Does your money just disappear every month? Creating a personal budget helps by sorting out where your money goes. It’s a simple step that brings clarity and control to your finances.

Most Americans don’t know how much they spent last month. Money coach Dave Ramsey says, “You must control your money or it will control you.”

I once wrote down my monthly expenses in simple groups like groceries and rent. It made me see where my money was going, revealing areas where I could save.

Want to understand your money better and take charge of your finances? Here’s how to make a budget that tracks every dollar:

- Sort expenses into Needs, Wants, Goals and assign amounts

- Make tiny categories for hidden costs like gifts and tolls

- Use names that mean something to you to connect emotionally

- Adjust your budget every month to match your spending

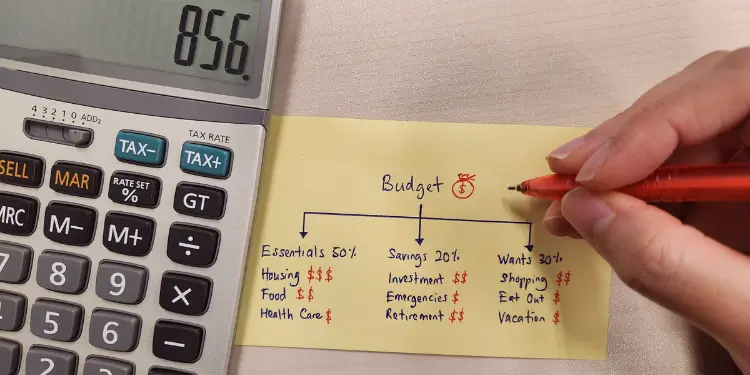

Personal budgeting begins by classifying all expenditures into three primary categories—needs, wants and goals—and assigning specific dollar amounts to each using a zero-based budgeting framework. This approach mandates creation of fine-grained “micro” categories for irregular or low-frequency costs (gifts, tolls, subscriptions) and establishment of sinking funds to amortize lumpy annual obligations (insurance premiums, property taxes, holiday spending) into manageable monthly contributions.

Category names should be personalized to align with individual objectives and values, strengthening commitment to the plan. A monthly reconciliation process compares actual spending against allocations, enabling reallocation of any surpluses to underfunded priorities. A reserved “discretionary” or “fun money” line ensures sustainable adherence by accommodating small indulgences without disrupting core financial targets.

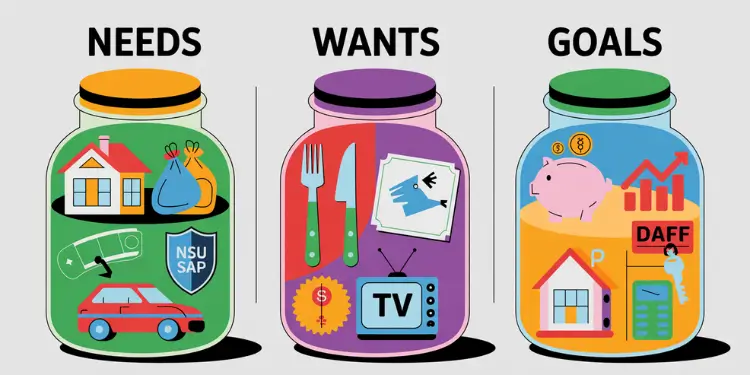

Group Expenses into Needs, Wants, Goals Before Assigning Dollar Amounts

To make a clear budget, start by grouping your expenses. Put them into needs, wants, and goals. This step helps you spend wisely and match your budget to your values.

Expense-tracking and categorization serve as self-regulatory tools, improving spending alignment with goals Ref.: “Zhang, Y. (2023). Financial Self-Regulation: How Does Expense-Tracking Inform Financial Behaviors. Consumer Interests Annual Conference.” [!]

Needs Safeguard Stability While Wants Preserve Joy

Needs are the must-haves for a stable life. They include fixed expenses like rent, utilities, and food. Keep these costs under 30% of your income.

Wants add joy to your life. They are things like dining out and hobbies. But, don’t let wants take over your budget.

Goals are for the future, like saving for retirement. A budget helps you save a little each month. Use special savings accounts to track your progress.

Here’s how you might group common expenses:

| Needs | Wants | Goals |

|---|---|---|

| Rent/mortgage | Dining out | Emergency fund |

| Groceries | Entertainment | Retirement savings |

| Transportation | Subscriptions | Paying off debt |

| Insurance | Shopping | Home down payment |

After sorting your expenses, assign dollar amounts to each category. Use zero-based budgeting to avoid waste. This way, your budget will support your financial goals.

Create Micro Categories for Sneaky Costs Like Gifts and Tolls

When making a detailed budget, it’s key to include all small expenses. These can add up over time. Gifts, tolls, and subscriptions are examples of sneaky costs that can be missed.

By setting up micro categories for these, you can track your monthly bills better. This gives you a clear view of your spending categories.

To find these sneaky costs, check your bank and credit card statements. Look for any regular or one-time charges that don’t fit into your main budget categories. Some common ones include:

- Gifts for birthdays, holidays, and special occasions

- Tolls and parking fees

- Subscriptions and memberships

- Pet expenses like food, toys, and vet bills

- Home maintenance and repairs

Detailed micro-categorization can reduce consistency, as only 32% of Americans review their budget regularly Ref.: “Kates, S. (2025). Survey: More than two-thirds of Americans aren’t reviewing their budgets. Bankrate.” [!]

After finding these costs, make specific micro categories for them in your budget. Put a realistic amount in each based on your past spending and current monthly income. This helps you avoid overspending and reach your financial goals, like cutting spending or paying down debt.

A detailed budget helps you make smart spending choices and reach financial stability. By including even the smallest expenses, you’re on your way to a budget that suits you.

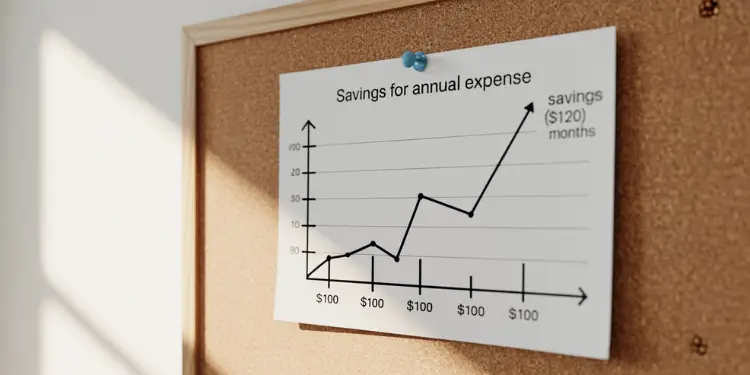

Use Sinking Funds to Handle Lumpy Annual Obligations with Ease

Managing your budget can be tough. Big expenses like insurance, property taxes, and holiday gifts can mess up your plans. But, using a budgeting tool called a sinking fund can help. It makes these big costs easier to handle.

A sinking fund is when you save a little bit each month for a big expense later. This way, you can handle the cost better. Many budgeting apps and online and mobile banking make it easy to set up these savings.

The sinking fund method can be complex and is often undesirable when interest rates are unpredictable Ref.: “Anderson, M. (2022). Sinking Fund Method: Definition, How It Works, and Advantages. Investopedia.” [!]

Think about what big costs you have each year. This could be:

- Annual insurance premiums

- Property taxes

- Holiday and birthday gifts

- Vacations

- Vehicle maintenance and registration

- Home repairs and appliance replacement

To figure out how much to save each month, use this formula:

| Total Needed | ÷ | Number of Months Until Due | = | Monthly Contribution |

|---|---|---|---|---|

| $1,200 | ÷ | 12 | = | $100 |

By saving for these costs ahead of time, you won’t stress about finding money when bills come. This way, you also don’t have to use your emergency fund or get into debt.

Adding sinking funds to your budget is a smart move. It helps you stay financially stable and plan for the future. By saving a little each month, you can handle big expenses without worry.

Align Category Names with Personal Language to Boost Emotional Connection

When saving for the future, make your budget categories personal. Use names like “Dream Home Down Payment” or “Olivia’s College Fund.” These names are more meaningful and motivating.

Linking budget categories to personal values reduces financial anxiety and improves adherence Ref.: “The Guardian. (2024). Anxious about money? Five financial therapists share their advice. The Guardian.” [!]

To make your budget personal, start by making a list of what’s important to you. Think about things like car tag renewals and types of insurance. Also, think about your long-term goals, like saving or investing for retirement. Then, give each category a name that shows your goals and values.

Here are some examples of personalized budget category names:

| Generic Category | Personalized Category |

|---|---|

| Savings | Family Vacation to Hawaii |

| Retirement | Beachfront Condo at 65 |

| Education | Liam’s Engineering Degree |

| Car Expenses | Reliable Ride for Work |

By making your budget categories personal, you connect more with your financial plan. Every time you check your bank statements or plan your spending, you remember why you’re doing it. This personal touch helps you stay on track with your budget.

When you decide how much money to put in each category, think about what’s most important to you. Consult a professional if you need help figuring out how to manage your money. With personal budget categories, you’re on your way to a secure financial future.

Read More:

Rebalance Categories Monthly Based on Actual Versus Planned Spending

To keep your budget on track, it’s key to check and tweak your budget categories often. This makes sure every single dollar is used well and meets your money goals. By looking at how much you spend versus what you planned, you can spot where you spend too much or too little.

It’s wise to update your budget every month. This keeps you in control of your money and lets you make quick changes when needed. When you look at your spending categories, watch for any patterns. For instance, if you always have extra in your food budget, think about moving that money to more important areas like debt or savings.

Conducting monthly budget reviews is recognized as a best practice for achieving financial goals and improving financial management Ref.: “M1 Finance LLC. (2025). Monthly Budget Reviews for Improved Financial Management. M1 Finance.” [!]

Shift Dollars from Surplus Lines to Underfunded Priorities

If some budget lines always have extra cash, it’s a chance to improve your financial plan. Instead of letting that money just sit there, move it to areas that need more money. This smart move helps you use your income better and keeps your budget running smoothly.

But, be careful when you change your numbers. If some categories always go over budget, look at why. See if you can spend less in those areas before just raising the budget. This way, you avoid spending too much and stay on track with your money goals.

Your budget should grow with you. Any big changes in income or monthly bills mean it’s time to update your budget. By staying active and regularly adjusting your budget categories, you’ll always know where your money is going and make smart choices about spending.

Incorporate Fun Money Line to Prevent Morale Crashes

When you make your list of budget categories, add a line for fun. This “fun money” lets you enjoy treats without hurting your big money goals. Personal finance advice often misses this, but it’s key to keep you going.

Decide how much fun money you want by taking 2-5% of your pay. You can change this if you’re paying off debt or saving. This way, you won’t feel left out or want to spend too much elsewhere.

Experts recommend allocating 5–10% of monthly income for fun money to maintain morale without derailing financial goals Ref.: “WaterStone Bank. (2019). Why You Should Set Aside \”Fun Money\”. WaterStone Bank.” [!]

Good personal finance is about managing money well and enjoying life. With a budgeting method like zero-based budgeting and fun money, you’ll track spending better. You’ll also reach your money goals with a happy heart. This small part of your budget can really help you succeed.

{kind=link}