Buying a house can surprise even the most ready first-time buyer. The price of your dream home is just the start. The real cost of owning a home is often 25-40% more than you think.

“Most buyers only think about down payments and monthly payments,” I tell my clients. “They miss out on thousands of dollars in extra costs.” I’ve seen many Greenville families look surprised when they see the full financial picture.

The market needs more planning than ever. Homeownership costs have risen over 25% in recent years. Yet, wages haven’t kept up. Many buyers find out about these costs too late, as shown in comprehensive budget worksheets that follow real homebuying journeys.

I want to help you feel confident when you enter the market. This guide will cover all the costs you’ll face. From pre-purchase checks to yearly upkeep.

Quick Hits:

- Closing costs average 2-5% of price

- Inspections and appraisals cost $600-1000

- Maintenance requires 1-2% annually

- Moving expenses often exceed $1500

- Emergency funds prevent financial strain

Nationwide figures show that buyer closing costs usually equal 2 – 5 percent of a home’s price—meaning a €400 000 purchase often demands an extra €8 000 – €20 000 in cash at signing.Ref.: “Zillow Research. (2024). Closing Costs Explained: What Are Closing Costs and How Much Are They? Zillow.” [!]

Pre purchase fees before offer acceptance

When you’re buying your first home, remember the costs before you even make an offer. Many first-time buyers forget about these early costs. I’ve helped buyers in Greenville for nine years and seen them struggle with these fees.

These costs are between $1,150 to $2,100 and must be paid upfront. I suggest saving for these costs separately from your down payment. This way, you won’t be caught off guard.

Inspection, Appraisal, and Survey Fee Breakdown

A home inspection is key to avoiding hidden problems. You’ll pay between $300 and $600 for this service. The cost depends on the home’s size, age, and location.

I tell my clients to get a general inspection at least. For older homes or homes in certain areas, consider extra inspections. For example, radon testing costs $150, and termite inspection is $75-$150. These can save you thousands later.

| Pre-Purchase Fee | Typical Cost Range | When It’s Due | Who Typically Pays |

|---|---|---|---|

| Home Inspection | $300-$600 | At time of service | Buyer |

| Home Appraisal | $400-$700 | When ordered by lender | Buyer |

| Property Survey | $400-$800 | Before closing | Buyer (negotiable) |

| Specialized Inspections | $75-$300 | At time of service | Buyer |

Your lender will need a home appraisal before approving your loan. This ensures the property’s value matches your offer. You’ll pay $400 to $700 for this service.

IMPLEMENTATION CONSTRAINT:

Inspection fees are paid at the time of service and are non-refundable; buyers remain responsible even if the deal collapses, so keep €300 – €600 liquid beyond your earnest-money budget.Ref.: “Whytock, A. (2023). Who Pays for a Home Inspection? Real Estate Witch.” [!]

A property survey confirms the property’s boundaries. It’s important to avoid future disputes with neighbors. While sometimes negotiable, buyers usually pay for this service. Skipping this can lead to problems later.

Remember, these fees are due even if you don’t buy the property. If issues are found or the appraisal is low, you might not buy it. But you won’t get your money back. This is why it’s important to plan your budget carefully, whether you’re buying a fixer-upper or a new home.

When making an offer, include these costs in your total investment. Some buyers get seller credits or help with closing costs. But in competitive markets, this isn’t always possible. A good budget check before house hunting can save you from surprises.

Loan related charges at closing table

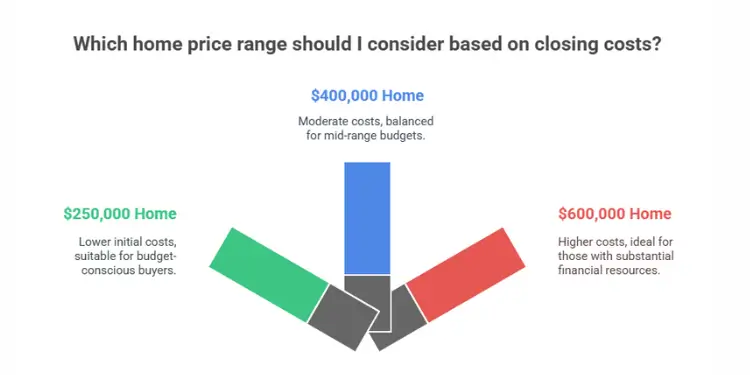

Understanding loan-related charges at the closing table can prevent surprises. After nine years helping first-time buyers in Greenville, I’ve seen many clients surprised by these costs. Closing costs are usually 2% to 5% of your home’s price. This means a $400,000 home could need an extra $8,000 to $20,000.

These costs include lender fees and third-party fees. Both affect how much cash you need to close. Many buyers forget about these extra costs, thinking only about their down payment.

Let’s look at what you’ll see on your closing disclosure. This way, you can budget well and avoid last-minute money troubles.

Origination, Discount, and Underwriting Explanations

Lender fees pay your mortgage lender for processing your loan. The biggest fee is usually the loan origination fee. It’s 0.5% to 1% of your loan amount. For a $300,000 mortgage, you might pay $1,500 to $3,000.

Discount points are optional fees to lower your interest rate. Each point costs 1% of your loan amount. For example, on a $300,000 mortgage, one point would be $3,000.

I suggest considering points only if you’ll stay in your home for 7 years or more. You can figure out if it’s worth it by dividing the cost of the points by your monthly savings. This helps balance upfront costs with long-term savings. You can learn more about this at balancing upfront costs versus long-term savings.

Underwriting fees cover checking your financial qualifications. They usually cost $300 to $900. This is when the lender checks your income, assets, and credit history.

Fannie Mae recommends requesting Loan Estimates from at least three lenders; comparison-shopping can shave hundreds off origination and third-party fees at closing.Ref.: “Fannie Mae. (2025). Closing Costs Calculator. Fannie Mae.” [!]

Other common lender charges include:

- Application fee: $300-$500

- Credit report fee: $25-$50

- Rate lock fee: $400-$800 (sometimes waived)

- Processing fee: $300-$900

Many of these fees change between lenders. I always tell my clients to ask for Loan Estimates from at least three lenders. Some lenders offer “no origination fee” loans but charge more in interest or other fees.

“read also: Affordable first home ideas for budget buyers“

Title Insurance, Escrow, and Recording Charges

There are also third-party charges you’ll see. Title insurance protects you and your lender from ownership disputes. Owner’s title insurance costs $500-$2,000, while lender’s title insurance is a bit less.

Escrow fees pay for the company that manages the transaction funds. These fees are usually $500-$800 and can be split between buyer and seller.

Recording charges cover filing your deed and mortgage documents. They cost $125-$250, depending on where you are. These fees make sure your ownership is legally recorded.

Other third-party fees include:

- Settlement fee: $400-$700

- Attorney fees (in some states): $500-$1,500

- Survey fee: $300-$800

- Transfer taxes: Varies widely by location

If your down payment is less than 20%, you’ll need to budget for private mortgage insurance (PMI). While not a closing cost, the initial setup might need an upfront premium at closing.

The table below shows typical closing costs for different home prices:

| Closing Cost Item | $250,000 Home | $400,000 Home | $600,000 Home | Typically Negotiable? |

|---|---|---|---|---|

| Loan Origination Fee (0.5-1%) | $1,125-$2,250 | $1,800-$3,600 | $2,700-$5,400 | Yes |

| Discount Points (optional) | $2,250 per point | $3,600 per point | $5,400 per point | Yes |

| Underwriting Fee | $300-$900 | $300-$900 | $300-$900 | Sometimes |

| Title Insurance | $500-$1,250 | $800-$2,000 | $1,200-$3,000 | No |

| Escrow/Settlement Fees | $500-$700 | $600-$800 | $700-$900 | No |

| Recording Charges | $125-$250 | $125-$250 | $125-$250 | No |

| Total Estimated Closing Costs | $5,000-$12,500 | $8,000-$20,000 | $12,000-$30,000 | Partially |

Many first-time buyers are surprised by these costs, even after being warned. I suggest saving an extra 1% of your purchase price for unexpected fees or last-minute changes.

Review your Closing Disclosure at least three days before closing. Compare it with your Loan Estimate and ask about any big differences. While some costs are fixed, others can be negotiated or shopped for better rates, saving you thousands.

Immediate move in repairs and upgrades

After you buy a new home, you’ll find repairs that need your attention and money. I’ve seen many first-time buyers worry about these costs. They often spend all their savings on buying the home, leaving little for repairs.

The state of your home when you buy it affects how much you’ll spend on repairs. Even if a home passes inspection, problems can show up when you start living there. It’s smart to save 1-3% of your home’s price for these costs.

Make two lists during your home inspection. One for safety repairs and another for cosmetic fixes. This helps you spend wisely and avoid surprises. Your inspector can tell you which repairs are urgent and which can wait.

Safety Compliance Repairs Before Move-In

Safety repairs are a must. They keep your family and home safe from dangers.

Electrical systems are often the biggest worry. Old panels, ungrounded outlets, or aluminum wiring need a pro to fix. This can cost $500-$2,500. Faulty wiring can start fires, so fixing it is very important.

High radon levels need a special system to fix. This gas can cause lung cancer. Fixing it costs $800-$1,500.

Old water heaters need to be replaced soon. A new one costs $900-$1,800. A broken water heater can damage your home, so fixing it is key.

Even if your HVAC system passed inspection, it might need cleaning or fixing. This can cost $300-$700. Dirty ducts or old filters can harm your air quality.

Look out for these safety issues too:

- Missing or broken smoke and carbon monoxide detectors ($20-$60 each)

- Unstable railings or damaged steps ($200-$1,000 to fix)

- Mold if there’s too much moisture ($500-$3,000 to fix)

- Lead paint in old homes ($800-$2,500 to remove)

- Roof damage that could leak ($500-$1,000 to fix)

After fixing safety issues, you can think about cosmetic upgrades. New carpeting costs $2-$5 per square foot. Painting a big house can cost $2,000-$4,000. These make your home nicer but can wait.

Get quotes from different contractors for big repairs. Prices and quality can vary a lot. Ask your real estate agent for trusted contractors who won’t charge too much.

Home maintenance is an ongoing cost. These first repairs are your first taste of what owning a home costs. Start a repair fund early to stay financially healthy.

The most expensive home repairs are the ones you postpone. Fix safety issues right away to avoid more costly problems later.

Ongoing maintenance and unexpected breakdowns

Buying a home is more than just a mortgage payment. You also face ongoing maintenance and unexpected repairs. A 2023 Thumbtack report shows homeowners spend about $500 monthly on upkeep. This means you’ll be fixing things yourself, unlike when you rent.

I tell my clients to plan for two types of maintenance. First, there’s regular upkeep. This includes things like HVAC checks, chimney cleaning, and pest control. These costs add up to $2,000-$3,500 a year for most homes.

Then, there are emergency repairs. These can be costly, like fixing a broken water heater. Costs can range from $1,000 to $3,000. Unexpected repairs often lead to the biggest bills.

| Maintenance Type | Frequency | Average Cost | Planning Strategy |

|---|---|---|---|

| HVAC Service | Twice yearly | $300-$600/year | Schedule in spring and fall |

| Gutter Cleaning | Twice yearly | $200-$500/year | Schedule before rainy seasons |

| Major Appliance Failure | Unpredictable | $500-$3,000 each | Emergency fund |

| Roof Repairs | As needed | $500-$5,000+ | Emergency fund or home warranty |

To handle these costs, keep a home emergency fund of $5,000-$10,000. This way, you won’t have to use high-interest credit cards for emergencies.

Some people also think about getting a home warranty. These plans cost $350-$600 a year plus service call fees. They can help with big repairs, which are common in older homes.

Consumer Reports advises self-insuring: redirect the €350 – €600 annual premium into a dedicated repair fund, which often yields better coverage and fewer claim denials than typical home-warranty contracts.Ref.: “Consumer Reports. (2025). Is Buying a Home Warranty Worth It? Consumer Reports.” [!]

Experts say to budget 1-4% of your home’s value for maintenance. For a $300,000 home, that’s $3,000-$12,000 a year. Keep track of these costs in your first year to know what your home needs.

- Fix small problems quickly to avoid big costs

- Learn to do simple repairs yourself

- Find reliable contractors before you need them

- Consider the age of your home’s systems when budgeting

- Find out how long your home’s parts last

Remember, fixing things now saves money later. A small leak can cause a lot of damage. By fixing problems fast and budgeting for both regular and emergency repairs, you protect your investment and avoid surprises.

Annual ownership expenses and tax duties

Buying a home means you have to pay for things every year. These costs are more than just mortgage payments. They are a big difference between renting and owning.

Property taxes help pay for schools, roads, and emergency services. The cost varies by place. For example, in Hawaii, it’s 0.25%, but in New Jersey, it’s 2.1%. For a $300,000 home, you could pay $750 to $6,300 a year.

Homeowners insurance is also a must. It costs about $1,400 to $1,800 a year for a $300,000 home. Your location and the age of your home affect the cost. If you put down less than 20%, you’ll also pay Private Mortgage Insurance.

Utility costs can surprise people who used to rent. You might pay $300 to $500 a month for things like electricity and water. These costs can go up in summer and winter.

Homeowners Association Dues and Assessments

If you live in a planned community or condo, you’ll pay HOA fees. These fees cover things like pool maintenance and building upkeep. Fees can be $200 to $600 a month for condos, and $30 to $100 for single-family homes.

What do these fees cover? Usually:

- Common area maintenance (lobbies, hallways, elevators)

- Exterior building maintenance and landscaping

- Amenities like pools, fitness centers, and security

- Some utilities (water/sewer in many condos)

- Master insurance policy for the building structure

But watch out for special assessments. These are one-time charges for big repairs. They can be thousands of dollars. Always check the association’s finances before buying.

Property Tax Escalation Forecasts Yearly

Property taxes often go up every year. They can increase by 1-3%. But there are times when they can go up more:

- Home purchase (many areas reassess at sale price)

- Major renovations or additions

- Local budget shortfalls requiring tax rate increases

- School funding initiatives or bond measures

INDUSTRY BENCHMARK DATA:

Effective property-tax rates vary ten-fold across the U.S.—from 0.26 % in Hawaii to 2.08 % in New Jersey—so relocating buyers must model annual tax drift before finalising their price ceiling.Ref.: “Tax Foundation. (2024). Property Taxes by State and County, 2024. Tax Foundation.” [!]

First-time buyers often see a big jump in property taxes after buying. The previous owner might have had special tax breaks. Always talk to the local tax assessor to figure out your first-year taxes.

Some states offer tax breaks for homeowners. These can include seniors, veterans, or low-income families. But you have to apply for them. Don’t miss the deadlines to save money.

For taxes, remember that mortgage interest and property taxes might be deductible. But the 2017 tax law changed this. Now, you can only deduct up to $10,000 for property taxes and homeowners insurance.

Make a spreadsheet to track your annual expenses. This helps avoid surprises and is good for taxes. Also, save 1-2% of your home’s value each year for repairs. This helps avoid financial stress when things break.

Read More:

Budget buffer strategies to avoid surprises

I’ve helped many first-time buyers. I’ve found five ways to avoid money surprises when owning a home.

First, use the 28/36 rule. Keep your mortgage under 28% of your monthly income. And, keep all debt under 36%. This rule helps you handle unexpected costs.

Second, save money in three places. Save $3,000-$5,000 for moving costs. Save 1-3% of your home’s value for yearly upkeep. And save another 1-2% for big repairs. The home’s price affects how much you need to save.

Third, add 15-20% to all cost estimates. Renovations often cost more than expected. This rule applies to all home improvements.

Fourth, wait 6-12 months before buying extra things. This lets you save money. It also helps you figure out what your home really needs.

Fifth, think about getting home warranties or HVAC service contracts. Some people use a home equity line of credit for emergencies. But, you need to have a lot of equity first.

Review your budget every quarter. Adjust your spending based on real costs. Closing costs vary by region, so plan carefully.

The aim is to own a home and stay financially healthy. Good budgeting turns nervous buyers into confident homeowners.

{kind=link}