Your investment goal time horizon is key to every money choice you make. It’s the time from now until you need your money for something. This could be a big purchase or a goal you’re saving for.

Ever wondered why some people stay calm when the market drops? Others panic. It’s often because of their planning timeline. A 2023 Fidelity survey found 72% of Americans don’t match their investing strategy to when they’ll need their money.

Warren Buffett said, “The stock market is designed to transfer money from the active to the patient.” I’ve seen how clients changed their results by linking each financial goal to the right.

The time you plan to keep money invested matters. Someone saving for retirement decades away has different choices than someone saving for next year’s vacation.

Quick hits:

- Short-term needs demand safety first

- Longer periods allow growth focus

- Match strategy to your deadline

- Different purposes need different approaches

- Patience rewards disciplined planning

Time horizon categories and their traits

Investment time horizons split your financial plan into three main parts. Each part needs a special way to handle risk and return. I’ve helped many investors see how the right strategy for their time frame improves their results.

Let’s look at how these time frames shape your investment choices and how to build your portfolio.

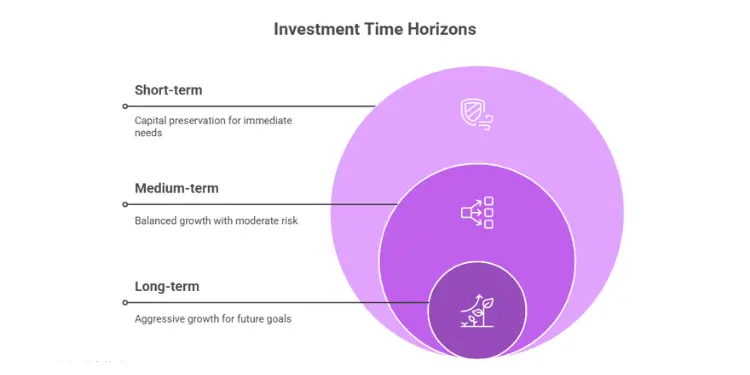

Short Span Capital Preservation Focus

A short-term time frame is from now to three years. Here, your main goal is to keep what you have safe, not to grow it fast.

Capital preservation is key here. Why? Market ups and downs can hurt your money if you can’t wait for it to get better. For short-term goals, think about these things:

- Liquidity is more important than making more money

- Stay away from big market swings

- Choose stable, easy-to-predict investments

- Accept lower returns for the safety they offer

Short-term goals are like saving for an emergency, a vacation, or a big buy in a few years. The main goal is to keep your money safe and ready when you need it, not to make a lot of money.

Medium Term Balanced Growth Approach

Medium-term time frames are from 3 to 10 years. This time needs a balanced strategy that aims for growth but also keeps risks in check. Your money should grow but not too fast or too slow.

The balanced strategy includes:

- A moderate risk level with a mix of investments

- Investments that grow and also make income

- Regularly check and adjust your investment mix

- Enough time to bounce back from small market drops

Medium-term goals are like saving for a house, a kid’s education, or a career change. This time lets you aim for meaningful investment goals while keeping some safety against market drops.

Long Horizon Aggressive Accumulation Opportunities

A long-term time frame is more than 10 years. It lets you take bigger risks for bigger rewards. Market ups and downs don’t worry you as much because you have time to wait for things to get better.

The long-term horizon has big advantages:

- It’s easier to handle market changes

- Chance to get higher returns from investments that grow

- Benefits from returns adding up over a long time

- Flexibility to change strategy as needed

Retirement planning is the main goal for long-term horizons. But, building wealth for the future or for your kids also fits here. With decades to go, you can focus on investments that grow more over time.

The longer you invest, the more you can handle market ups and downs. What might seem risky in the short term becomes a smart choice for the long haul.

| Time Horizon | Primary Focus | Typical Goals | Risk Tolerance |

|---|---|---|---|

| Short-term (0-3 years) | Capital preservation | Emergency fund, vacation, major purchase | Very low |

| Medium-term (3-10 years) | Balanced growth | Home down payment, education, career change | Moderate |

| Long-term (10+ years) | Aggressive accumulation | Retirement, wealth building, legacy planning | Higher |

Knowing these time horizons helps you make investment choices that match your goals. Each time frame needs its own way to pick investments, manage risks, and set goals. The key is to match your investment strategy to the right time frame, not to use the same plan for everything.

Read More:

Mapping personal goals to horizons

Linking your financial goals to specific times helps make plans clear. Investors who connect their goals to timeframes make better choices. This turns vague dreams into clear, measurable goals.

Your investment goals should match your life’s path. A 35-year-old saving for a vacation home and retirement needs different plans. A 50-year-old balancing college funds and business sale also needs specific strategies.

The key question is “When will I need this money?” Your answer guides every investment choice. Goals fall into different time frames:

- Short-term goals (0-3 years): Emergency funds, vacation savings, home down payments, wedding expenses

- Medium-term goals (3-10 years): College funding, career sabbaticals, major home renovations

- Long-term goals (10+ years): Retirement, generational wealth transfer, early financial independence

Many investors use one strategy for all goals. But this rarely works. I suggest separate plans for each time frame.

Choosing Targets Based on Life Events

Life events set natural deadlines for your goals. Events like marriage or buying a home change your financial plan. Each event needs careful planning of when you’ll need money.

Saving for retirement is flexible, but college funds are not. You can delay retirement but not your child’s college start. This affects your time horizon for your goals and investment strategies.

Consider these common life events and their typical time horizons:

| Life Event | Typical Time Horizon | Flexibility Level | Investment Approach |

|---|---|---|---|

| Emergency Fund | 0-1 years | None | Capital preservation |

| Home Purchase | 1-5 years | Moderate | Conservative growth |

| College Education | 5-18 years | Low | Age-based allocation |

| Retirement | 10-40+ years | High | Long-term growth |

| Legacy Planning | 30+ years | Very High | Aggressive growth |

When goals compete for money, prioritize them. Use urgency, importance, and consequences to rank goals.

For example, an emergency fund is more urgent than vacation savings. Retirement often takes priority over helping adult children, despite emotional appeal.

The most successful investors I’ve worked with revisit their goals annually, adjusting time horizons as life circumstances change. Flexibility is your ally when mapping goals to horizons.

Life is rarely straightforward. Career changes or health issues may change your goals. Adjusting your strategy is key to success.

Setting goals with specific time frames is about peace of mind. Knowing when you’ll need money and having a plan reduces stress and prevents bad decisions.

Selecting securities for each timeframe

Different timeframes need different securities for safety and growth. Your investment horizon helps choose the right vehicles for your goals. Let’s match your investment choices with your time horizon.

Cash Equivalents for Near Needs

For goals in 0-3 years, keeping your money safe is key. Look for stable, easy-to-access investment products.

High-yield savings accounts are great for short-term goals. They offer FDIC insurance and higher interest rates than regular savings. I suggest them for down payments or vacations.

Money market funds are also good for short-term. They invest in short-term debt and keep a stable value. They offer better yields than savings accounts but are just as liquid.

Certificates of deposit (CDs) are another option. They offer returns above savings rates but have less liquidity. Early withdrawals may have penalties. CDs are good for specific goals with known dates.

Short-term bonds and Treasury bills are also good for short-term needs. They offer higher returns than cash with little risk. Keep money you’ll need in a year in these investments.

| Time Horizon | Primary Investment Types | Typical Allocation | Key Benefit |

|---|---|---|---|

| 0-1 year | High-yield savings, money market funds | 90-100% cash equivalents | Maximum liquidity |

| 1-3 years | CDs, short-term bonds, Treasury bills | 70-90% fixed income, 10-30% cash | Stability with modest yield |

| 3-7 years | Balanced funds, dividend stocks | 40-60% stocks, 40-60% bonds | Growth with moderate risk |

| 7+ years | Stock funds, growth investments | 70-90% stocks, 10-30% bonds | Maximum growth |

Equities Dominate Multi-Decade Goals

For goals over 10 years, the investment landscape changes. Long-term goals like retirement or college funding allow for market volatility. This lets you capture the growth of equities.

Stocks have outperformed bonds and cash over decades. The S&P 500 has averaged 10% annual returns. Bonds and cash have averaged 5-6% and 3%, respectively.

For goals 15+ years away, I recommend 80-90% in diversified investments. Bonds make up 10-20% to reduce volatility.

Target-date funds are a simple way to manage retirement savings. They adjust their stock and bond mix as your goal date nears. For example, a 2060 fund starts with 90% stocks and shifts to bonds as 2060 approaches.

For long-term goals, choose low-cost, diversified options. A three-fund portfolio of U.S. stocks, international stocks, and bonds is a good start. This approach balances growth and diversification.

For medium-term goals (3-10 years), a balanced mix works best. Consider dividend stocks, intermediate-term bonds, and alternatives. A 50/50 or 60/40 stock/bond mix offers growth with limited risk.

“The single greatest edge an investor can have is a long-term orientation.”

Riskier investments become safer with time. Daily market ups and downs matter less for long-term goals. What’s key is matching your investments to your time horizon and staying disciplined.

Your investment strategy should change as your goals do. As goals near, move from growth to stable investments. This should be a planned move, not a reaction to market changes.

Adjusting horizon after market swings

Market swings mean you might need to change your investment plan. It’s key to know when to adjust and when to stay the same. I’ve seen many investors make big mistakes by reacting too fast to market changes.

Big drops or sudden rises in the market can change how long you should hold onto your investments. This is called horizon risk. It’s when your investment time might get shorter because of things outside of the market.

When to Extend Your Time Horizon

After big drops, your portfolio might need more time to get back to where it was. Knowing your time horizon is very important here. If you can, make your timeline longer to avoid losing money during bad times.

Here are some tips for when markets fall:

- Change your retirement date if your portfolio drops but your income stays the same

- Wait to buy big things to let your investments recover

- Save more money to make up for lower returns

- Keep your investments spread out to help them recover faster

I once helped a client who was close to retirement during the 2008 crisis. By waiting just 18 months and working part-time, his portfolio recovered a lot. This move saved him from selling too early and losing years of retirement income.

When to Shorten Your Time Horizon

But, if the market does well, you might reach your goals sooner. This is a chance to adjust your investing to reach your goals faster.

When you do better than expected, think about:

- Locking in gains for goals that are now within reach

- Moving some money to safer investments

- Checking if you can handle more risk as your time gets shorter

- Building a bigger cash reserve to protect against future ups and downs

Good returns might let you reach your goals sooner. But, don’t throw away your whole plan. Just adjust parts of your portfolio to keep moving forward.

Guarding Against Horizon Risk

Horizon risk isn’t just about market changes. Life events can also force you to sell too soon. For example, losing your job or unexpected big expenses like home repairs might make you sell investments you meant to keep long-term.

To avoid this risk, have some short-term investments in your mix. This creates a safety net to help you avoid selling long-term investments when markets are down.

A good strategy is to keep:

- 3-6 months of expenses in cash for emergencies

- 1-2 years of planned withdrawals in safe investments if you’re near or in retirement

- A small part of your portfolio in short-term bonds, even if you’re aggressive

As you get older or get closer to your goals, your investments should get more conservative. This isn’t about reacting to the market. It’s about adjusting to your changing needs.

The most important thing is to tell the difference between emotional reactions and real changes. Market ups and downs shouldn’t usually change your plan. But, big life changes or huge portfolio swings might mean it’s time to think about adjusting your investment timeline.

Common horizon mistakes and fixes

Many people make big financial mistakes because they don’t match their money needs with their investments. I’ve seen many investors make the same errors over and over again. These errors can ruin their financial plans before they even start.

These mistakes often come from not understanding how time and risk work together. When people don’t match their investments with their time needs, they hurt their own financial goals.

The good news is that most of these mistakes can be avoided. With the right planning and knowledge, you can fix these common errors.

Misreading Deadline Flexibility Costly Consequences

One big mistake is thinking deadlines are more flexible than they really are. I’ve seen people saving for a home in two years invest in stocks. They think they have more time than they really do.

When the market gets tough, these investors have to choose between buying a home or losing money. They often sell at the worst time, losing a lot of money. This could have been avoided if they matched their investments with their deadlines.

On the other hand, some people treat long-term goals like retirement as if they were short-term. This means they invest too safely. A 35-year-old might keep their retirement savings in cash or bonds, thinking they’re safe from market swings. But, inflation can slowly reduce their money’s value over time.

Inflation is the most powerful argument for equity exposure in long-term investment horizons. Even modest 3% annual inflation cuts purchasing power in half over 24 years.

Another mistake is not changing your investment plan as your goals get closer. Many people set their investment strategy based on their initial time horizon. But, they don’t adjust it as that time gets shorter. The plan that was perfect for retirement 20 years ago might not be right anymore.

Using the same investment plan for all your goals is also a mistake. Different goals need different timelines and investment strategies. Your emergency fund, home down payment, and retirement savings should not all be invested the same way.

Ignoring tax implications can also hurt your returns. Short-term and long-term investments are taxed differently. Some accounts, like IRAs and 401(k)s, are better suited for certain time horizons.

Letting emotions control your investment decisions is another big mistake. When the market drops, many investors sell too early, missing out on future gains. During good times, they take too much risk with money they’ll need soon.

| Horizon Mistake | Potential Consequence | Practical Fix |

|---|---|---|

| Treating short-term goals as long-term | Forced selling during market downturns | Match investment volatility to actual time need |

| Treating long-term goals as short-term | Inflation erosion of purchasing power | Accept appropriate volatility for distant goals |

| Failing to adjust as horizons shorten | Excessive risk near goal completion | Schedule annual horizon reviews and adjustments |

| Using single horizon for all assets | Misaligned risk across different goals | Segment portfolio by specific goal timelines |

Fixing most horizon mistakes starts with being honest about when you need your money. For each goal, ask yourself: “What would happen if this money wasn’t available when needed?” If the answer is big trouble, you need to invest more conservatively as the deadline gets closer.

For long-term goals like retirement, the biggest risk isn’t short-term market swings. It’s not growing enough to keep up with inflation over time. These investments need to grow fast enough to beat inflation, even with market ups and downs. Remember, even at retirement, you have the rest of your life to plan for.

Reviewing horizons during annual check

Your investment goal time horizon isn’t fixed. As you get closer to your financial goals, your timeline gets shorter. You’ll need to adjust your portfolio. It’s smart to plan an annual review to make choices wisely, not when the market is shaky.

At your yearly review, check if your target dates are realistic. A goal for retirement in 15 years becomes 14 years after just one year. Investment horizons affect both risk and what you invest in. So, you’ll need to make changes as your deadline gets closer.

Then, look at your asset allocation. As your long-term investment time gets shorter, start moving from growth to preservation. For example, when you’re five years from retirement, cut stock exposure by 5-10% each year.

Life changes can also change your investment time. Getting married, having kids, or changing jobs can make your timeline longer or shorter. Keep track of these changes to stay on track with your investing.

Studies show that reviewing financial goals and investment horizons yearly helps people meet their goals 40% more often. Make a simple checklist for your review:

• Check if your goal deadlines are right

• Adjust your investments as your time horizon gets shorter

• Look at new goals and their timelines

• See how your investments are doing against your targets

Remember, your investing time horizon is key to your strategy. Regular reviews keep your portfolio in line with your changing financial needs.

{kind=link}