Is it better to chase ten financial targets at once or focus on just one? I’ve helped hundreds of new investors set their first goals. Most think more targets mean faster progress.

A Vanguard study found that beginners with 2-4 specific goals are 68% more likely to stay on track. This focus is key for success.

“Setting limits isn’t about restricting growth,” says Charlie Munger. “It’s about focusing for growth.” This advice has guided my clients in Phoenix for over a decade.

Starting your investing journey doesn’t need to be complicated. What’s important is finding the right balance for you, not following someone else’s plan.

In this guide, I’ll show you how to pick the right number of financial goals. We’ll focus on what you can realistically achieve, not ideal scenarios.

Key Takeaways:

- Quality trumps quantity when establishing your first set of financial targets

- Most beginners benefit from focusing on 2-4 well-defined objectives

- Your personal circumstances should determine your approach, not generic advice

- Effective planning requires clarity about both short and long-term priorities

Factors determining optimal goal count

The right number of investment goals for you depends on several personal factors. I’ve helped many investors figure out how many goals they can handle. Your financial situation, life stage, and how much risk you’re willing to take all play a role.

Think of your investment goals like spinning plates. Each plate needs your attention and resources. The right number keeps you focused without feeling overwhelmed. Let’s look at the key factors that guide your decision.

Assessing Income and Expense Stability

Your income pattern is the base for all your investment activities. Those with steady income can handle more goals than those with variable earnings.

Government employees and tenured professionals often manage 4-5 goals at once. Their steady paychecks help. Freelancers and those with variable income should aim for 2-3 goals to match their cash flow.

Start by looking at your income over the last 24 months. A steady income means you can handle more goals. But if your income is unpredictable, fewer goals are better.

Stable expenses are just as important as stable income. Compare your fixed monthly costs to your income. A big surplus means you can tackle more goals. A small surplus means focus on fewer, more important goals.

FINRA recommends building a liquid emergency reserve covering 3–6 months of expenses *before* tackling multiple investment goals, so unexpected cash needs don’t force premature asset sales that derail your plan. Ref.: “FINRA Investor Education Center. (2025). Start an Emergency Fund. FINRA.” [!]

The stability of your income and expenses creates the foundation for all your financial decisions. Without this foundation, even the most promising investment strategy will eventually crumble.

Evaluating Risk Tolerance and Age

Your comfort with financial risk limits how many goals you can pursue. Conservative investors should aim for fewer, more certain goals. This avoids spreading risk too thin.

Age affects both your goal count and what goals to prioritize. Young investors (under 40) focus on fewer, long-term goals. This allows for compound growth and handling market ups and downs.

As you get closer to 45, you balance growth with preservation. This age supports 3-4 goals with different time frames. By 65, you may need to manage several immediate goals, like income and healthcare planning.

Your current life situation also matters. Major life changes, like career shifts or family growth, mean fewer goals until things settle. Each change can change your financial priorities and capacity.

| Factor | Fewer Goals (1-2) | Moderate Goals (3-4) | More Goals (5+) |

|---|---|---|---|

| Income Stability | Variable/commission-based income, frequent gaps | Mostly stable with occasional fluctuations | Highly predictable income (government, tenured positions) |

| Expense Stability | Unpredictable expenses, tight margin | Mostly fixed expenses with adequate surplus | Very predictable expenses with wide surplus margin |

| Risk Tolerance | Conservative, discomfort with uncertainty | Moderate comfort with calculated risks | High tolerance for volatility across multiple fronts |

| Age/Life Stage | Very young (70) | Mid-career (35-55) with established foundation | Pre-retirement (55-65) with complex planning needs |

| Life Situation | Major transitions pending (career change, relocation) | Relatively stable life circumstances | Highly stable personal and professional situation |

Managing multiple financial goals isn’t just about money. It’s also about your mental capacity. Each goal needs regular checks, adjustments, and emotional strength during market changes. Be honest about how much complexity you can handle.

Your goal count will likely change as your financial situation and risk tolerance evolve. The goal is to find a balance between focus and diversification for your current situation. Stay flexible to adjust as your life changes.

“read more: How to Adjust Investment Goals Over Time“

Balancing short medium long term goals

Creating harmony between your short, medium, and long-term financial goals is key to effective investing. After guiding investors for 12 years, I’ve seen two common mistakes. Some focus too much on long-term goals and ignore immediate needs. Others only worry about short-term needs and forget about long-term investing.

The best investment portfolios mix different timeframes. I suggest the “1-2-1 framework” for beginners: one short-term goal, two medium-term goals, and one long-term goal. This balance helps create liquidity layers in your finances.

Vanguard’s Life-Cycle Investing Model shows that matching each goal with its own risk-appropriate asset mix materially improves the probability of success by adjusting exposure as deadlines approach—validating the 1-2-1 framework’s goals-based structure. Ref.: “Aliaga-Díaz, R., Ahluwalia, H., Zhu, V., Donaldson, S., Daga, A., & Pakula, D. (2021). Vanguard’s Life-Cycle Investing Model (VLCM): A General Portfolio Framework for Goals-Based Investing. Vanguard.” [!]

The Short-Term Foundation

Your short-term goal should be achievable in 1-3 years and focus on immediate financial security. The most important short-term goal is building an emergency fund for 3-6 months of expenses. This fund protects your other goals from unexpected costs.

“An emergency fund isn’t just another savings account—it’s insurance for your other financial goals.”

Without this foundation, you risk derailing your investment strategy at the first financial hiccup. I’ve seen investors forced to sell long-term investments at bad times because they lacked this basic protection.

The Medium-Term Bridge

Medium-term goals (3-10 years) are milestones that keep you motivated. Examples include saving for a home or a college fund. These goals bridge the gap between immediate needs and long-term dreams.

I recommend two medium-term goals that match your priorities. For many, saving for a house is the main goal. This goal has a clear timeline and target, making it easier to plan.

Your second medium-term goal might be for a major life event or education. The key is to choose goals with clear timelines, not vague dreams.

The Long-Term Vision

Your long-term goal (10+ years) gets the biggest growth potential and the largest investment over time. For most, retirement savings is the main long-term goal.

The power of a long-term goal lies in its growth potential. Investing early in retirement can lead to much more wealth than investing later. This makes your long-term goal very sensitive to early contributions.

| Time Horizon | Typical Goals | Recommended Count | Primary Purpose |

|---|---|---|---|

| Short-term (1-3 years) | Emergency fund, vacation | 1 | Financial security |

| Medium-term (3-10 years) | Home down payment, college savings | 2 | Life milestone achievement |

| Long-term (10+ years) | Retirement, legacy planning | 1 | Wealth accumulation |

Why This Balance Works

The 1-2-1 framework avoids two common mistakes. It prevents focusing only on distant goals and neglecting immediate needs. It also stops the mistake of only addressing short-term needs and ignoring long-term investing.

When picking goals, choose those with clear deadlines. For example, saving for college by age 18 is better than just building wealth. The more specific the goal, the easier it is to plan.

Remember, the number of goals should match your ability to fund them well. Four well-funded goals are better than eight poorly funded ones. Quality is more important than quantity when setting goals.

“The best investment strategy isn’t the one with the most goals—it’s the one with the right goals in the right proportions.”

This balanced approach ensures financial security across different time frames. Your short-term goal offers immediate protection. Your medium-term goals provide motivating milestones. And your long-term goal benefits from compound growth.

Prioritizing goals using ranking framework

When you have many financial goals, a ranking system is key. After 12 years of helping investors, I’ve seen beginners struggle. They often can’t decide which goals to focus on first.

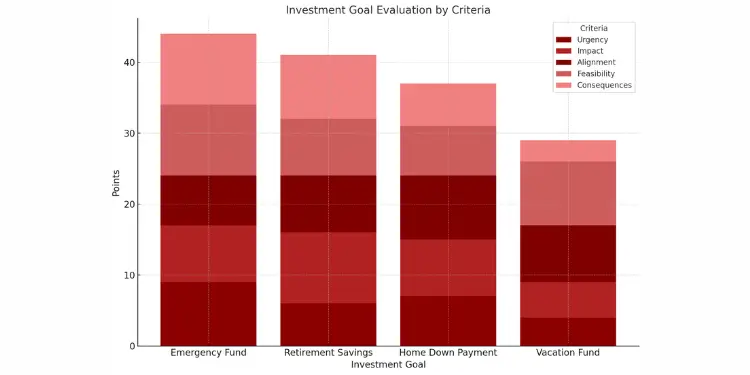

I’ve created a simple 10-point ranking system for new investors. It makes choosing goals clear and ensures your money goes to the most important ones.

Here’s how it works: For each goal, give it 1-10 points in five areas:

- Urgency: How urgent is this goal?

- Impact: How big of a financial impact will it have?

- Alignment: Does it match your values?

- Feasibility: Is it likely you can achieve it?

- Consequences: What happens if you miss this goal?

STATISTICAL EVIDENCE:

Investopedia’s analysis of the 50/30/20 budgeting rule confirms that earmarking a fixed 20 % of income for savings offers a clear, measurable pathway to finance both short- and long-term objectives without starving essential spending. Ref.: “Whiteside, E. (2024). The 50/30/20 Budget Rule Explained With Examples. Investopedia.” [!]

This method helps you see each goal from different angles. I’ve seen investors choose vacation homes over saving for emergencies because they’re more exciting. This system stops such mistakes.

Your first goals should focus on financial security. Only after that can you aim for lifestyle goals. If two goals are tied, choose the one with the sooner deadline or smallest cost.

| Investment Goal | Urgency (1-10) | Impact (1-10) | Alignment (1-10) | Feasibility (1-10) | Consequences (1-10) | Total Score |

|---|---|---|---|---|---|---|

| Emergency Fund | 9 | 8 | 7 | 10 | 10 | 44 |

| Retirement Savings | 6 | 10 | 8 | 8 | 9 | 41 |

| Home Down Payment | 7 | 8 | 9 | 7 | 6 | 37 |

| Vacation Fund | 4 | 5 | 8 | 9 | 3 | 29 |

Applying SMART Criteria to Rankings

After ranking your goals, use SMART criteria to refine them. This turns vague wishes into clear plans.

SMART means Specific, Measurable, Achievable, Realistic, and Time-based. Goals that score well but don’t meet SMART criteria need work.

For example, “save for retirement” might be important but lacks specifics. Change it to “save $800,000 by age 67” and it becomes actionable. This clarity helps you track and adjust your progress.

“The most common mistake I see is when investors prioritize discretionary goals over foundational ones. Your emergency fund and retirement security should always come before that vacation home or luxury purchase.”

Let’s look at how SMART criteria apply to your goals:

- Specific: Be clear about what you want. “Build wealth” is vague; “save $50,000 for a down payment” is specific.

- Measurable: Have clear ways to track progress. “Grow my portfolio” lacks metrics; “increase portfolio value by 7% annually” sets a clear goal.

- Achievable: Set goals that challenge you but are possible. Consider your income, expenses, and knowledge.

- Realistic: Make sure your goal fits your risk tolerance and financial situation. A 20% annual return might be too high for a conservative investor.

- Time-based: Set a deadline that motivates you without causing stress.

Financial advisors say specific goals lead to better results. When you know what you’re aiming for, you can choose the right investments and track your progress.

Remember, prioritizing goals isn’t a one-time task. You should review your goals every quarter as your finances change. The ranking system is flexible but keeps you focused.

By using the 10-point ranking system and SMART criteria, you create a powerful tool for prioritizing. This ensures your limited resources go to the most important goals, helping you succeed in investing.

“read also: How to Determine Your Investment Goals Properly“

Allocating savings across multiple goals

Dividing your savings among different goals is key to success. First, decide how many goals you have and their order of importance. Then, split your money wisely. This step is crucial for making progress.

Start with a percentage-based system for allocating funds. This way, your savings grow with your income. When you earn more, you save more without changing your plan.

For those with 3-4 goals, here’s a good starting point:

- 50% to your highest priority goal

- 30% to your second priority goal

- 20% divided among remaining goals

This plan helps you make good progress on your top goals. For example, saving $500 a month can go to retirement, a house down payment, and an emergency fund. This balance helps you move forward in all areas.

When choosing between short and long-term goals, think about the “opportunity cost differential.” Saving for a short-term goal, like a house down payment, means missing out on growth in long-term investments, like retirement.

The longer you have until you want to meet your goal, the more you can pursue growth through your investment portfolio.

This doesn’t mean ignore short-term goals. But, it should guide your decisions. Many investors increase their long-term investment percentages to make up for lost growth.

For goals with deadlines, like college funding, calculate your monthly savings. Start with your goal amount, subtract what you already have, add a return rate, and divide by the months left.

| Goal Type | Time Horizon | Allocation Approach | Investment Vehicle | Review Frequency |

|---|---|---|---|---|

| Emergency Fund | Immediate | Fixed amount | Liquid investments | Quarterly |

| House Down Payment | 2-5 years | Target amount | High-yield savings | Semi-annually |

| College Fund | 5-18 years | Target with deadline | 529 Plan | Annually |

| Retirement | 20+ years | Percentage of income | 401(k)/IRA | Annually |

For retirement, save a percentage of your income. This method adapts to your finances and builds a lasting habit. Consistent contributions lead to better investment growth.

When you get unexpected money, like bonuses or gifts, put most of it toward your top goal. This approach can help you overcome challenges faster and simplify your finances.

Don’t spread your savings too thin across many goals. Saving $50 a month to eight goals seems like progress but slows down real results. Focus on a few key goals for better success.

Allocation is not just about money; it’s also about attention. Each goal needs monitoring, which costs time and effort. Start with fewer goals to manage better.

As your finances grow, so should your strategy. What works for $10,000 may not for $100,000. Aim for focus to see real progress while keeping a balanced approach.

“read more: Why People Fail to Reach Investment Goals“

Monitoring progress and reallocating funds

Successful investors closely monitor their progress and adjust their funds as needed. Even with the best plans, you need to check in regularly and make changes when necessary. Think of your investment plan as something that evolves, not a fixed plan.

Setting up a simple quarterly review system is a good idea. It should take less than 30 minutes, but it helps keep your investments on track. This way, you avoid checking your accounts too often or not often enough.

DALBAR’s 29-year QAIB study reveals that, over the past two decades, the average equity-fund investor earned roughly 4–5 % annually versus 9–10 % for the S&P 500—underscoring the cost of emotional timing errors when portfolios aren’t rebalanced systematically. Ref.: “DALBAR, Inc. (2023). Quantitative Analysis of Investor Behavior. DALBAR.” [!]

Setting Quarterly Progress Review Checkpoints

Make a one-page dashboard for each investment goal. Track three important metrics: target balance, planned contributions, and expected returns. This helps spot any issues early on.

Plan these reviews for the first weekend of January, April, July, and October. These dates match when most investment statements come out. It’s a good time to reflect on your progress.

| Review Element | Questions to Ask | Potential Action |

|---|---|---|

| Timeline Assessment | Has my timeline for this goal changed? | Adjust contribution rate or investment strategy |

| Target Evaluation | Has my target amount changed? | Recalculate required savings rate |

| Funding Capability | Has my ability to fund this goal changed? | Reprioritize goals or adjust timeline |

| Performance Review | Are my investments performing as expected? | Consider rebalancing or changing investment products |

During each review, ask these questions about each goal. If you answer “yes” to any, you need to update your contribution rates. Monitoring and rebalancing your investment portfolio keeps you on track, even when markets change.

Responding to Life Circumstance Changes

Life changes often mean you need to adjust your goals. Big events like job changes or marriages should prompt a review of your goals. Don’t stick to old plans just because it’s not review time.

Watch out for “goal creep,” adding new goals without removing old ones. This spreads your resources too thin. If a new priority comes up, be brave and adjust your goals accordingly.

When moving funds between goals, think about taxes and penalties. Sometimes, it’s better to change future contributions than to move money now. For example, adding to a savings account is easier than moving money from a retirement account.

“The most powerful reallocation strategy for beginners is what I call the ‘completion redirect’—when you fully fund one goal, immediately redirect its entire allocation to your next highest priority unfunded goal rather than spreading it across remaining objectives.”

This method helps you achieve goals faster. I’ve seen investors reach three goals quicker by focusing on one at a time.

Monitoring isn’t just about numbers; it’s about staying motivated. Celebrate your progress to keep yourself on track. A small reward for reaching certain milestones can really help.

For accounts like 401(k)s or IRAs, match your reviews with any changes in employer matching. This helps you make the most of “free money” while keeping up with your goals.

Use your reviews to see which strategies work best for you. The data will show you patterns in your saving and investing. This information can help you make better choices for all your financial goals.

Read More:

Checklist for deciding your goal count

After guiding hundreds of beginning investors, I’ve made the goal-setting process simple. This checklist helps you avoid the mistakes of having too few or too many goals:

✓ Assess your financial foundation – Make sure you have 3-6 months of savings and manageable debt before setting goals.

✓ Identify your time horizons – Sort your goals by when you need the money. Short-term is 0-2 years, medium-term is 3-7 years, and long-term is 8+ years.

✓ Apply the rule of three – Beginners usually do well with 1-2 short-term, 1-2 medium-term, and 1 long-term goal.

✓ Run a goal calculator – Use online tools to figure out how much you need to save each month for each goal.

✓ Check your capacity – Don’t invest more than 20-30% of your take-home pay each month.

✓ Set and prioritize – Use the SMART criteria to rank your goals.

✓ Create your game plan – Decide how much of your investment dollars to put into each goal.

✓ Schedule quarterly reviews – Set reminders to check your progress and make changes as needed.

This checklist is your first step to a solid investment plan. I’ve seen beginners succeed by focusing on 3-5 clear goals instead of trying to do everything at once. Start with this guide, learn to set meaningful goals, and adjust as your financial situation changes.

{kind=link}