Only 42% of Americans actively track their spending, leaving the majority uncertain about their financial outflows. They check their bank accounts often. But, I was one of them, watching my paycheck disappear without savings.

I adopted a straightforward daily spending system that transformed my financial habits. It’s not hard. It’s about giving each dollar a job. Some dollars cover bills, others bolster emergency savings, and some are allocated for discretionary spending.

Tracking your money daily is key. It helps you see where it goes and make changes early. This approach is effective regardless of income level, focusing on intentional money management. It’s about using your money wisely, not just having more.

Daily expense tracking enhances financial awareness, enabling individuals to identify spending patterns and make informed adjustments promptly. This practice supports more effective budgeting and financial goal attainment. Ref.: “Tamplin, T. (2025). The Benefits Of Expense Tracking And How You Can Do It Effectively. Forbes.” [!]

When you tell your money where to go, you control your future. Start by planning what to do with every dollar that comes in.

- A daily spending system helps you track money in real-time, not just at month-end

- Assigning specific jobs to your dollars creates financial clarity and reduces stress

- This method works for any income level and adapts to your personal financial goals

- Taking control of your money today leads to greater financial freedom tomorrow

Determine Your Reliable Monthly Take-Home Income Before Allocating Funds

The first step in mastering your money is figuring out your reliable monthly income. This is the steady cash flow that is the base of your budget. Without it, even the most detailed zero-based budget will fail under real-world pressure. I learned this the hard way after planning a month’s budget around a tax refund that never came.

Relying on irregular income sources, such as bonuses or tax refunds, can lead to budget shortfalls. It’s advisable to base budgets on consistent income to ensure financial stability. Ref.: “Investopedia. (2024). Zero-Based Budgeting: Benefits and Drawbacks.” [!]

Start by reviewing your last three months of pay stubs or bank statements to identify consistent income. Your goal is to find the money you can always count on every month. For most, this is your after-tax income—the cash that actually goes into your bank after taxes are taken out.

If you have automatic deductions for things like retirement accounts or health insurance, you have to decide what to do. Some say to add these back in to see your full savings and expenses. I prefer to keep it simple—just focus on the cash that really goes into your account.

For side jobs or freelance work, deduct business expenses and estimated taxes to calculate reliable income. We’re looking for reliable income, not just occasional money.

Exclude Irregular Income Sources for a Conservative Budgeting Approach

The biggest budgeting mistake I see is counting on money that’s not sure to come. In zero-based budgeting, exclude the following irregular income sources:

- Tax refunds (they can change a lot from year to year)

- Birthday or holiday gifts

- Overtime pay that isn’t regular

- Bonuses that aren’t promised

- Side hustle income that changes

If you get paid bi-weekly, you’ll get 26 paychecks a year. This means two months will have three paychecks instead of two. Don’t base your regular monthly budget on these “extra” paychecks. Instead, see them as special windfalls that can help you reach your financial goals faster.

For those with income that changes a lot—like freelancers or seasonal workers—budgeting needs extra care. Look at your income from the past year and use your lowest month as your base. This creates a safety net that stops you from planning expenses based on money that might not come.

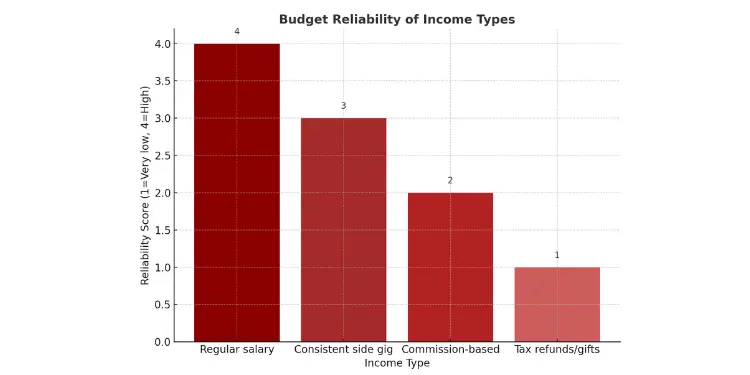

| Income Type | Budget Reliability | How to Handle | Example |

|---|---|---|---|

| Regular salary | High | Include full amount | $3,500 monthly after-tax paycheck |

| Consistent side gig | Medium | Include conservative estimate | $400 monthly from weekend delivery work |

| Commission-based | Low | Use lowest month as baseline | $2,200 (lowest) to $5,800 (highest) monthly |

| Tax refunds/gifts | Very low | Exclude from regular budget | $1,200 annual tax refund (treat as bonus) |

This careful way of figuring out your income might seem strict at first. You might think, “Why can’t I include that tax refund or birthday check?” The reason is simple: your monthly budget needs to be reliable above all else.

When you base your zero-based budget on your minimum reliable income, you create a system that works month to month without constant changes. Any extra money is a nice surprise that helps you reach your financial goals faster, not something you count on that might not come.

Once you’ve figured out your reliable monthly income, write it down. This is the base of your entire budget—every dollar you allocate comes from this amount. With this number in hand, you’re ready to move on to the next step: dividing your money into categories that make sure every dollar has a job.

Implement the Four-Bucket Allocation Framework for Efficient Budgeting

When I had trouble with budgeting, the four-bucket method changed everything. I’ve tracked our money for over 10 years. Most budgeting systems fail because they’re too hard.

People get tired of choosing where each dollar goes. The four-bucket system makes it easier. It organizes your spending into four simple categories.

“read more: Zero budgeting vs spending plan which plan suits“

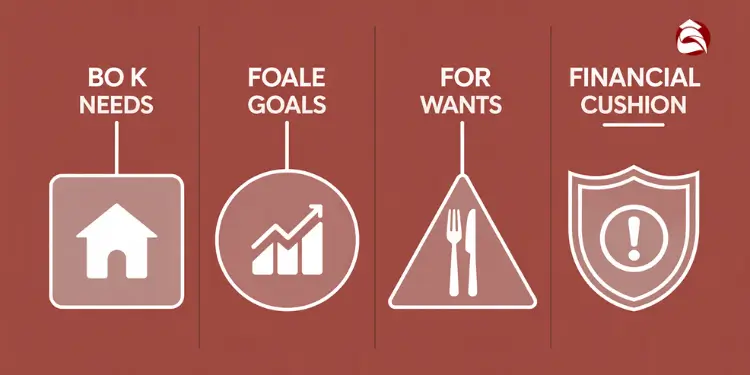

Categorize Expenses into Needs, Goals, Wants, and Cushion Buckets

First, fill your NEEDS bucket. This includes your “four walls” – the basics:

- Housing: Rent or mortgage, property taxes, insurance

- Utilities: Electricity, water, gas, internet, phone

- Food: Groceries and basic supplies

- Transportation: Car payment, insurance, gas, maintenance, or public transit

These costs usually take 50-60% of your income. By paying these first, you cover your basic needs.

Next, put money toward your current goals in the GOALS bucket. This includes:

- Debt payments beyond minimums

- Emergency fund contributions

- Retirement savings

- College funds

- Down payment for a home

Try to put 15-20% of your income here. Even 5% is better than nothing if you’re starting out. You can increase it as you can.

Allocate funds for discretionary spending in your WANTS bucket, including:

- Dining out and coffee shops

- Entertainment and streaming services

- Shopping for non-essentials

- Hobbies and recreation

- Gifts and celebrations

Be smart but fun with this category, which should take 15-20% of your income. If you need to save, cut here first.

Finally, establish a CUSHION bucket, allocating 5-10% of your income for unexpected expenses. It’s not for emergencies (that’s in your GOALS bucket). It’s for unexpected costs:

- Car repairs

- Medical co-pays

- Surprise school fees

- Appliance replacements

- Seasonal expenses

This system is flexible. You can adjust your spending between buckets as needed. If your income changes, you can move money around without starting over.

This method works with paper, spreadsheets, or apps. The tool doesn’t matter as much as following the four-bucket principle. Start with a good guess based on your income, then adjust as you spend.

Many families have found financial peace with this simple system. When every dollar has a purpose, you’ll know exactly where it goes. Making financial choices becomes much easier.

“A budget is telling your money where to go instead of wondering where it went.” – Dave Ramsey

The four-bucket budgeting method simplifies financial management by categorizing expenses into essential needs, financial goals, discretionary wants, and a cushion for unexpected costs. This approach aids in maintaining a balanced and adaptable budget. Ref.: “Kiplinger. (2023). Bucket Budgeting: An Easy Way to Manage Cash Flow.” [!]

Automate Transfers and Bill Payments to Maintain Budget Allocations

Setting your finances on autopilot makes sure you reach your goals. I used to miss savings goals and bill deadlines. But then I found out how powerful automation is.

Automation is like a financial bodyguard. It makes sure your money goes where it should before you can spend it. This way, you learn to live on what’s left after savings are taken out.

To automate your savings, link your budget to your accounts. This lets your finances work for you while you live your life.

Automating savings and bill payments ensures timely transactions, reduces the risk of missed payments, and supports consistent financial growth. This strategy is widely recommended by financial experts for effective money management. Ref.: “Winchell House. (2025). The Benefits of Using Automatic Payments for Saving, Paying Off Debt, and Investing.” [!]

Utilize Employer Split Deposits or Bank-Scheduled Transfers Effectively

Using your employer’s payroll system is the easiest way to automate. Many companies can split your paycheck into different accounts. I have mine split into 60% for main checking, 30% for bills, and 10% for savings.

If your employer doesn’t offer split deposits, your bank might. Set up automatic transfers to move money to different accounts on payday. This is great for building an emergency fund.

For bills, use auto-pay but with a safety net. Schedule them 2-3 days after payday to avoid overdrafts. This keeps your money safe while paying bills on time.

For big expenses like car insurance or property taxes, use sinking funds. Save 1/12 of the annual cost each month. Most online banks let you have many savings accounts for this. It helps you save little by little instead of all at once.

“Automation is to your budget what cruise control is to your car—it keeps you on track with minimal effort.”

If your income is not steady, set reminders to transfer money manually. The goal is to be consistent, even if the amounts change. Having someone to hold you accountable can help a lot.

Remember, automation works best with a little extra money in your account. Keep at least $500 to avoid overdraft fees if a bill comes early.

By automating your budget, you make getting out of debt easier. The system does the hard work for you. This makes reaching financial success much more likely.

Maintain a Two-Minute Nightly Spending Log for Real-Time Financial Awareness

Tracking your money every night is the best budgeting tool. It’s not an app, but a simple habit. This habit gives you real-time insight into your spending.

Small purchases add up fast. That $4.75 coffee is $142.50 a month. We forget these small buys easily.

Logging your spending each night is easy. You don’t need fancy software. Just a simple routine to track your money.

Regularly logging daily expenses, even briefly, can significantly enhance financial awareness and control, leading to better spending habits and increased savings over time. Ref.: “Frugal Spartans. (2023). The Benefits of Daily Expense Tracking.” [!]

Keep Receipt Box And Update After Dinner Each Day

Make tracking easy by removing all obstacles. I use a small box for receipts. After dinner, I update my log in just two minutes.

I use a notebook with three columns. Others prefer apps for tracking. The key is to be consistent.

This habit helps you spot spending patterns quickly. You’ll avoid big problems later. One person saved $37 weekly by avoiding a convenience store.

“I was skeptical about tracking every penny—it seemed obsessive. But after just one week of the two-minute log, I found three subscription services I was paying for but never using. That’s $64 monthly back in my pocket!”

Tracking together helps couples. My wife and I review our logs on Sundays. It stops money fights.

This habit also finds hidden spending. One person saved $14 monthly by canceling a streaming service.

Even tracking 80% of your spending helps. Start tonight with what you have. A simple notepad is enough until you decide on better tools.

This habit saves an average of $320 monthly. Stick with it for 21 days. By day 10, you’ll feel more in control.

Staying on top of your spending is about making choices. Knowing where your money goes lets you make better decisions.

Conduct a Weekly Budget Review to Manage Financial Surprises

Successful budgeting isn’t about being perfect. It’s about adapting calmly each week. Life can throw financial surprises like needing school supplies or car repairs. These surprises happen to everyone, no matter how well you plan.

Instead of giving up when surprises come, have a 15-minute weekly review. I do mine every Sunday evening. This helps keep small changes from becoming big problems.

This weekly check-in is like car maintenance for your budget. It keeps your budget running smoothly. You don’t need to make it hard to manage your money.

“The difference between successful budgeters and those who give up isn’t having fewer unexpected expenses—it’s having a system to handle them.”

“read more: Zero budgeting vs cash stuffing helping you decide“

Move Dollars Between Variable Categories Not From Savings

When adjusting your budget, move money between categories, not from savings. If you’re spending too much on groceries, use money from entertainment instead. This keeps your budget on track while being realistic.

Your weekly review has four easy steps:

- Review: Check what you’ve spent in each category

- Identify: Find categories that need more money

- Reallocate: Decide where to take money from

- Transfer: Make the changes in your system

This keeps your budget flexible and reduces stress. You’re not failing at budgeting when expenses come up. You’re just making planned changes.

For couples, these sessions can turn budget talks into useful conversations. When you both see adjustments as normal, talking about money is less stressful.

Remember, your emergency fund is for big emergencies, not for regular budget overruns. By moving money between categories, you keep your safety net strong. This makes saving easier.

If tracking changes is hard, use a financial app. Tools like EveryDollar make budgeting easier. They help you assign a purpose to every dollar.

Some people like to have a miscellaneous category for unexpected expenses. This gives you flexibility without ruining your budget. Just don’t make it too big.

The weekly adjustment habit helps you stick with budgeting long-term. It shows that budgeting is an ongoing process. With this habit, you’ll be ready for any surprise and reach your financial goals.

Reward yourself by directing surplus to priority goal at month end

At month-end, you find a small surplus in your budget. Even $20-50 can make a big difference. Use it for your top financial goal instead of spending it randomly.

I paid off $32,000 in student loans using this method. Every month, I saved every extra dollar for my debt. The budget every dollar method helps you win small victories and use them wisely.

Read More:

Visible tracker shows shrinking debt or rising savings progress

Make a simple tracker for your main goal. Use a basic thermometer chart for your debt or savings. Color it in each month as you save more.

Put this tracker where you see it every day. It could be on your fridge, mirror, or phone. It helps you connect your daily choices to your big dreams.

When you hit milestones, like saving $1,000, treat yourself a little. Use some of your fun money to celebrate. This makes budgeting feel good.

The everydollar budget isn’t about saying no. It’s about helping you reach your most important goals. By giving every dollar a job and saving for what matters, you’ll change your financial future slowly but surely.

{kind=link}