Americans who implement a zero-based budget save 18% more annually compared to those who don’t, according to surveys conducted in Financial Peace University classes. This is compared to those who don’t use this method. A zero-based budget helps you reach your money goals faster. It does this by giving each dollar a job.

I learned about this when I wanted to save for my first home. What seemed like a long wait was actually just 18 months. The trick wasn’t making more money. It was using what I had wisely.

A zero-based budget means your income minus your expenses equals zero. It doesn’t mean you spend all your money. Instead, every dollar is used for bills, groceries, debt, and saving.

This budgeting technique makes saving faster than usual. It helps you reach your savings goals quicker. This is because you’re directing money to specific places.

Want to make your savings grow? Let’s see how to use this method in your daily money life.

- Assigning Every Dollar: The Core of Zero-Based Budgeting

- This method typically helps people save 15-20% more without increasing income

- You’ll gain complete visibility into where your money goes each month

- The approach works for any income level and adapts to changing financial goals

Transforming Leftover Dollars with Single-Purpose Funds

The single-purpose fund concept changes how we save money. It makes sure extra cash goes toward real goals, not just sitting around. I used to let my “someday fund” get spent on things I didn’t need until I found a better way.

When you save for one thing, it feels like a mission. This fits well with zero-based budgeting, where every dollar has a job. Your money then has direction and purpose.

Imagine saving for “miscellaneous future expenses” versus “my family’s dream vacation to Yellowstone next summer”. Saving for a specific goal feels more meaningful.

The Power of Specific Savings Goals

Research indicates that individuals with specific, written goals save significantly more than those with vague or no goals. Our brains like clear goals better than vague ones.

I learned this the hard way. My emergency fund never grew because it didn’t have a clear goal. Every time it hit $1,000, I’d spend it on something else. It wasn’t about being disciplined, but about not knowing what to save for.

When I named my savings accounts for specific goals, like “New Laptop Fund” or “Holiday Gift Budget”, things changed. Those accounts felt harder to spend on other things. Just naming them helped me stay focused.

The more specific your savings goal, the more likely you are to achieve it. Vague intentions produce vague results.

Specific savings goals enhance saving behaviors. Research indicates that individuals with clearly defined savings targets exhibit higher saving rates, particularly as they approach their goals. Ref.: “Consumer Financial Protection Bureau. (2022). Consumer Savings App Strategies and Savings Outcomes.” [!]

Single-purpose funds also show you how close you are to your goal. This makes saving more motivating. It helps you stay on track, even when it’s hard.

Knowing exactly how close you are to your goal makes managing money easier. You get to plan your finances with precision, not just vague savings.

| Feature | Single-Purpose Fund | Generic Savings | Psychological Impact |

|---|---|---|---|

| Goal Clarity | Specific target with deadline | Vague “someday” purpose | Increased commitment and focus |

| Emotional Connection | Strong attachment to outcome | Minimal emotional investment | Greater resistance to impulse spending |

| Progress Tracking | Clear percentage toward completion | Arbitrary growth metrics | Regular motivation boosts |

| Success Rate | 27% higher savings rate | Baseline savings rate | Increased financial confidence |

| Spending Temptation | Low – purpose creates boundary | High – flexible purpose enables raids | Reduced financial guilt and stress |

Focused savings goals do more than just help you reach your goal. Each time you succeed, you build confidence and good money habits. You’re not just saving money; you’re changing how you think about it.

When I started saving this way, I saved more. My money seemed to go further because every dollar had a purpose.

This way of saving feels empowering. Instead of feeling like you’re missing out, you look forward to what you’re saving for. Saving becomes a smart choice, not just a sacrifice.

Setting Clear and Inspiring Financial Targets

Choosing a specific savings goal is key to success. It turns vague dreams into real actions. Zero-based budgeting needs a clear goal to work well.

I learned this the hard way. I saved for “home repairs” without a clear plan. My savings kept getting used for other things. It wasn’t my lack of discipline that failed me, but my unclear goal.

Your goal should excite and be clear. Think about what would really make your life better. This focus helps you save more each month.

New Laptop or Semester Fees Work Better Than Vague Rainy Day

Goals like “$1,200 for a new laptop” are better than a “rainy day fund”. They give you a clear goal that motivates you. This helps you avoid spending too much elsewhere.

When setting your goal, remember these three things:

- Exact dollar amount – Know exactly how much you need ($1,200, $3,500, $5,000)

- Specific deadline – Set a date to create urgency (3 months, 6 months, 1 year)

- Clear purpose – Know what the money is for (laptop, tuition, vacation)

This way, you have a clear goal to reach. Zero-based budgeting needs this precision to work. Without it, saving can feel aimless.

The more specific your financial goals, the more likely you are to achieve them. Vague intentions rarely translate into consistent action.

For big goals, break them into smaller steps. Saving $5,000 for a vacation? Celebrate at $1,000, $2,500, and $4,000. These milestones keep you motivated.

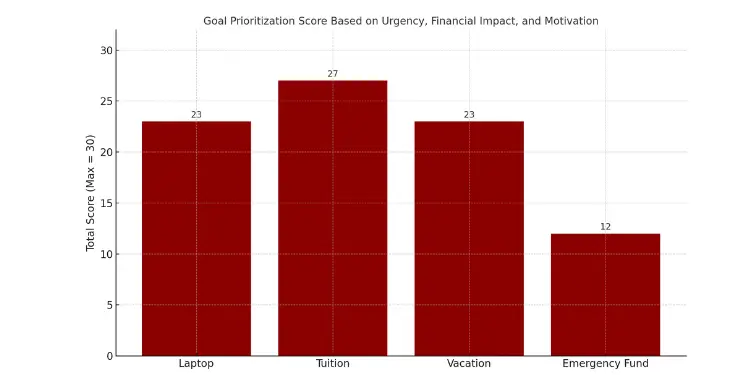

What if you have many goals? This is a common problem. Instead of many funds, pick one goal to focus on first. Choose the goal that means the most to you.

Write down your goals and rate them. Use urgency, financial impact, and emotional motivation. Pick the goal with the highest score to focus on first.

Remember, zero-based budgeting makes you think about every dollar. Applying this to your savings goal helps you stay focused on what’s important.

Automating Savings Through Micro Transfers

Building your zero budget fund is easy with automated micro transfers. You don’t have to wait until the end of the month to save. Small amounts moving in throughout the month build momentum.

Automation takes the willpower out of saving. Your system works quietly while you live your life. Your future self will be grateful for this invisible discipline.

Most banks let you set up automatic transfers. You can move money weekly from your checking to savings. This adds up to $260 a year without feeling it.

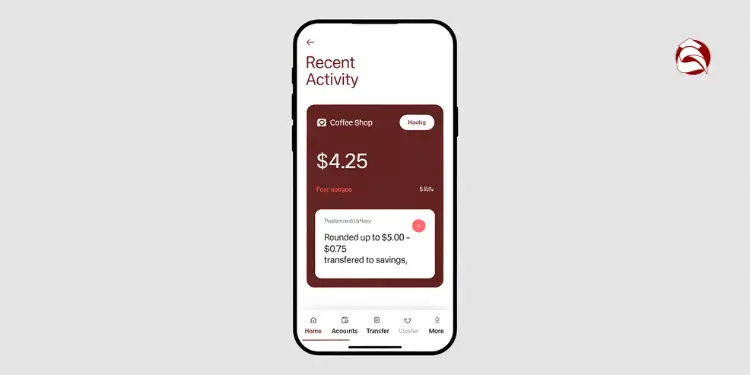

Utilizing Round-Up Apps for Effortless Saving

Round-up apps automatically round up your purchases to the nearest dollar, saving the difference. When you spend $4.25 on coffee, it rounds up to $5. The extra $0.75 goes to savings. This turns spending into saving.

Users can save substantial amounts over time by consistently using round-up features on everyday purchases. It worked because it was tied to something I did often but not every day.

While round-up savings apps like Qapital and Acorns offer convenient saving mechanisms, they often come with monthly fees ranging from $3 to $12. Users should assess whether the benefits outweigh the costs based on their saving habits. Ref.: “Money Crashers. (2025). The Best Round-Up Savings Apps of 2025.” [!]

Several apps facilitate saving through unique features:

| App Name | Key Features | Cost | Best For | Transfer Speed |

|---|---|---|---|---|

| Acorns | Round-ups + investment options | $3-5/month | Investment-minded savers | 2-3 business days |

| Qapital | Custom rules (like save when under budget) | $3-12/month | Creative rule-makers | 1-2 business days |

| Chime | Automatic 10% of deposits saved | Free | Simplicity seekers | Instant |

| Digit | AI analyzes spending to save optimally | $5/month | Hands-off savers | 1 business day |

| Bank Round-ups | Built into existing accounts | Usually free | Bank-loyal customers | Same day |

To find the best daily categories for micro-transfers, look at your spending. Find small purchases where you can save a dollar or two. Coffee, lunch, or convenience store stops are good choices.

Setting up your system takes just minutes. First, connect your spending account to your app. Then, choose your rules, like round-ups or saving when you’re under budget. Lastly, link your savings account.

Manual methods work too. Try the envelope method or round up your purchases mentally. This way, you save without apps.

Remember, every dollar needs a job in zero-based budgeting. Save every spare penny to make progress. Small, regular transfers work better than big, sporadic ones.

Adjust your budget as you get used to micro-transfers. You might save more without feeling it. Start with 50 cents and increase as you get comfortable.

Maximizing Savings with High-Yield Accounts

Choosing the right place for your zero budget fund is key. It turns saving into growing. After you start saving money, you need to find a good spot to keep it.

As of June 2025, high-yield savings accounts offer competitive interest rates up to 5.00% APY, providing a secure and accessible way to grow your savings. They’re insured by the FDIC, so your money is safe.

I learned the hard way. I kept my vacation money in a regular account. It earned almost nothing. Then, I moved it to a high-yield account. It earned 4.25% interest, adding $425 a year to my savings.

Currently, several high-yield savings accounts offer attractive rates suitable for your zero-based budgeting goals. The LendingClub LevelUp Savings account offers up to 4.40% APY with no fees and no minimum balance requirement. Every dollar you save starts working for you right away.

As of June 2025, top high-yield savings accounts offer Annual Percentage Yields (APYs) up to 5.00%, significantly higher than traditional savings accounts. For instance, Varo Bank and Fitness Bank provide APYs at this rate, enhancing savings growth. Ref.: “Investopedia. (2025). Best High-Yield Savings Accounts for June 2025.” [!]

Look for these features in a high-yield account:

- Easy online access and management

- Free transfers between your primary bank

- Mobile app capabilities for tracking growth

- The ability to nickname accounts based on your savings goal

- No hidden fees that eat into your progress

Separate sub-account keeps temptation out of sight and mind

Using a separate account for your zero budget fund is powerful. It keeps your savings separate from your everyday money. This makes it easier to save for a specific goal.

I learned this when my vacation fund kept disappearing. Moving it to a separate account solved the problem. It made it harder to spend the money impulsively.

Many online banks let you create sub-accounts. Each can have its own name and purpose. This makes it easy to see your savings for different goals in one place.

Here are some tips for using a separate account:

- Name your account after your goal (“New Laptop 2024”)

- Set up direct deposit to save money automatically

- Remove the account from your main app’s dashboard

- Wait 48 hours before making withdrawals

If you have many goals, make separate accounts for each. This helps you save for each goal without mixing funds. It also lets you see how you’re doing on each goal.

Utilizing separate, named savings accounts for specific goals can enhance financial discipline and reduce impulsive spending. This strategy aligns with zero-based budgeting principles by assigning clear purposes to each dollar saved. Ref.: “Ramsey Solutions. (2025). Zero-Based Budgeting: What It Is and How to Use It.” [!]

While many high-yield savings accounts traditionally limit withdrawals, some banks have relaxed these rules, offering more flexibility. But, many banks have relaxed these rules. This helps you avoid dipping into your savings too often.

Visualizing Progress and Celebrating Milestones

Seeing your savings grow is more fun when you can watch it happen. Bank statements only show part of the story. Visual tracking lets you feel the rewards of saving, keeping you going even when it’s hard.

I learned this the hard way, failing three times before I succeeded. Seeing my progress made all the difference. It turned saving into a fun game with clear goals and rewards.

Every small win makes your brain happy. Visual tracking makes each deposit a step forward. This makes you want to keep going.

Visual tracking of savings progress can boost motivation and commitment. Studies suggest that visual cues, such as progress charts, enhance goal adherence by making achievements more tangible. Ref.: “Wendel, S. (2022). Micro Investment and the Behavioral Economics of Savings: The Power of Small Wins. The Berkeley Economic Review.” [!]

“read also: 50/30/20 budget calculator for quick planning and spending balance guide“

Sticker Charts or App Badges Keep Momentum Alive

Choose a tracking method that fits you. Some like physical reminders, while others prefer digital tools.

When we saved for a Disney trip, we used a big thermometer chart. Each deposit let my kids color in more. It became a fun family activity.

Here are some tracking methods that work:

- Physical trackers: Thermometer charts, sticker calendars, or jar systems where you add a marble for each $10 saved

- Digital solutions: Savings apps with progress bars, goal-tracking spreadsheets, or banking apps with visual goal features

- Social accountability: Shared tracking with a partner or posting milestone updates to supportive friends

Break your goal into smaller parts for milestones. Celebrate at 25%, 50%, and 75% with small rewards. These rewards help you stay on track without spending too much.

“I give myself a $5 treat at each 25% milestone—a fancy coffee or a discount movie ticket. It costs just $15 across my entire savings journey but keeps me motivated for months.” – Maria, paid off $5,200 in credit card debt

Make your rewards match your progress. A small reward at 25% keeps you going without spending too much. Celebrate your final goal with something meaningful that fits your financial values.

Read More:

Setbacks happen, like an unexpected car repair. Don’t give up. Mark the setback clearly. This honest approach helps you start again.

| Tracking Method | Best For | Effort Level | Motivation Factor | Cost |

|---|---|---|---|---|

| Paper Thermometer Chart | Families, visual learners | Low | High (even with kids) | Free (printable) |

| Savings Apps (YNAB, Qapital) | Tech-savvy savers | Medium | Medium-High | $5-15/month |

| Excel/Google Sheets | Data-oriented people | Medium | Medium | Free |

| Physical Jar System | Concrete thinkers, cash users | Low | High | $1-5 for supplies |

| Social Media Updates | Community-motivated savers | Low | High (with supportive network) | Free |

The best tracking systems are easy to see and use often. Keep your tracker where you see it every day. This keeps your goal in mind when you spend money.

Tracking is about celebrating your journey. Each step forward is a chance to praise yourself. This makes saving easier and builds good habits for the future.

Continuing Momentum: Funding Your Next Financial Goal

When your zero-based budgeting method becomes a habit, magic happens. My emergency fund reached its goal, and I felt lost. But then, I knew what to do: keep going.

I didn’t let those automatic transfers go back to spending. Instead, I used them for my next big dream – a new kitchen. My budget stayed flexible, and my savings kept moving forward.

“Read more: 50/30/20 budget for low income households that stretches every dollar“

Try using a “savings ladder” with different funds at each stage. It lets you celebrate small wins and work on big goals. Your monthly budget stays the same, but where your money goes changes.

When picking your next dream, ask yourself three things:

1. Which goal would make me less stressed?

2. What savings goal would make my life better?

3. Which goal fits with my long-term financial plan?

This way of saving grows your money over time. Just like government R&D investments do, your personal savings strategy brings financial security.

As your budget grows, old budgeting rules fade away. The fully funded pot is just the start of a journey. It’s where savings and debt control become easy, all from those extra dollars.

{kind=link}