Smart frugal home buying tips can save you thousands in today’s tough market. Start with a realistic budget to avoid heartbreak. Did you know nearly 40% of first-time buyers regret not knowing the hidden costs of buying a house?

“The choices you make before signing affect your money for the next decade,” says housing economist Janet Rivera. This advice is key for me, helping hundreds of clients find great deals.

Most buyers only think about down payments. But there are other big costs like inspection fees and closing costs. Your mortgage amount isn’t what you should spend. Keep payments under 28% of your income for room to breathe.

The best deals go to those who know the market and their limits. Being ready helps you grab perfect opportunities quickly.

Quick hits:

- Get pre-approved before house hunting

- Budget for 2-5% in closing costs

- Negotiate repairs after thorough inspection

- Consider homes needing cosmetic updates

- Reserve cash for post-purchase expenses

The Consumer Financial Protection Bureau estimates that typical closing costs range from 2 % – 5 % of the purchase price (exclusive of your down payment). Build this allowance into your budget to avoid last-minute cash shortfalls. Ref.: “Consumer Financial Protection Bureau. (2024). Figure Out How Much You Want to Spend. CFPB.” [!]

Hunt for undervalued properties creatively

Smart homebuyers look for value in places with little competition. They find great deals before making an offer. Most buyers fight over the same listings, but smart shoppers find hidden gems.

When I help first-time buyers find their first home, I tell them to look beyond usual listings. This takes patience and research, but it can save a lot of money. Knowing the costs of buying helps find savings.

Fixer-uppers can save money on the purchase price. They need extra money for repairs later, but the initial savings are worth it. Make sure to plan for repairs before making an offer.

“You Might Also Like: How to determine home buying budget for beginners“

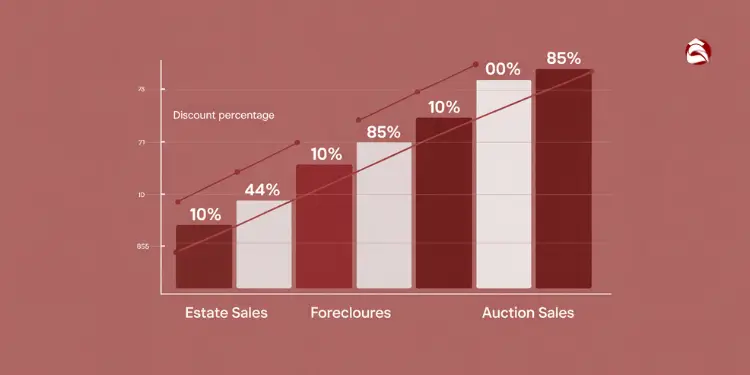

Track Estate Sales, Foreclosures, and Auction Listings

Estate sales are a treasure trove for budget buyers. They are priced 10-15% lower than market value. Set up alerts on your county’s probate court website to find these deals early.

Foreclosure auctions offer big discounts. Homes sell for 70-85% of market value. But, you need cash and do a thorough title search before bidding.

HUD foreclosure sales are strictly “all-cash, as-is” transactions, and the deed conveys **no warranties of title**. Thorough title searches and earmarked repair funds are essential before bidding. Ref.: “U.S. Department of Housing and Urban Development. (2016). Foreclosure Sale Invitation to Bid – Inverness Homes. HUD.” [!]

“I bought my first house at a foreclosure auction and saved nearly $45,000. It took more work, but the savings were worth it.”

Auction homes need repairs, but the discount helps with fixing them. Research the property well, including neighborhood and repair costs. Always check the property before bidding.

“Discover More: Ten smart ways to cut expenses to afford house faster“

Use Alert Tools for Price Drops

Technology helps spot price drops quickly. Set up alerts on Zillow and other sites for price drops over 3% in your area.

By being quick to respond to price drops, you can save thousands. Have your pre-approval ready and be ready to see the house fast.

Home prices change with market conditions and seller motivation. Homes listed for over 45 days might have motivated sellers. Your realtor can find these deals and help with offers.

When you find undervalued homes, you have more power in negotiations. The listing price is just a starting point. Bring comparable sales data to negotiate a better price.

Finding your first home on a budget means thinking outside the box. By exploring these paths, you can save thousands on your purchase.

Maximize savings on professional services costs

The 5-7% of your home purchase for professional services is a big chance to save. Most buyers just accept these fees without thinking, leaving thousands of dollars unclaimed. By negotiating and choosing service providers wisely, you can cut costs without losing quality.

In my nine years helping first-time buyers in Greenville, I’ve seen clients save an average of $3,800. This money can go toward your down payment, home improvements, or emergency fund.

“Further Reading: How to avoid overspending on house purchase budget“

Negotiate Agent Commissions Staging Allowances Aggressively

Begin by talking to several buyer’s agents and ask about their commission structure. Many will lower their commission by 0.5-1% if you find the property. This simple question can save you thousands.

When making offers, ask for a 3% seller contribution toward closing costs. This makes these costs part of your mortgage instead of out-of-pocket. Sellers often agree to this, even if the property has been listed for over 45 days.

Think about what you really need versus what you want when choosing services. Knowing this helps you budget better and avoid extra costs. Learn more about balancing needs versus wants in home buying to make smarter choices.

Don’t use the inspector your agent suggests. They might not find problems to keep the deal alive. Instead, find independent inspectors who know about your home’s age. They can find issues that others might miss.

Ask for radon, mold, and sewer scope inspections together for a discount. This can save $150-300 compared to getting them separately. These extra inspections can find costly problems that standard ones miss, saving you thousands.

Get quotes from at least five insurers for homeowners insurance. Use these quotes to get a better deal. One client saved $743 a year by bundling policies and raising their deductible. This lowers your monthly costs without increasing your risk too much.

Your credit scores affect your mortgage rate and insurance costs. Improving your score by 20 points can lower your rate by about 0.25%. This can save tens of thousands over your loan’s life. Check your credit reports for errors and pay down debt to boost your score.

| Professional Service | Standard Cost | Negotiation Strategy | Potential Savings | Success Rate |

|---|---|---|---|---|

| Agent Commission | 2.5-3% of purchase price | Self-property finding discount | $1,250-$3,000 on $250K home | 65% |

| Closing Costs | 2-5% of loan amount | Seller contribution request | $4,000-$10,000 on $200K loan | 70% |

| Home Inspection | $300-$500 | Bundle with specialty inspections | $150-$300 | 90% |

| Homeowners Insurance | $800-$1,500 annually | Multiple quotes and bundling | $200-$750 annually | 85% |

Negotiating might feel hard at first, but remember, everything is negotiable in real estate. Practice your negotiation script to feel more confident. A little discomfort can save you thousands.

When shopping around for services, be open about comparing options. Saying you’re getting quotes from others can create competition that helps you. This can lead to better deals.

Keep all quotes in writing and ask for fee breakdowns. Some providers add unnecessary extras. By asking to remove these, you can save money and cut costs without losing quality.

“Related Topics: House hacking first home guide for new buyers“

Leverage seasonal market timing advantages

Smart homebuyers know that the calendar date of your closing can dramatically impact what you’ll pay for your dream home. My data tracking shows January and February typically deliver 5-8% lower median sales prices than May through August in most U.S. markets. This isn’t just real estate folklore—it’s verified by National Association of Realtors seasonal price fluctuation data.

Winter buyers face significantly less competition at showings and open houses. With fewer buyers making offers, you’ll enjoy stronger negotiating leverage and encounter fewer stressful bidding wars that drive up purchase price. Sellers listing during colder months often have compelling reasons to move quickly, creating perfect conditions for reasonable offers with favorable terms.

One of my clients, a newly married couple, shifted their home search from June to January. They secured their target property for $17,500 less than an identical unit sold six months earlier. Even better, the motivated seller covered $5,000 in closing costs—money that went straight to reducing their monthly payments over the life of their loan.

| Season | Average Price Difference | Competition Level | Negotiation Power |

|---|---|---|---|

| Winter (Jan-Feb) | 5-8% below peak | Low | Strong |

| Spring (Mar-Apr) | 2-4% below peak | Moderate-High | Moderate |

| Summer (May-Aug) | Peak prices | Highest | Weakest |

| Fall (Sep-Dec) | 3-6% below peak | Moderate-Low | Moderate-Strong |

Redfin market data show the median U.S. sale price in January 2023 ($383,249) was 11.5 % lower than the May peak of $433,133, underscoring the financial edge of off-season purchasing. Ref.: “Redfin Data Center. (2023). U.S. Homeowners Have Lost $2.3 Trillion in Value Since June Peak. Redfin.” [!]

Beyond seasons, track interest rate announcements from the Federal Reserve. Rate increases often temporarily cool markets for 30-45 days afterward, creating brief windows where you’ll pay less for comparable properties. This directly affects how much you’ll pay each month for the entire mortgage term.

For maximum advantage, begin your serious search 60-90 days before your target season. This gives you time to understand what you need in a house versus the things you want, which helps prioritize spending. First-time buyers often tell me they wish they’d known this timing strategy earlier—it requires patience but delivers substantial returns.

Consider your long-term housing needs when timing your purchase. If you’re newly married or planning a family, you might want to pay attention to school districts and house price to income ratio in family-friendly neighborhoods. Buyers who need public transportation access should factor seasonal weather impacts into their timing strategy.

The price per square foot difference between peak and off-peak seasons can mean the difference between affording a three-bedroom home versus settling for two. When you pay interest on your mortgage for 15-30 years, even small purchase price reductions translate to thousands saved over the loan term.

- Research seasonal price trends in your specific target neighborhoods

- Set up alerts for Federal Reserve meetings and possible rate changes

- Schedule your pre-approval to align with your optimal buying window

- Prepare all documentation 90 days before your target buying season

- Practice patience—rushing costs money, while strategic timing saves it

Remember that what you want to pay and what sellers want to receive are naturally at odds. Seasonal timing gives you a built-in advantage that doesn’t require aggressive negotiation tactics—the market conditions do much of the work for you. This approach has helped dozens of my clients secure better deals while maintaining positive relationships with sellers.

Use energy efficiency to lower ownership expenses

Energy-efficient homes can save you money every month. They also increase your home’s value over time. Many buyers only look at the price of the home, not the monthly costs.

Think about all the costs of owning a home, not just the mortgage. Energy-efficient homes use less energy. This means you save money every month.

Before you buy, ask to see the seller’s utility bills. This can help you understand the costs. One buyer saved over $3,300 a year by choosing an energy-efficient home.

“Read More: Frugal home buying tips for budget conscious buyers“

Evaluate Insulation, HVAC, and Appliance Upgrades

Ask for a blower door test during inspections. This shows if your home leaks air. Homes that don’t leak air save a lot of energy.

When looking at homes, consider the HVAC system. A new, efficient system might cost more upfront. But it saves money over time.

Here are some easy ways to save money:

- Install programmable thermostats ($75-150) for 10-15% energy reduction

- Add water filters ($20-300) to eliminate bottled water expenses

- Replace standard bulbs with LED lighting to reduce electricity usage

- Install low-flow showerheads to decrease water heating costs

Replacing an old refrigerator with an ENERGY STAR-certified model saves about $150 in electricity over its 12-year lifespan while cutting energy use by 9 %. Multiply these gains across multiple appliances to compound monthly savings. Ref.: “U.S. EPA ENERGY STAR. (2025). Why ENERGY STAR Refrigerators? EPA.” [!]

Energy-efficient appliances also save money. New appliances use less energy. This means lower bills for you.

Think about whether to renovate or buy new. Older homes might need upgrades. But new homes often have the latest energy-saving features.

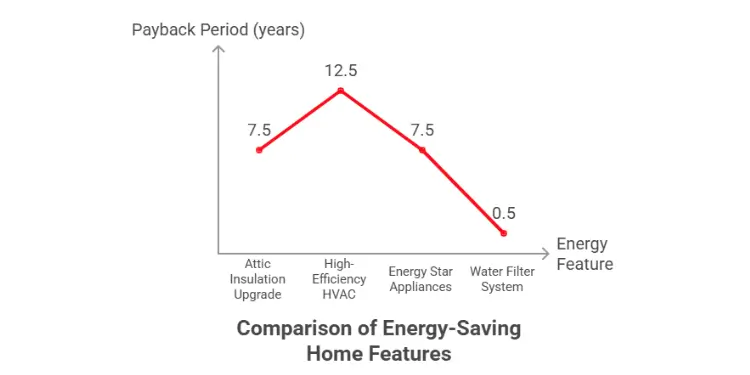

| Energy Feature | Typical Cost | Annual Savings | Payback Period |

|---|---|---|---|

| Attic Insulation Upgrade | $1,700-$2,100 | $200-$300 | 7-8 years |

| High-Efficiency HVAC | $4,500-$8,000 | $300-$500 | 9-16 years |

| Energy Star Appliances | $400-$1,500 extra | $80-$150 | 5-10 years |

| Water Filter System | $150-$300 | $240-$365 | Under 1 year |

Use online tutorials to check a home’s energy use before buying. This can help you find efficient homes faster.

Energy upgrades can also get you tax breaks or rebates. Ask your lender about special mortgages for energy-efficient homes. This can make your home more affordable.

“Check This Out: Affordable first home ideas for budget buyers“

Adopt disciplined spending during purchase process

When I tell clients we need a spending freeze after their offer is accepted, they often look surprised. Yet this 60-day financial pause is critical. Lenders track your credit activity until closing day. One client almost lost their single-family house when they financed new furniture just days before closing.

After you’ve bought our first house, make a list. Divide projects into three categories: immediate needs, 90-day improvements, and one-year goals. This prevents the common mistake that leads 44% of Americans to regret their home purchase – underestimating costs.

“Related Articles:

Tackle simple diy projects yourself. Painting, basic landscaping, and fixture replacements save 60-75% over contractor pricing. For my budget-conscious buyers, this approach stretches dollars significantly further than paying premium prices.

Your mortgage payment and hoa fees are just the beginning. Live frugally during the first six months of ownership by delaying non-essential purchases. One client saved over $4,200 by waiting to furnish guest rooms, finding quality items through estate sales instead.

Schedule your home inspection during mid-winter when contractor rates often drop. This simple hack ensures your emergency fund remains intact when inevitable repair surprises arise. Remember, homeownership can include fun things – just plan for them strategically.

{kind=link}