The journey to financial success starts long before you buy anything. I’ve helped hundreds of new investors and seen a common problem. Many hurt their financial future before they even begin.

Is making money about picking the right stocks, or is there something deeper? A Dalbar study found that average investors earn just 5.19% a year. Meanwhile, the S&P 500 makes 9.85% – not because of bad choices, but because of poor planning.

“The difference between success and failure isn’t about timing the market,” says Warren Miller, a seasoned financial advisor. “It’s about knowing what success means for you.”

I recall a client who had saved for years but felt lost. He didn’t need to change his investments. He just needed to set clear, structured goals.

This article will show you six big planning mistakes beginners make. Each mistake has a simple fix you can start today. Fixing these basics will help you build a strong strategy, not a shaky one.

Key takeaways:

- Proper financial planning frameworks matter more than market timing

- Clear, realistic objectives aligned with personal circumstances create sustainable growth

- Emotional decision-making undermines even well-selected portfolios

- Long-term vision beats short-term reactions in building wealth

Rushing Targets Without Financial Baseline

Many beginners rush into investing without a solid financial plan. They aim to grow their wealth fast but often face a harsh reality later. First, you must understand your current financial situation.

Knowing your financial health is key to making smart investment choices. It’s like building a house. You start with the foundation, not the roof. Setting goals needs a clear view of your finances.

When I meet new clients, I first map their financial situation. We track income, expenses, assets, and liabilities over six months. This baseline is crucial for setting achievable goals.

Bankrate’s 2025 Money & Mental Health Survey found that only 29 % of Americans reviewed their household budget in the prior 30 days—highlighting why a tracked financial baseline is essential before setting investment targets. Ref.: “Bankrate Staff. (2025). Survey: More Than Two-Thirds of Americans Aren’t Reviewing Their Budget. Bankrate.” [!]

Ignoring Income Stability Realities Today

Beginners often overlook their income stability when setting targets. Your income type greatly affects your investment strategy.

For example, if your income varies, setting fixed investment goals is risky. I advised a freelance designer to invest a percentage of her income instead of a fixed amount.

She struggled to meet her targets and eventually gave up. Setting goals based on a percentage of income is more realistic.

Before investing, document your income for six months. Look for patterns and be honest about job security. This helps set targets you can consistently meet.

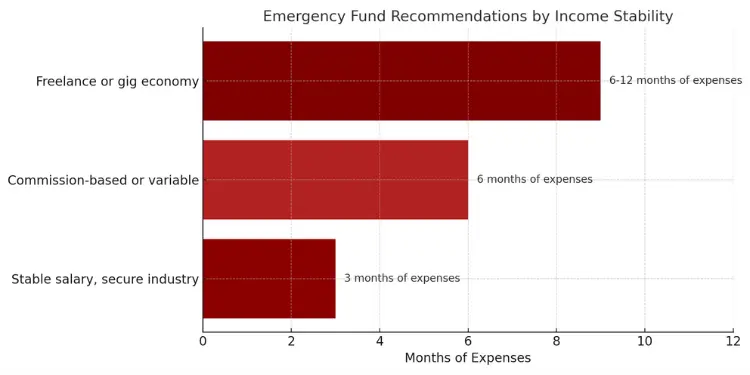

Skipping Emergency Fund Foundation Step

Beginners often skip building an emergency fund before investing. This is a critical mistake.

Without 3-6 months of expenses in a savings account, you’re at risk. Unexpected costs can force you to sell investments at bad times.

The emergency fund isn’t just financial protection—it’s psychological freedom that allows you to stay invested during market downturns.

I’ve seen beginners invest too much, then face unexpected bills. Without an emergency fund, they must sell investments during downturns. This leads to losses and missed recovery opportunities.

Before investing, build an emergency fund. Start with one month’s expenses and aim for 3-6 months based on your income. Only then can you decide how much to invest.

| Income Stability | Recommended Emergency Fund | Investment Approach |

|---|---|---|

| Stable salary, secure industry | 3 months of expenses | Regular, automated contributions |

| Commission-based or variable | 6 months of expenses | Percentage-based contributions |

| Freelance or gig economy | 6-12 months of expenses | Lump-sum investing during high-income periods |

Successful investing starts with managing money basics. Document your cash flow, build an emergency fund, and then invest. This method may seem slow, but it’s essential for long-term success.

Setting Vague Aims Lacking Measurability

After twelve years of advising investors, I see a common mistake. People set financial targets that are hard to track or achieve. Saying “I want to grow my money” is not a goal—it’s a wish. When clients say they want to “save for retirement” or “build wealth,” I know it often leads to disappointing results.

Vague objectives cause three big problems. First, you can’t measure progress without clear goals. Second, picking the right investments is hard without a clear goal. Third, it’s tough to stay disciplined when markets change without clear success benchmarks.

Let’s look at how I help clients change their goals. Instead of “save for retirement,” we set specific targets like “Accumulate $1.2 million by age 62 to generate $48,000 annual income.” This clear goal helps choose the right investments and how much to save.

Without concrete numbers, investors drift between strategies based on recent performance rather than long-term fit.

To set financial goals that work, include four key elements:

- Specific dollar amount needed – Define exactly how much money you need to achieve your objective

- Target date – Establish when you need to reach this financial milestone

- Required monthly contribution – Calculate what you must invest regularly to stay on track

- Minimum return rate necessary – Determine the performance your investments must generate

Being specific turns hopes into real plans. When markets change, clear goals help you see if it’s a problem or normal.

Many investors give up good strategies during market dips. They can’t tell if the drop affects their goals. Without clear targets, emotions guide decisions, not facts.

Short-term goals need the same clarity as long-term ones. Saving for a home in two years or retirement in twenty needs specific targets. Vague goals lead to vague results. Specific goals lead to specific achievements.

Take a moment to check your investment goals. If they lack numbers, dates, and returns, they’re wishes, not goals. Use the four markers to make them clear, and you’ll know which investments fit your needs.

Overestimating Returns Versus Risk Tolerance

Many beginners make a big mistake by thinking they can get high returns without taking big risks. Over the last 12 years, I’ve seen many investors dream of 12-15% annual returns. But this dream is based on recent highs, not reality.

People often think they can handle market ups and downs, but reality is different. I’ve seen investors who thought they were okay with risk, but panicked when their investments fell 20%. This mismatch can ruin a good financial plan.

Risk tolerance is more than just a number. It’s how you act when things go wrong. Many investors think they can handle volatility until they face their first big loss. Your investment plans should match your goals and how well you can handle market swings.

Vanguard finds that investors who panic-sell to cash for a year have an 87 % probability of underperforming those who stay balanced—proof that misjudged risk tolerance, not poor picks, often sinks returns. Ref.: “Vanguard. (2025). Answering Our Investors’ Top Market Volatility Questions. The Vanguard Group.” [!]

“read more: How to Adjust Investment Goals Over Time“

Confusing Past Performance With Guarantees

Thinking past success means future wins is a big mistake. Using last year’s S&P 500 returns to plan your retirement can lead to disappointment.

Equity returns have averaged 7-10% over the long term, but there’s a lot of variation. The same market that gave you 30% gains one year might lose money the next. Mutual funds warn about past performance not predicting future results for a reason.

The most successful investors I’ve worked with build their financial plans using conservative return assumptions, then treat any outperformance as a bonus that accelerates their timeline.

It’s smarter to use 2-3% less than historical averages when planning. If your portfolio does better than expected, you can speed up your goals or lower contributions. This way, your plans are based on what’s likely to happen, not just what might.

Your investment mix should match your goals and how comfortable you are with risk. If a 20% drop in your portfolio would make you give up, you need to rethink your risk level.

Market trends are unpredictable, and no one can guess them all. A diversified portfolio that you can stick with through ups and downs is more valuable than chasing high returns that are too risky.

“read more: How to Determine Your Investment Goals Properly“

Neglecting Timeline When Choosing Assets

Choosing investments based on your time horizon is key to achieving goals. Yet, many beginners overlook this. In my 12 years of advising, I’ve seen many make the mistake of not matching their investments with their timeline.

Many new investors pick investments based on recent success, not their timeline. Investing in growth stocks for a short-term goal can be risky. The market doesn’t care about your deadlines, and short-term ups and downs can hurt your money.

The SEC’s Beginner’s Guide states that an asset mix must adjust as your goal date nears—long horizons can weather stock volatility, while money needed within three years belongs in cash or short-term bonds. Ref.: “U.S. Securities and Exchange Commission. (2025). Beginners’ Guide to Asset Allocation, Diversification, and Rebalancing. Investor.gov.” [!]

Time in the market beats timing the market, but only when your investment timeline matches your asset selection.

On the other hand, keeping retirement funds in low-risk investments for too long can be a problem. This approach can lead to losing purchasing power over time. Understanding the link between time and risk is crucial for setting financial goals.

I tell clients to divide their investments into buckets based on time frames:

| Time Horizon | Appropriate Assets | Primary Focus | Risk Level |

|---|---|---|---|

| Short-term (0-3 years) | High-yield savings, short-duration bonds, and money market funds | Capital preservation | Low |

| Mid-term (3-10 years) | Balanced funds, moderate bond/stock mix, dividend stocks | Moderate growth with stability | Medium |

| Long-term (10+ years) | Growth stocks, index funds, and real estate investments | Maximum growth potential | Higher |

For long-term goals like retirement, your timeline helps you handle market ups and downs. A 35-year-old can take on riskier investments for retirement. This approach offers the best chance for growth over time.

Each goal needs its own timeline and investment plan. This prevents using the same strategy for all goals. Your down payment fund and retirement account should not be treated the same.

Your timeline can change as you get closer to your goals. As your goal nears, your investments should become more conservative. What’s right for a long-term goal becomes too risky as the time frame shortens. Adjusting your investments as your goals approach is key to reaching financial freedom.

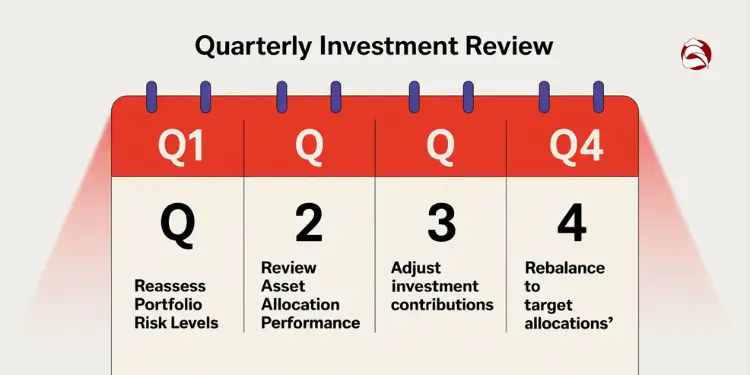

Failing to Revisit Goals Periodically

Investment goals change with a changing market. Many investors set goals but then forget about them. They keep putting money into their accounts but don’t check if it still fits their lifestyle.

About 70% of Americans who make financial plans don’t stick to them. This is often because they forget the importance of regular financial checks, which can ruin even the best investment plans.

Scheduling Annual Progress Reviews Routine

Set aside time each year to check on your investment goals. Look at your progress, whether your goals are still relevant, and whether you need to change how much you contribute. This will keep you on track.

Track your investment goals using a straightforward method. Include the target amount, timeline, current progress, and how much you must contribute each month. Regular checks can help you progress 40% faster than setting and forgetting about goals.

SEC guidance advises rebalancing portfolios at least every 6–12 months; neglecting these checkpoints allows asset drift that silently inflates risk beyond your stated goals. Ref.: “Schock, L. (2024). Is It Time to Rebalance Your Investment Portfolio? Investor.gov.” [!]

Updating Contributions After Life Changes

Life changes mean you need to update your goals right away. Things like getting married, having kids, changing jobs, getting an inheritance, or dealing with health issues affect your money.

If you get a raise, use at least 50% of it to reach your goals faster. Don’t let it all go to lifestyle upgrades. If your income decreases, you must adjust how much you contribute to avoid financial trouble.

Read More:

Your investment goals should grow with your life. Without updating them, all your hard work won’t help you achieve financial security in the long run.

{kind=link}