Did you know most Americans think they need at least $10,000 to start building wealth? But the truth is, you can start with just $100 and a clear plan.

After 12 years helping first-time investors in Phoenix, I’ve learned something key. Success doesn’t depend on how much money you have. It’s about knowing what you’re aiming for. Warren Buffett said, “Someone’s sitting in the shade today because someone planted a tree long ago.”

Your financial goals are like a compass in the complex world of money. They help you choose the right accounts, decide on risk levels, and pick strategies that fit your timeline. Many new investors dive into stocks without first asking, “What am I saving for?”

This reminds me of how people learn about blockchain technology. 76% have heard of it, but only 16% have tried it because they lack clear goals. Setting specific targets makes abstract ideas into steps you can take.

Whether you’re saving for emergencies, planning to buy a home, or starting to save for retirement, clear goals make progress real. The clearer your goal, the easier your path becomes.

Key Takeaways:

- Start with defining your “why” before worrying about investment mechanics

- Your financial objectives determine which accounts and strategies make sense

- Clear targets transform abstract financial concepts into achievable milestones

- Begin with any amount—strategy matters more than starting sum

Clarify Personal Reasons Behind Investing

In my twelve years guiding investors, I’ve learned that knowing your “why” is key. Don’t start by asking, “What should I invest in?” Instead, ask yourself, “What am I investing for?” This simple shift changes how you set financial goals.

Your investment strategy should reflect your personal story, not just generic advice. When market volatility hits, those who connect their money to meaningful goals stay strong. Others might panic and sell at the worst time.

I’ve seen clients get through three market corrections because they saw their investments as funding for big life goals. This emotional tie to your goals makes you more resilient than just numbers can.

Visualize Future Lifestyle Funding Needs

Take time to imagine what your investments will fund. Close your eyes and see yourself in that retirement home in Arizona. Feel the joy of paying off that final college tuition. This makes your investment more than just numbers.

Make your goals specific. Instead of vague ideas like “save for retirement,” define it clearly. For example, “Generate $4,000 monthly income by age 65” or “Fund a $25,000 wedding for my daughter in five years.” These clear targets give your investment decisions a clear purpose.

The more vividly you can picture what you’re investing for, the easier it becomes to make consistent contributions even when markets get rocky.

I suggest making a vision board or detailed document for these future needs. Look at it when you’re tempted to give up during market ups and downs.

Separate Essential and Aspirational Objectives

Not all financial goals are equal. Creating a hierarchy helps you allocate resources wisely. I divide goals into essential and aspirational.

Essential objectives are your financial foundation—needs that must be met first:

- Emergency reserve (3-6 months of expenses)

- Retirement security

- Basic healthcare funding

- Essential debt elimination

Aspirational objectives are the enrichment layer of your financial life:

- Vacation properties

- Legacy planning for heirs

- Philanthropic goals

- Luxury purchases or experiences

This separation helps when setting a goal timeline. I’ve seen many chase aspirational goals while ignoring their essential foundation, leading to painful corrections later.

Remember, your investment goals should reflect your values, not what others think. Write down both categories of goals to make them real. Review them quarterly as your life changes.

By understanding why you’re investing before choosing what to invest in, you create a personal finance plan that can withstand market cycles. It keeps you focused on achieving your goals, no matter the economy.

Define Short and Long Term Targets

The timeline of your financial goals is key to choosing the right investments. I’ve helped many clients set their goals based on time frames. This step is crucial for picking the right investment products.

Investment goals fall into three main time frames. Each needs a different strategy to balance growth and stability. Knowing these time frames helps match the right financial tools to your goals.

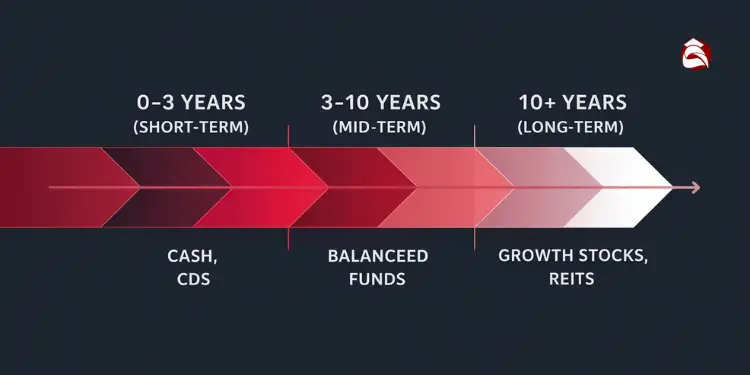

Short-Term Goals (0-3 Years)

Short-term goals focus on safety and quick access to money. If you need your money in the next three years, keeping it safe is most important. This includes saving for emergencies, vacations, or a down payment on a home.

For these goals, consider these low-risk options:

- High-yield savings accounts

- Money market funds

- Short-duration Treasury bills

- Certificates of deposit (CDs)

I advise keeping short-term funds away from the stock market. A 20% market drop could harm your plans if you need the money soon. Instead, aim to beat inflation while keeping your capital safe.

Mid-Term Goals (3-10 Years)

Mid-term goals allow for a bit more risk while still keeping things stable. These might include saving for college, starting a business, or buying a vacation home in the next decade.

For these goals, a balanced approach works best:

- Balanced mutual funds

- Bond funds with 40-60% allocation

- Blue-chip dividend stocks

- Target-date funds aligned with your timeframe

With 3-10 years to recover, you can take on some risk. A mix of growth and fixed-income investments can balance out market ups and downs.

“read more: How a Financial Advisor Can Help with Investment Goals“

Long-Term Goals (10+ Years)

Long-term goals are best suited for growth strategies. This includes retirement planning, building generational wealth, or saving for a child’s education. With decades to go, you can handle market swings.

For long-term financial goals, consider:

- Broad market index funds

- Growth-oriented ETFs

- Real estate investment trusts (REITs)

- Tax-advantaged retirement accounts

History shows that stocks usually outperform other investments over long periods. A retirement plan with 20+ years can safely invest 70-90% in stocks, based on your risk tolerance.

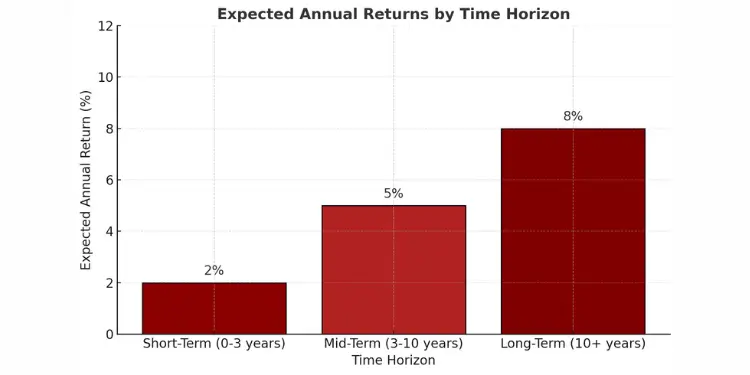

| Time Horizon | Appropriate Investments | Risk Level | Example Goals | Expected Annual Return |

|---|---|---|---|---|

| Short-Term (0-3 years) | High-yield savings, Money markets, CDs, T-bills | Very Low | Emergency fund, Home down payment, Wedding | 1-3% |

| Mid-Term (3-10 years) | Balanced funds, Corporate bonds, Blue-chip stocks | Moderate | College fund, Home upgrade, Business startup | 4-6% |

| Long-Term (10+ years) | Index funds, Growth stocks, REITs | Higher | Retirement, Legacy planning, Early financial independence | 7-10% |

The key is to remember: the longer your time frame, the more market ups and downs you can handle. This is the core of strategic asset allocation.

Before picking investments, map your goals to these time frames. This step alone can help avoid common mistakes and boost your confidence in reaching your financial goals.

Your investment plan should change as your goals evolve. A retirement account might start with growth but shift to preservation as you near your target date.

Align Risk Comfort With Goal Timeline

Your ability to handle market ups and downs must match your investment time frame. This ensures your portfolio stays strong even when markets drop. Many people think they can handle risk, but seeing their accounts fall 20% makes them doubt.

True risk comfort is about knowing how much risk you can handle. It’s about your emotional and financial readiness for market changes. If you need money soon, like for a home, you can’t take as much risk.

Investment strategies should consider how long you have until you need the money. Also, think about how you’ll feel if your balance goes down. For example, if you need money in three years, you can’t take as much risk as someone saving for retirement.

Risk tolerance changes as you get older. A 35-year-old saving for retirement can take more risk than someone five years from retirement. Life events like getting married or having kids can also change your risk tolerance.

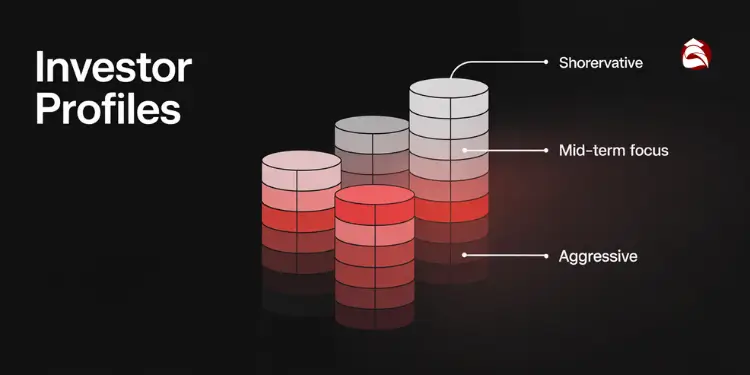

Match Asset Classes to Risk Appetite

Different investments have different risks and rewards. The key is to match these to your risk comfort and timeline. A good portfolio should let you sleep well while still working towards your goals.

For those with short time frames (1-3 years), focus on keeping your money safe. Consider CDs, Treasury bills, and short-term bond funds. They offer stability and modest returns, making them good for short-term goals.

Those with 5-10 year horizons can take a balanced approach. Aim for 60% fixed income and 40% equities. This mix offers growth potential while keeping volatility in check.

| Risk Profile | Time Horizon | Suggested Allocation | Expected Volatility |

|---|---|---|---|

| Conservative | 1-3 years | 80-90% fixed income, 10-20% stocks | Low |

| Moderate | 5-10 years | 40-60% stocks, 40-60% fixed income | Medium |

| Aggressive | 15+ years | 80-90% stocks, 10-20% fixed income | High |

Aggressive investors with long time frames can focus on 80-90% equities. This includes stocks from different countries. This approach accepts more risk for potentially higher returns over time.

Diversification is key. Spread your investments across asset classes and within each class. For stocks, diversify by industry, size, and location. No single investment should be more than 5-10% of your portfolio.

The biggest risk of all is not taking one when you have time on your side.

Check your risk alignment every year or after big life changes. As your timeline or financial situation changes, so will your best asset allocation. The goal is to take the right amount of risk for your situation and goals.

“read also: Why People Fail to Reach Investment Goals“

Use SMART Framework for Goal Metrics

In my twelve years guiding investors, I’ve seen the SMART method make a big difference. It turns vague dreams into real goals. Without clear goals, investing is like flying without a map.

The SMART framework is key to a successful investment plan. It has five parts that help you reach your financial goals:

- Specific: Set exact amounts, like “save $1.2 million for retirement by 65.”

- Measurable: Use numbers to track your progress. “Save $750 a month” is a clear goal.

- Achievable: Make sure your goals are realistic. Saving 15% is doable, but 50% might be too high.

- Relevant: Align your goals with what matters to you. Saving for your child’s education might be more important than keeping up with others.

- Time-bound: Set deadlines to stay on track. “Save $60,000 for an MBA by January 2027” is a specific plan.

Let’s see how this works. A client once said, “I want to save for retirement.” That’s a good start, but it’s too vague. After using SMART, we made it clear: “Save $1.5 million by 67 by putting in $1,850 monthly into a 70% equity portfolio.”

This clear plan gives us specific numbers to aim for. It tells us how much to save, when, and how to invest. This clarity helps you reach your goals by removing confusion and keeping you accountable.

The difference between hoping and planning is measurement. When we measure, we manage.

Your investment plan needs this clarity. For each goal, make a one-page document with SMART details. This document guides you and keeps you from making emotional decisions during market ups and downs.

Even if investments change, your commitment to SMART goals should stay strong. Check your progress every quarter to stay on track. This keeps you focused on reaching your financial goals.

The SMART method is simple yet powerful. It turns vague dreams into clear goals. This discipline is the base of a successful investment plan.

“read more: How to Adjust Investment Goals Over Time“

Prioritize Goals by Urgency and Impact

Building a solid investment strategy starts with prioritizing your goals. Over 12 years, I’ve helped investors create a three-tier framework. This ensures you balance growth and stability, avoiding common financial pitfalls.

Near Term Safety Net Comes First

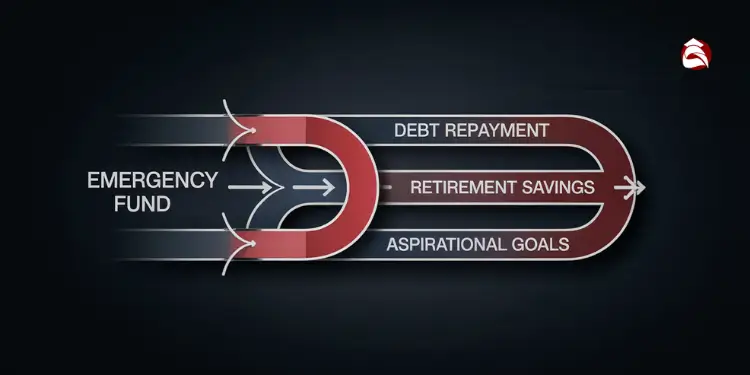

First, build an emergency fund. It should cover 3-6 months of living costs like housing and food. For those with $5,000 monthly needs, aim for $15,000 to $30,000 in liquid assets.

Only 63 % of U.S. adults could cover a $400 emergency with cash, underscoring how critical it is to fund a robust safety net before chasing higher-risk investments.Ref.: “Federal Reserve Board. (2025). Economic Well-Being of U.S. Households in 2024. Board of Governors of the Federal Reserve System.” [!]

Keep these funds in high-yield savings or Treasury bills. Building an emergency fund may not be exciting, but it’s crucial. It protects you from sudden income drops and prevents selling investments too soon.

Many clients have kept their financial plans on track after job losses thanks to this fund. It acts as a financial cushion, keeping your investments safe during market downturns.

Allocate Surplus Toward Growth Opportunities

After securing your emergency fund, focus on employer retirement matches. These can offer a 50-100% return, unmatched by any investment. Think of it as free money that boosts your retirement savings.

Next, tackle high-interest debt and then fill up tax-advantaged accounts like 401(k)s and IRAs. Only then should you invest in taxable accounts for growth.

Fidelity recommends saving 15% of your income for retirement, including employer matches. Set up automatic contributions to keep your savings on track without emotional decisions.

Fidelity’s longevity studies suggest saving about 15 % of pre-tax income—including any employer match—gives most workers a high probability of sustaining their lifestyle in retirement.Ref.: “Fidelity Investments Editorial Team. (2025). How Much Should I Save for Retirement? Fidelity Investments.” [!]

For most, the order makes sense:

- Emergency fund (3-6 months expenses)

- Employer retirement match

- Debt above 5% interest

- Remaining tax-advantaged space

- Taxable investments

Review your priorities every year as your finances change. What’s right for your early career might not be the same as you near retirement. The framework stays the same, but the balance between safety and growth changes with your life stage.

Read More:

Track Progress and Rebalance Regularly

Setting investment goals is just the start of your wealth management journey. I’ve seen many portfolios go off track when investors forget to check on them. To stay on course, check your progress every quarter and do a full portfolio check once a year.

Your investment account changes as markets do. What was a 70/30 mix might become 76/24 in a strong market, increasing your risk. Rebalancing your portfolio when it’s off by 5% or more keeps your risk level right where you want it and might even boost your returns.

Vanguard’s 2022 study finds annual rebalancing best keeps a 60/40 portfolio’s equity weight from drifting toward 80 %, preserving intended risk levels without excessive trading costs.Ref.: “Zhang, Y., Ahluwalia, H., Ying, A., Rabinovich, M., & Geysen, A. (2022). Rational Rebalancing: An Analytical Approach to Multiasset Portfolio Rebalancing Decisions and Insights. Vanguard Research.” [!]

Create a simple tracking system with these elements:

• Each goal’s target amount and timeline

• Current portfolio value

• Progress percentage toward each goal

• Required monthly contributions

• Year-to-date actual contributions

Life changes—like a new job, getting married, or having kids—mean you might need to adjust your investments. If you’ll need money sooner, you might want more liquid investments. After paying off debt, you could put that money toward long-term goals.

Have an annual “financial physical” to check if your goals and risk tolerance still match your life. This regular check-up stops small mistakes from becoming big problems. It keeps your investment strategy working for you as your needs change.

{kind=link}