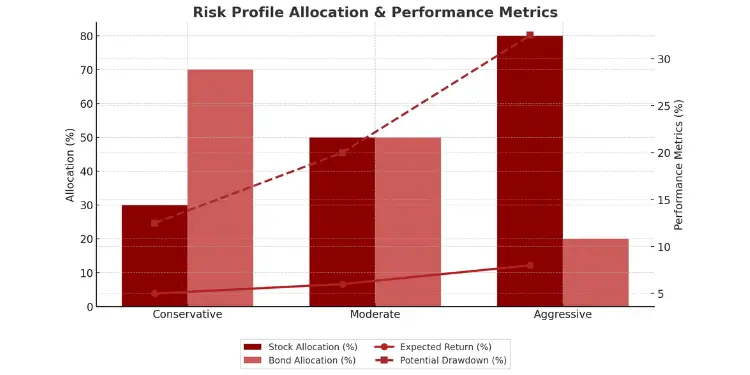

| Risk Profile | Stock/Bond Allocation | Expected Annual Return | Potential Drawdown | Suitable For |

|---|---|---|---|---|

| Conservative | 30/70 | 4-6% | 10-15% | Near-term goals, low risk tolerance |

| Moderate | 50/50 | 5-7% | 15-25% | Mid-term goals, average risk tolerance |

| Aggressive | 80/20 | 7-9% | 25-40% | Long-term goals, high risk tolerance |

After figuring out your risk profile, picking the right mix of investments is easier. The table above gives general ideas for different types of investors. But, your situation might need special adjustments.

Your ideal mix of investments can change over time. A young person might choose more stocks, while someone close to retirement might focus on keeping their money safe.

Knowing a lot about investing helps you make better choices. People who understand the market better can often handle more risk if they can afford it.

The biggest risk of all is not taking one. The key is taking calculated risks that align with both your financial capacity and emotional tolerance for uncertainty.

After you’ve matched your risk tolerance with the right investments, you need to check if they match your financial goals. If your safe portfolio can’t grow enough to reach your goals, you have three options. You can wait longer, save more, or learn to take more risk.

By carefully choosing investments that match your risk tolerance, you build a plan you can stick with. This is the secret to success in investing for the long term.

“Explore More: How to Make 50/30/20 Budget with Clear Practical Step by Step“

Selecting Asset Classes For Growth

Choosing the right mix of asset classes is key to a good portfolio. You need to know your risk level and how to diversify. I’ve helped investors for 12 years and found that simple often works best for beginners.

Let’s look at four main asset classes. They are the base of most good portfolios. Each has its own special traits that help meet your investment goals:

Core Asset Classes and Their Growth Characteristics

U.S. equities let you own pieces of American companies. They often grow a lot over time. For young investors, putting a lot in equities makes sense, even if it’s bumpy.

International stocks also grow and spread out risk. They can do well when the U.S. market doesn’t. I suggest 20-40% of your equity go to international markets, based on how you feel about currency changes.

Bonds are stable and give income. They help when the stock market drops. Bonds are like loans to governments or companies, and they pay you back with interest. Bonds get more of your money as you get older or near financial goals.

Cash and cash-like things keep your money safe and liquid. They don’t keep up with inflation but help you avoid selling other investments in bad times. Keep 3-6 months of expenses in cash.

Choosing Between Investment Vehicles

After picking your asset classes, choose how to invest in them. Each option has its own good points:

| Investment Vehicle | Advantages | Disadvantages | Best For |

|---|---|---|---|

| Individual Stocks/Bonds | Full control, no fees | Needs a lot of research, riskier | For experienced investors, big portfolios |

| Index Funds | Low cost, spreads out risk | Only gets market returns, no protection | For main portfolio, passive investors |

| ETFs | Can trade all day, tax smart | Trading costs, some complexity | For tax-aware accounts, tactical moves |

| Actively Managed Funds | Professional help, special strategies | High fees, not always better | Niche markets, special areas |

For new investors, I suggest starting with index funds or ETFs. They offer quick diversification at low cost. Less cost means more money in your pocket over time.

When comparing funds, look at their expense ratios. Even small differences add up. A 0.05% fee versus 0.75% can mean tens of thousands more in your account over years.

“For More Information: 50/30/20 vs 80/20 Rule Detailed Comparison Guide“

Matching Asset Types to Economic Conditions

Different assets react differently to the economy. Knowing this helps you prepare for different times:

In good times, stocks usually do well. Tech, consumer, and industrial sectors often lead. Your portfolio might do better with more of these when the economy is strong.

In times of inflation, real assets like commodities, real estate, and TIPS protect your money. They tend to move with inflation, keeping your buying power.

In bad times, defensive sectors like utilities, staples, and healthcare often do better. Bonds also gain value when interest rates fall. Keeping some bonds in your portfolio helps it stay strong.

For young investors, market drops are chances to buy, not risks. Buying at lower prices means more money over time. I tell clients to keep investing during downturns.

Asset allocation changes over time. As your life changes or markets shift, so should your mix. Make smart changes based on your goals, not just market feelings.

Your next step is to diversify within each class. Spread your investments across sectors and industries. This reduces risk and keeps growth chances.

Diversifying Across Sectors To Manage Volatility

Asset allocation is key, but sector diversification is even more important. Many investors focus too much on stocks and bonds. They forget about sector allocation, which can cause big problems when the economy changes.

Spreading investments across different sectors is smart. Think of sectors like neighborhoods in the economy. Just like neighborhoods, sectors react differently to changes.

Portfolios that spread investments well do better in tough times. They don’t avoid all ups and downs. They just make the journey smoother.

“You Might Also Like: How to Prioritize Multiple Investment Goals as a Beginner“

Balancing Cyclical Defensive Sector Weightings

The economy goes up and down, affecting sectors differently. Cyclical sectors like tech and consumer goods do well when the economy grows. But they can fall hard when it shrinks.

Defensive sectors like utilities and healthcare stay steady. People always need these things, even when times are tough.

Finding the right mix of sectors is key. Most investors should have some of both. Adjust this mix based on how long you can wait and how much risk you can take.

Those with more time can take on more cyclical sectors. But those close to retirement should lean on defensive sectors. This helps protect against sudden market drops.

It’s a big mistake to put too much in one sector. This can hurt a lot when that sector falls. In 2000, tech-heavy portfolios lost a lot when the dot-com bubble burst. In 2008, too much in finance was a disaster.

MSCI’s risk analytics show that even a single 5 % “hot” position can contribute disproportionately to total portfolio risk, exposing investors to sharp drawdowns when that sector reverses.Ref.: “MSCI (2012). RiskMetrics – Risk Reporting for Individual Investor Portfolios. MSCI Inc.” [!]

| Sector Type | Economic Sensitivity | Examples | During Expansion | During Contraction |

|---|---|---|---|---|

| Cyclical | High | Technology, Consumer Discretionary, Industrials | Strong outperformance | Significant underperformance |

| Defensive | Low | Utilities, Consumer Staples, Healthcare | Modest growth | Relative stability |

| Hybrid | Moderate | Energy, Materials, Communication Services | Variable performance | Mixed results |

| Rate-Sensitive | Variable | Financials, Real Estate | Performs well with rising rates | Sensitive to credit conditions |

Incorporating Low Correlation Alternative Investments

Adding alternative investments can help protect your portfolio. These investments often move differently than stocks and bonds. They can zig when others zag.

Real Estate Investment Trusts (REITs) offer a way to invest in real estate without owning it. They often perform differently than the stock market, which is good during inflation.

Commodities like gold can be a safe haven during economic uncertainty. They can also be affected by supply and demand, not just stock market trends.

Treasury Inflation-Protected Securities (TIPS) protect against inflation. They adjust to keep up with inflation, helping to preserve your buying power when stocks and bonds struggle.

The goal with alternatives isn’t to make more money. It’s to reduce how much your portfolio swings. Even a small 5-15% in alternatives can make a big difference.

When checking your diversification, use this checklist:

- Do you have exposure to both cyclical and defensive sectors?

- Is any single sector representing more than 25% of your equity allocation?

- Do your holdings include some assets with low correlation to traditional stocks and bonds?

- Would your portfolio withstand a severe downturn in your largest sector?

- Are you prepared for different economic environments (growth, recession, inflation, deflation)?

Good diversification isn’t about having everything. It’s about having assets that react differently to the economy. This makes your portfolio stronger and helps you stay in the game through market ups and downs.

“Related Articles: Examples of Common Investment Goals for Beginners“

Rebalancing Strategy When Goals Or Markets Shift

Portfolio rebalancing is key to keeping your investments on track. It’s like a routine check-up for your money. Without it, your investments can stray from your goals.

Think of rebalancing as adjusting your financial GPS. Markets can change your portfolio’s mix. For example, if stocks do well, your portfolio might get too risky.

Life changes also mean you might need to adjust your investments. Getting married, having kids, or starting a new job can change your financial needs. You might need to look at your goal-based investing strategy again.

“Read More: How Investment Goals Influence Portfolio Strategy for Beginners“

Calendar Versus Threshold Rebalancing Comparison

There are two main ways to rebalance your portfolio: calendar-based or threshold-based. Each has its own benefits.

| Feature | Calendar-Based Rebalancing | Threshold-Based Rebalancing |

|---|---|---|

| Timing Trigger | Predetermined intervals (quarterly, semi-annually, annually) | When allocations drift beyond set percentage thresholds |

| Monitoring Required | Low (scheduled reviews) | Higher (regular portfolio checking) |

| Transaction Frequency | Predictable, scheduled | Variable, market-dependent |

| Best Suited For | Disciplined investors who prefer routine | Active investors comfortable with market monitoring |

Calendar-based rebalancing is simple and regular. It’s good for those who like routine. I suggest it for new investors to keep costs down.

Vanguard’s 2022 study found that annual rebalancing strikes the best balance between cost and risk-control, outperforming both very frequent and very infrequent schedules on a risk-adjusted basis.Ref.: “Zhang, Y. et al. (2022). Rational Rebalancing: An Analytical Approach to Multi-Asset Portfolio Rebalancing Decisions and Insights. Vanguard Research.” [!]

Threshold-based rebalancing reacts to market changes. It’s good for active investors. But, it needs more watching.

For those building an emergency fund, a mix of both might work. This way, you get regular checks and quick action when needed.

Here are some tips for rebalancing:

- Use new money to fix imbalances without selling

- Adjust tax-advantaged accounts first to save on taxes

- Harvest tax losses in taxable accounts

- Look at your whole portfolio, not just parts

- Keep track of your rebalancing steps

Don’t give up on a strategy just because one part isn’t doing well. Markets go up and down. But, if things keep going wrong, it might be time to look closer.

Changes in the market might mean you need to rethink your strategy. For example, low interest rates might mean you need to adjust your bond plan.

Remember, you can’t predict the future. That’s why keeping your portfolio balanced is so important. It helps you buy low and sell high, which is smart.

At least once a year, review your goals, cash needs, time horizon, risk tolerance and portfolio performance.

Life changes mean you should check your whole investment plan. Big events like job changes or having kids are good reasons to review.

- Job changes or career transitions

- Family additions or changes

- Approaching retirement (5-10 years before)

- Inheritance or windfall receipt

- Significant health changes

When big things happen, don’t just rebalance. Look at your whole investment plan. You might need to change your goals or how you’re investing.

By rebalancing regularly, you keep your investments right for your goals. This helps you avoid making emotional decisions based on market ups and downs.

“Related Topics:

Monitoring Progress And Adjusting Portfolio Regularly

Setting up a regular check-in system is key. I suggest reviewing your portfolio every three months. This keeps you on track with your goals, not just market trends.

Make a simple chart to track your portfolio’s value and goal progress. Include targets, timelines, current values, and how much you’re adding each month. This way, you stay true to your plan, not just chasing numbers.

Don’t make quick decisions when markets change a lot. Many people lose money by selling too soon. Instead, see these times as chances to buy more.

Rebalance your portfolio if it’s off by 5% or more from your goals. Rebalancing means checking your current mix, seeing what you should aim for, and adjusting by selling or buying.

Life events like getting married or nearing retirement might mean you need to adjust your portfolio. If you’re looking for better returns or need help with investment choices, a financial advisor can help. They can guide you through market ups and downs and make sure your income matches your risk level.

Staying calm and focused is key to success. Your main goal should be moving closer to your specific targets, not just following market trends.

{kind=link}