Homeowners who spend too much on their homes are called house poor. They have little money left for other things. When buyers stretch their budgets too far, they face a financial squeeze.

In Greenville, I’ve seen many new homeowners become house poor. They pay off their mortgage, but then they’re left with almost no money. They can’t handle unexpected maintenance costs or hidden homeownership expenses.

“Owning a home should make your life better, not worse,” my mentor said. Yet, 37% of American homeowners with mortgages spend too much on housing.

Why do smart people become house broke? It’s because they forget about the total cost of owning a home.

Someone who’s cash poor might skip home repairs or delay saving for retirement. They might even use credit cards to keep up with their home. This turns their biggest asset into a financial burden.

Quick hits:

- Monthly housing costs should stay under 28%

- Emergency funds prevent repair-related financial strain

- Maintenance typically costs 1-2% annually

- Budget for all homeownership expenses upfront

- Consider total lifestyle costs before purchasing

Definition signs and financial danger zones

‘House poor’ means you spend too much on your home. This makes it hard to pay for other things you need. Owning a home is a dream for many. But, it can turn into stress if you can’t afford to pay for it.

Being house poor isn’t just about having a big house. It’s about not having enough money for other things. You might have a beautiful home but can’t afford to go on vacation or eat out.

The signs of being house poor come slowly. You might move money from savings to pay the mortgage. Or, you might stop saving for retirement or use credit cards for groceries. These signs mean you’re in trouble financially.

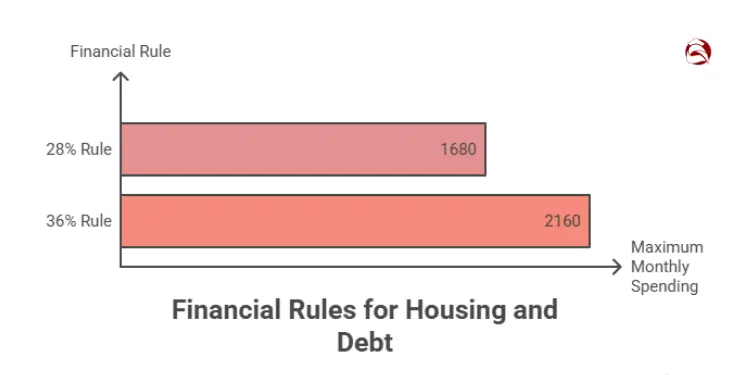

Experts have rules to help you avoid being house poor. The 28/36 rule is a good guide. It says your housing costs should be no more than 28% of your income. And, your total debt payments should be under 36%.

Percent Income Benchmarks for Housing Costs

Knowing the right percentages can help you stay safe from being house poor. The 28% rule includes your mortgage, taxes, insurance, and HOA fees. This is the most you should spend on housing before taxes.

For example, if you make $6,000 a month, your housing costs should be no more than $1,680. If you spend more, you’ll have less money for other things.

The 36% rule is about your total debt. It includes your mortgage, car loans, and credit cards. If you make $6,000 a month, your total debt payments should be under $2,160.

These rules are based on lots of financial data. They help avoid financial stress and the risk of default. The house price to income ratio is also important for knowing if housing is affordable in your area.

Watch for signs that you’re house poor:

- Putting off home repairs because they’re too expensive

- Feeling stressed when unexpected bills come

- Having no emergency fund or always using it up

- Working extra just to pay for your home

- Spending less on health care or food to afford your home

The biggest sign of being house poor is how it affects your future. If your home costs too much, you can’t save for retirement or invest. Your home then becomes a financial burden instead of an asset.

These rules might need to change based on where you live and your situation. In expensive places like San Francisco, spending more than 28% on housing is common. The important thing is to make sure you can afford other important things without stress.

Causes leading buyers into house poorness

Every house poor situation has a series of big mistakes. Buyers often don’t see these mistakes until it’s too late. I’ve helped many clients avoid financial trouble by understanding these common pitfalls.

Many buyers who bought a house they couldn’t afford didn’t see the trouble coming. They started with good plans but made big mistakes. Here are the most common mistakes I’ve seen in nine years of real estate.

Overestimating Appreciation and Lifestyle Inflation

Buyers often think their home will quickly increase in value. But counting on quick appreciation is very risky.

“I’ll grow into this payment” is a common mistake. It leads to spending more as income grows. This makes it hard to feel financially secure.

When buyers stretch their budgets, they often forget about other costs. I’ve seen clients struggle with the “cascade effect” of homeownership:

- Larger homes need more furniture

- Nicer neighborhoods make you want to keep up appearances

- Longer commutes cost more for transportation

- Upgraded homes lead to upgraded lifestyles

Being poor is having a mortgage that leaves no room for these lifestyle changes. Buyers often only think about the monthly payment, not the full financial picture.

Ignoring Emergency Fund and Maintenance Needs

Another big mistake is using up emergency savings for a down payment. I’ve helped many first-time buyers who spent their savings to buy a home.

The rich house poor situation often starts when buyers ignore maintenance costs. Homeownership means dealing with unexpected expenses that can hurt your budget.

One client had to replace their HVAC for $12,000 just eight months after buying. Without savings, they used high-interest credit cards, getting into debt.

Maintenance isn’t the only cost. Buyers often underestimate the total cost of homeownership. You can find a detailed cost breakdown of buying a house to see how these costs add up.

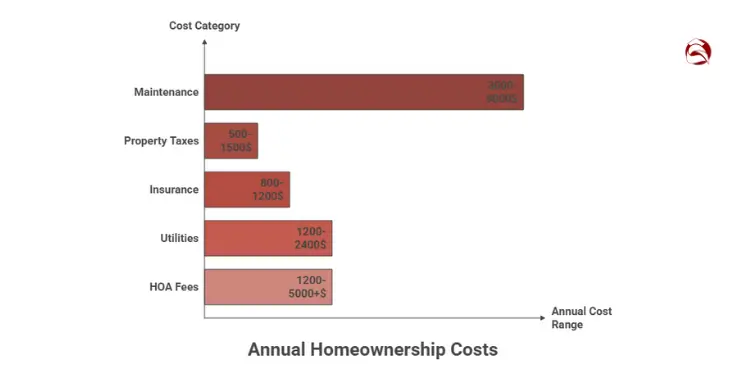

| Expense Category | What Buyers Expect | Actual Reality | Annual Impact |

|---|---|---|---|

| Maintenance | Occasional minor repairs | 1-3% of home value annually | $3,000-9,000 on $300K home |

| Property Taxes | Static amount | Increases with reassessments | $500-1,500 increase possible |

| Insurance | Similar to renter’s insurance | 2-3x higher plus rising premiums | $800-1,200 more than expected |

| Utilities | Similar to rental costs | 30-50% higher for larger spaces | $1,200-2,400 additional |

| HOA Fees | Minor monthly expense | Rising fees plus special assessments | $1,200-5,000+ unexpected costs |

Another pattern is buyers maxing out their mortgage approval. Remember, lenders use formulas, not your financial goals. Just because you qualify for a $400,000 mortgage doesn’t mean you should use it all.

The house poor house situation often comes from emotional buying. Buyers might spend more on features like granite countertops or backyard pools. I’ve seen clients add $50,000 for a kitchen upgrade that could have cost $15,000 later.

Many buyers also ignore life changes. Job loss, medical emergencies, or family additions can change your finances. Without savings, these changes can make a manageable mortgage overwhelming.

The poor house situation isn’t set in stone. By understanding these causes, you can avoid financial trouble. In the next section, we’ll look at the long-term effects of being house poor and how it affects more than just your bank account.

Impact of being house poor long term

Being house poor hurts your budget a lot. It changes your life in big ways. I’ve helped many people buy homes, and I’ve seen the bad effects of buying too big.

When your house costs too much, you have to cut back on things you need. You might not eat well because you can’t afford food. It’s like living in a nice house but feeling poor.

Homeowners might have a lot of money tied up in their house. But they don’t have cash for everyday things. This problem gets worse over time because of repairs and surprises.

Relationship Stress and Investment Opportunity Loss

Money problems can hurt your marriage a lot. I’ve seen couples who were happy to start with, but money fights soon followed. The stress of barely making ends meet can hurt even the strongest relationships.

When money is tight, couples often blame each other. One person said, “We used to dream about our future in this house. Now we just fight about how to pay for it.”

Being house poor can lead to a debt trap. When your house costs too much, you might use credit cards for other needs. This debt can grow fast and make your money problems worse.

Missing out on investments is another big problem. While others save for retirement, house-poor people struggle to stay afloat. This means losing a lot of money over time.

I’ve shown clients how much they could lose. A 35-year-old who can’t save $500 a month will have about $600,000 less at retirement. This is the real cost of being house poor.

Being house poor can also limit your career choices. You might not take risks or look for better jobs because you need every penny for your house. This can make you unhappy in your job.

For many, owning a home is a financial burden. It limits their ability to grow their wealth in other ways. The home that was meant to be an investment becomes a weight holding them back.

“The biggest mistake I see first-time buyers make is underestimating how being house poor will affect their quality of life. They focus on getting the house, not on what life will be like after they get it.”

Financial stress can also hurt your health. It can cause anxiety, sleep problems, and even depression. These health issues can make life harder and cost more money.

It’s important to think about these long-term effects before buying a house. A house should help your financial future, not hurt it.

“You Might Also Like: Common budgeting mistakes first time buyers make“

Calculating safe mortgage affordability ratios

Figuring out how much you can afford for a mortgage is more than just what banks say. It’s about what you can really handle. I’ve helped many first-time buyers for nine years. Too many have struggled because they only looked at what lenders said they could borrow.

One simple rule is to spend no more than 2.5 times your yearly income on a home. For someone making $80,000 a year, that’s a home price of $200,000. But this rule doesn’t consider all your financial details.

Front-End and Back-End Ratio Guidelines

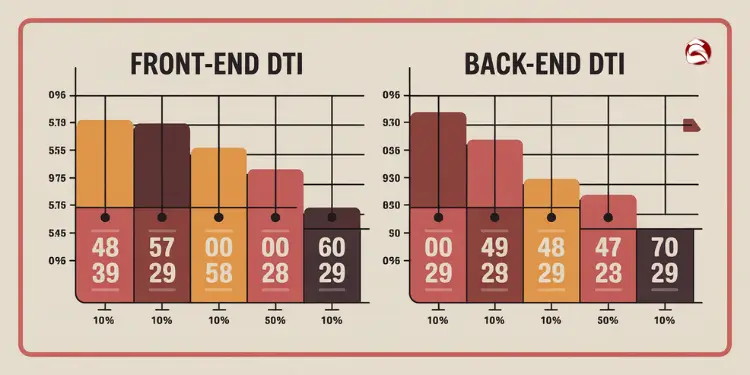

More detailed rules use debt-to-income (DTI) ratios to set safe spending limits. These ratios help keep you from spending too much on a home. Let’s look at both types:

| Ratio Type | What It Includes | Maximum Percentage | Example ($5,000 Monthly Income) |

|---|---|---|---|

| Front-End DTI | Housing costs only (mortgage, taxes, insurance, HOA) | 28% of gross monthly income | $1,400 maximum for housing |

| Back-End DTI | All debt payments (housing plus car loans, student loans, credit cards) | 36% of gross monthly income | $1,800 maximum for all debts |

| Conservative Approach | Housing costs for those with variable income or future plans | 20-25% of gross monthly income | $1,000-$1,250 for housing |

These percentages are based on solid research to keep homeowners safe. Spending more than 28% of your income on housing is risky.

To find your front-end ratio, multiply your monthly income by 0.28. For back-end ratio, multiply by 0.36. These numbers show how much you can spend on housing and total debt.

“Discover More: How to determine home buying budget for beginners“

Considering Variable Income and Future Goals

If your income changes a lot, you need a safer plan. Use your lowest income months for calculations, not your highest. This budget check before buying helps avoid money troubles.

Think about your future plans too. If you’re planning to:

- Start a family (which might lower your income or increase costs)

- Change careers or go back to school

- Retire early or work less

- Care for aging parents

It’s wise to aim for housing costs of 20-25% of your income. This gives you room for life’s surprises.

Online Calculators Accuracy Versus Individualized Professional Advice

Be careful with online mortgage calculators. They often give low estimates because they don’t include:

- Property taxes (usually 1-2% of the home’s value each year)

- Homeowners insurance (around $800-$1,500 a year for most homes)

- Private mortgage insurance (if you put down less than 20%)

- HOA fees (can be $100-$700 a month)

- Maintenance costs (about 1% of the home’s value each year)

I helped clients who thought they could afford a $350,000 home based on an online calculator. But after adding all costs and their future plans, they could only afford $275,000.

Online tools are a good start, but they can’t replace personalized advice. A real estate expert or financial advisor can tailor advice to fit your unique situation.

Lenders often approve you for more than you should spend. Their maximum amounts can be too high and lead to financial trouble. Stick to the safe ratios, even if you qualify for more, to keep your finances healthy.

“Further Reading: How to stick to home buying budget without fail“

Practical strategies to escape house poorness

Feeling the financial strain of homeownership? There are concrete steps you can take to escape being house poor. I’ve helped dozens of clients regain their financial footing. Several proven strategies can change your situation from house poor to financially stable.

Start with a detailed expense audit. Track every dollar for 30 days to see where your money goes. You’ll find non-essential spending to cut. Small changes in streaming services, dining out, and subscription boxes can save hundreds monthly.

For quick relief, consider mortgage recasting if you have a lump sum. Unlike refinancing, recasting keeps your loan but lowers payments. It costs $250-500 in fees, unlike thousands for refinancing.

If interest rates have dropped, look into refinancing. A 0.5% rate drop can lower your monthly payments. Make sure the closing costs are worth it for your situation.

House hacking is a powerful strategy. Renting out a spare room can cut your mortgage payment by 25-40%. One client turned their finances around by renting two rooms, covering 70% of their costs.

“I was drowning in mortgage payments until I rented out my basement apartment. That single decision changed everything—I went from barely making ends meet to building savings again.”

Property tax appeals can save a lot if your home is overvalued. Many homeowners don’t know they can challenge their assessment. A successful appeal can save thousands annually, lowering your monthly escrow payment.

For those with equity but cash flow issues, a Home Equity Line of Credit (HELOC) can help. Use it to consolidate debt, but never for vacations or luxuries when you’re house poor.

Increasing your income is another way to move forward. Look into side hustles, overtime, or asking for a raise. An extra $500 monthly can greatly improve your housing cost ratio and ease financial pressure.

When deciding between renovating or buying new, consider the financial impact. A fixer-upper vs. new construction choice should include ongoing maintenance costs. These costs can affect your house poor status.

As a last resort, downsizing to a more affordable home might be necessary. While moving has costs, the long-term relief can be worth it. I’ve guided many clients through this, and it often leads to financial freedom.

| Strategy | Potential Monthly Savings | Implementation Difficulty | Time to See Results |

|---|---|---|---|

| Expense Reduction | $200-500 | Low | Immediate |

| Refinancing | $100-400 | Medium | 1-2 months |

| House Hacking | $500-1,200 | Medium | 2-4 weeks |

| Property Tax Appeal | $50-200 | Medium | 3-6 months |

| Downsizing | $500-1,500+ | High | 3-6 months |

Escaping house poorness is not just about quick fixes. Each strategy should be part of a larger plan to improve your housing cost ratio. The goal is to not just survive but to build wealth again.

Building resilient budget for sustained future stability

Knowing what “house poor” means is just the start. You need to keep your finances strong for the long haul. Smart homeowners create plans to avoid being house poor.

“Read More: House poor meaning and how to avoid becoming it“

Building Sinking Fund for Unexpected Expenses

Make a special fund for home upkeep, apart from your emergency money. Aim to save 1-2% of your home’s value each year. For a $300,000 home, that’s $3,000 to $6,000.

Put this money into a savings account each month. Label it for home expenses. This way, you’re ready for any surprises.

Many people forget about upkeep costs when buying a home. They only think about mortgage payments. But, your home will need repairs someday.

“Related Articles:

Adjusting Budget Annually as Circumstances Change

Review your budget every January. Property taxes and insurance go up, and your home needs more maintenance as it gets older. Being unprepared can make you house poor.

Have a 10% buffer in your housing budget for these increases. If you have a variable-rate mortgage, test your budget with a 1-2% rate hike. Can you handle it? If not, think about switching to a fixed rate.

As your income grows, keep your housing costs the same. Don’t spend more on a bigger home. This way, your home becomes a solid financial base and a source of happiness.

{kind=link}