When a financial advisor helps with investment goals, they do more than just pick stocks or bonds. They act as your personal money guide. They turn complex market signals into simple steps that fit your life.

Ever wondered why some investors stay calm during market storms while others panic?

Studies show that investors with clear financial goals are 65% more likely to stay on track during market ups and downs. This steady approach often leads to success.

“The best advice isn’t about chasing returns—it’s about matching your money moves to your life goals,” a client once told me after our first meeting.

In my 12+ years helping Phoenix investors, I’ve seen how good advice turns vague dreams into real goals. The best partnerships are built on honest talks, not just promises of high returns.

Quick hits:

- Turn market noise into actionable steps

- Match investments to personal timelines

- Navigate volatility with confidence

- Transform confusion into clear direction

Vanguard’s Advisor’s Alpha framework shows that disciplined rebalancing, behavioral coaching, and tax-efficient implementation can add up to—or even exceed—3 percentage points in annual net returns for the typical client. Ref.: “Vanguard Investment Advisory Research Center. (2022). Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha. Vanguard.” [!]

Defining Advisor Roles And Fiduciary Responsibilities

How your financial advisor works with you depends on the law. It’s key to know this when picking someone for your money. Not all “financial advisors” work the same way or put your needs first.

Trust is key in your advisor relationship. But, this trust needs legal backing. Advisors are mainly fiduciary or follow the suitability standard. This choice affects your money and advice.

A fiduciary financial advisor must always put your needs first. They must tell you about any conflicts and choose the best for you. This is a big help, mainly for new investors.

Choosing a fiduciary advisor means you get someone who fights for your best interests. They pick the cheapest, best investments for you. This rule applies to all parts of your financial life.

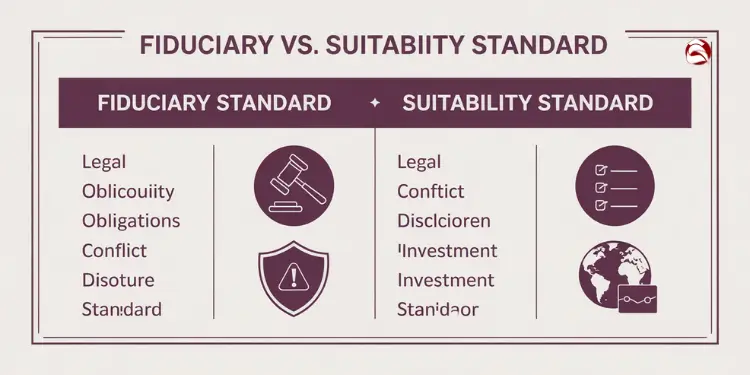

Comparing Fiduciary And Suitability Standards

Fiduciary and suitability standards are big differences. Knowing this helps you see who really cares about you in your financial talks.

| Aspect | Fiduciary Standard | Suitability Standard | Impact on Investor |

|---|---|---|---|

| Legal Obligation | Must put client’s interests first | Must recommend “suitable” investments | Potentially thousands in saved fees under fiduciary care |

| Conflict Disclosure | Required to disclose all conflicts | Limited disclosure requirements | Greater transparency with fiduciary advisors |

| Investment Selection | Best available option for client | Any suitable option, even if better alternatives exist | More optimal investment selections with fiduciaries |

| Typical Professionals | RIAs, CFPs operating as fiduciaries | Broker-dealers, insurance agents | Different service models and incentive structures |

Non-fiduciary advisors, like many stockbrokers and insurance agents, follow a less strict rule. They just need to make sure investments are “suitable” for you. This means they might suggest higher-fee products that pay them more, even if cheaper options are available.

Broker-dealers operating under the suitability rule need only ensure a recommendation is “suitable,” whereas Registered Investment Advisers must meet a fiduciary duty of care and loyalty that legally obliges them to place your best interests ahead of their own. Confirm which standard governs your advisor to avoid hidden conflicts and higher-cost products. Ref.: “Clayton, J. (2019). Regulation Best Interest and the Investment Adviser Fiduciary Duty: Two Strong Standards that Protect and Provide Choice for Main Street Investors. U.S. Securities and Exchange Commission.” [!]

The way your advisor gets paid can also affect their advice. There are four main ways advisors get paid:

- Fee-Only Advisors: Usually fiduciaries who charge a percentage of your assets, by the hour, or a flat fee.

- Fee-Based Advisors: Charge fees but might also earn commissions, leading to possible conflicts.

- Commission-Based Advisors: Make most of their money from selling products, which might lead to higher-commission choices.

- Hybrid Models: Mix different payment methods, with varying levels of transparency.

When looking for an advisor, ask about their fiduciary status and how they get paid. A good advisor will be open about this. Ask: “Are you legally obligated to act as a fiduciary 100% of the time?” and “How are you compensated for the products you recommend to me?”

Your advisor should clearly explain any possible conflicts and how they handle them. If they’re vague or hesitant, it’s a red flag. A good advisor is transparent about their duties and profits.

Before picking an advisor, check their background and any complaints through FINRA’s BrokerCheck and the SEC’s Investment Advisor Public Disclosure database. These tools show an advisor’s skills, past jobs, and any issues. This info is key before you let them plan your investment goal time horizon.

The choice between fiduciary and non-fiduciary advisors isn’t about their skill or honesty. It’s about their legal duties and how they make money. Many non-fiduciary advisors are honest and helpful. But knowing the difference helps you pick someone who meets your needs and follows the law.

Assessing Personal Goals Budget And Risk Profile

Before you invest, a financial advisor will help you set goals. They’ll look at your budget and risk level. This makes your dreams clear and specific.

They turn vague dreams into real plans. This is where a good investment goal starts to take shape.

In 12 years, I’ve seen many clients change. They go from vague dreams to clear plans. This is thanks to a detailed process that shows what’s truly important.

Using Goal Discovery Questionnaires Effectively

Goal discovery questionnaires are key. They do more than just ask for money info. They find out how you feel about money and your goals.

A certified financial planner doesn’t just ask what you want. They help you understand why. This is important when the market gets tough.

The most revealing question I ask clients isn’t about numbers at all. It’s: “What would you do differently if money were no object?” Their answer often unveils the true priorities that should drive their financial plan—whether that’s career flexibility, family legacy, or community impact.

Good questionnaires cover a few key areas:

- Time-based goals – When do you need the money and for how long?

- Priority ranking – Which goals take precedence if resources are limited?

- Risk capacity – How much volatility can your financial situation actually withstand?

- Risk willingness – How do market swings affect your emotional well-being?

- Past experiences – How have previous financial decisions shaped your current outlook?

Your answers help find your Risk Number®. This is a way to make sure your investments match your goals and comfort level.

Advisors look for any signs of unrealistic goals. For example, wanting low risk but high returns is a mismatch. They’ll talk and teach you about this.

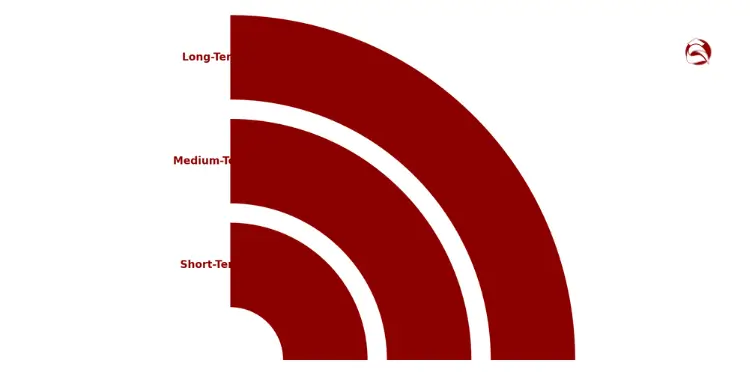

Mapping Budget Surplus Toward Investment Buckets

After setting goals, you need to figure out how much you can invest. It’s not just about how much you make. It’s about what’s left after you pay for basics and save for emergencies.

A good advisor will help you organize your money into different buckets. These buckets are based on how soon you need the money and what it’s for.

| Investment Bucket | Time Horizon | Typical Allocation | Risk Profile | Example Goals |

|---|---|---|---|---|

| Short-Term | 0-2 years | 10-30% of surplus | Very Conservative | Emergency fund, upcoming major purchase |

| Medium-Term | 3-7 years | 20-40% of surplus | Moderate | Home down payment, education funding |

| Long-Term | 8+ years | 30-60% of surplus | Growth-Oriented | Retirement, legacy planning |

| Opportunity | Varies | 5-15% of surplus | Speculative | Business ventures, higher-risk investments |

This bucket approach helps manage risk. Short-term needs are safe, while long-term goals can grow more.

As you get older, your allocations change. Young people focus on long-term goals. Those nearing retirement focus on short and medium-term goals to reduce risk.

To find your budget surplus, start with your after-tax income. Subtract essential expenses and emergency fund savings. What’s left is for investing.

Working with a financial advisor is key. They make sure you’re making smart choices. They turn small amounts into big steps toward your goals.

Next, calculate your budget surplus and decide which goals fit into each bucket. This will help you talk to your advisor about the right investment strategy for you.

Crafting Diversified Portfolios With Professional Tools

Building a portfolio is like a puzzle. It needs both smart math and personal touch. Financial advisors use top tools to help you.

For 12 years, I saw how trading tools got better. Now, they’re much more advanced than simple spreadsheets. Most people can’t use them.

At the core of good investment strategies is how things move together. When they don’t, it’s safer. This helps advisors keep your money safe during tough times.

Today’s advisors use special software. It looks at many asset combinations at once. It checks their past performance and how they move together.

Modern Portfolio Theory might sound hard. But it’s simple in practice. Advisors use it to make your portfolio safer. They explain it in a way you can understand.

Equity securities may fluctuate in response to news on companies, industries, market conditions and general economic environment. Bonds are subject to interest rate risk. When interest rates rise, bond prices fall; generally the longer a bond’s maturity, the more sensitive it is to this risk.

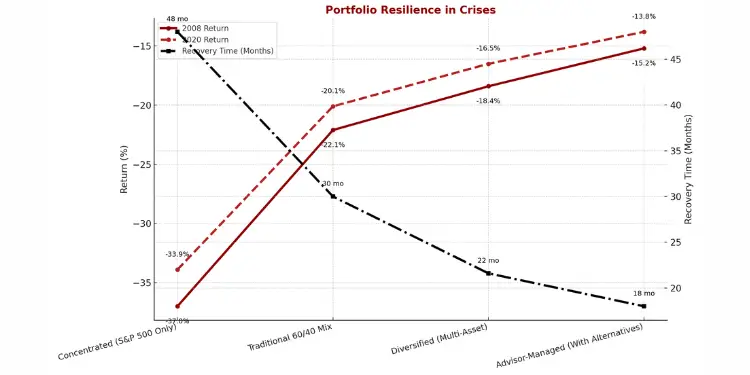

Diversification is key in bad times. In 2008 and 2020, diverse portfolios did better than ones with just a few stocks.

| Portfolio Type | 2008 Financial Crisis (Return) | 2020 Pandemic Drop (Return) | Recovery Time |

|---|---|---|---|

| Concentrated (S&P 500 Only) | -37.0% | -33.9% | 4+ years / 5 months |

| Traditional 60/40 Mix | -22.1% | -20.1% | 2.5 years / 4 months |

| Diversified (Multi-Asset) | -18.4% | -16.5% | 1.8 years / 3 months |

| Advisor-Managed (With Alternatives) | -15.2% | -13.8% | 1.5 years / 2 months |

Today, interest rates change a lot. Advisors adjust your portfolio for these changes. They move to safer bonds or stocks when rates go up.

Vanguard’s 2024 analysis underscores that globally diversified portfolios rebound faster and suffer smaller drawdowns than single-asset strategies—reinforcing diversification as a core, enduring best practice for risk control. Ref.: “Davis, G. (2024). Building Resilient Portfolios Through Diversification. Vanguard.” [!]

Managing your portfolio means keeping it balanced. Advisors sell stocks that do well and buy ones that don’t. This keeps your portfolio in check.

Advisors make a plan that changes with the market. They use tools to test your portfolio against different scenarios. This helps find and fix problems before they hurt you.

Many clients are surprised by what tools can find. They show how different investments can work together. This can help avoid big losses.

Remember, diversification doesn’t guarantee wins or protect against all losses. But it’s the best way to manage risk. A good tax advisor will also check your strategy to make sure it fits your needs.

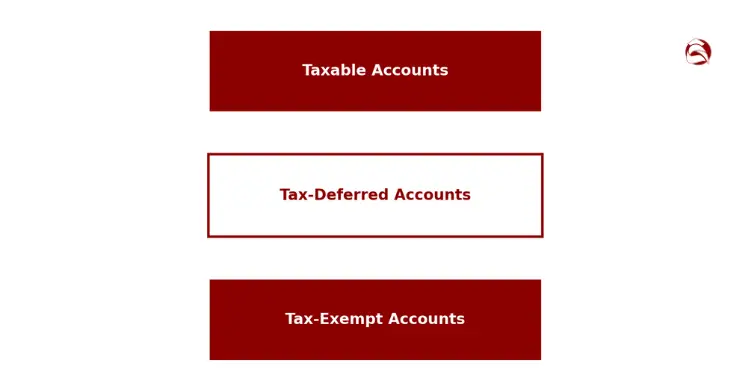

Optimizing Tax Efficiency And Account Selection

Good investment results often depend on choosing the right accounts wisely. Many focus on pre-tax gains, but the real goal is after-tax wealth. Smart tax planning can increase your after-tax returns by 0.5-1.5% each year. This can add up a lot over time.

When I look at new clients’ portfolios, I often see the same investments in different accounts. This can hurt your financial future a lot. It’s not about avoiding taxes, but preventing unnecessary losses.

“Asset location” is more than just where you put your money. It’s about where you put it. For example, putting $10,000 in a bond fund in a taxable account versus an IRA can make a big difference over 20 years.

| Investment Type | Taxable Account | Tax-Deferred (IRA, 401k) | Tax-Exempt (Roth) |

|---|---|---|---|

| High-yield bonds | Poor choice | Excellent choice | Good choice |

| Municipal bonds | Excellent choice | Poor choice | Poor choice |

| Growth stocks | Good choice | Fair choice | Excellent choice |

| REITs | Poor choice | Excellent choice | Good choice |

Good financial planning means choosing the right accounts for your investments. For example, put income-generating investments in tax-advantaged accounts. Growth investments or municipal bonds are better in taxable accounts.

Morgan Stanley research finds that optimal asset location—placing income-heavy assets inside tax-advantaged accounts and tax-efficient equity index funds in taxable accounts—can boost after-tax returns by about 0.30 % per year, compounding meaningfully over time. Ref.: “Shalett, L., Hunt, D., Ye, Z., & Wang, S. (2022). Tax Efficiency: Getting to What You Need By Keeping More of What You Earn. Morgan Stanley Wealth Management.” [!]

Your advisor should think about your taxes now and in the future. If you’ll be in a lower tax bracket in retirement, tax-deferred accounts might be better. But if you’ll pay more taxes later, Roth accounts could be a good choice for your short-term goals and long-term security.

Coordinating Tax Loss Harvesting Opportunities

Tax loss harvesting is a key service for financial planners. It helps you use investment losses to lower your taxes. This can save thousands of dollars each year without risking your investments.

Here’s how it works: your advisor looks for investments that have lost value. They sell these to use the loss for tax purposes. Then, they buy similar investments to keep your market exposure.

For example, if a fund you own drops by $10,000, your advisor might sell it. Then, they buy a similar fund. This keeps your investment mix while using the loss to offset gains or income.

Tax laws are complex and can change. Morgan Stanley does not give tax or legal advice. You should talk to your tax and legal advisors before setting up a Retirement Account. They can help with tax and ERISA rules.

Effective tax loss harvesting needs careful timing and planning. There are rules against buying the same investment too soon after selling it. Your advisor must follow these rules while keeping your investment mix right.

The best advisors work with your tax team during big life changes. They make sure your investments match your tax situation. For example, they might move income around to save on taxes.

Advisors should also check mutual funds for tax efficiency. Some funds pass on a lot of capital gains, even if you didn’t make a profit. These “phantom gains” can lead to tax bills even when the market is down.

Next, review your accounts for tax-saving chances. Ask your advisor to check your portfolio for tax efficiency. This simple step can show ways to improve your after-tax returns without changing your investment strategy.

To avoid common pitfalls in investment goal setting, Investment Goal Setting Mistakes Beginners Should Avoid

Reviewing Progress Through Regular Advisor Meetings

Advisor meetings are key to keeping your investment plan on track. They turn a simple relationship into a strong partnership focused on your financial success. Working with an advisor who values regular talks means you get more than just portfolio management. You also get ongoing advice that fits your changing life.

An advisor will keep you on track with regular meetings. These meetings create accountability and keep you moving forward. In my 12 years helping clients, I’ve seen the best relationships have a regular rhythm of reviews.

The Meeting Framework That Drives Results

Different meetings serve different purposes in your financial journey. Each type of meeting helps you reach your financial goals in its own way.

| Meeting Type | Frequency | Primary Focus | Key Outcomes |

|---|---|---|---|

| Quick Check-in | Monthly | Immediate concerns, market reactions | Emotional reassurance, minor adjustments |

| Progress Review | Quarterly | Performance tracking, rebalancing needs | Portfolio alignment, tactical shifts |

| Strategy Session | Semi-annually | Goal progress, life changes | Strategy refinement, priority adjustments |

| Comprehensive Review | Annually | Full financial picture, long-term planning | Major strategy updates, tax planning |

The best advisor relationships aren’t just about quarterly reports. They’re about connecting investment decisions to your life goals. A good advisor will help you plan for both expected and unexpected life changes.

Preparing for Productive Review Meetings

To get the most from your advisor meetings, prepare well. Being ready ensures your time together is spent on decisions that move you forward.

Before your next meeting, gather these items:

- Updates on major life changes (job, family, health, housing)

- Questions about recent market events or economic news

- Progress on financial goals you’ve previously established

- New financial priorities or concerns that have emerged

- Recent tax documents or estate planning updates

Your advisor can also prepare well if you share these items in advance. This teamwork ensures meetings focus on your pressing concerns and long-term goals. The Financial Industry Regulatory Authority suggests documenting these discussions for a clear record of advice and decisions.

“read also: Investment Goal Planning Basics for Beginner Investors“

How Regular Reviews Prevent Emotional Decisions

Market volatility can lead to emotional decisions that harm your investment plans. I’ve helped clients through many market corrections. The key to success often lies in having regular reviews that keep you focused on long-term progress.

During tough markets, your advisor will help you see short-term changes in context. These talks are key when looking at your progress toward goal-based investing targets. These targets provide clear measures of success beyond just market performance.

An advisor’s objective view during meetings acts as an emotional shield. Instead of reacting to market news, you make decisions based on your goals and strategy. This disciplined approach helps avoid the common mistake of selling low and buying high.

Technology-Enhanced Review Experiences

Today’s review meetings use interactive tools that model different scenarios in real-time. These tools help you see possible outcomes and make better decisions during meetings.

Advisors can create dynamic financial models that adjust as your inputs change. For example, you might explore how different retirement dates or spending levels affect your success. This interactive approach makes complex ideas clear and tangible.

The best advisors use technology while keeping the human touch that makes financial guidance meaningful. Digital tools enhance meetings without replacing the importance of personalized advice tailored to your unique situation.

Evaluating Your Advisor’s Meeting Value

Not all advisor meetings are equal. To see if your meetings are worth it, look for these signs:

- Meetings focus more on your goals than on market performance

- Your advisor asks thoughtful questions about your life changes

- Discussions include both short-term tactics and long-term strategy

- You leave with clear action items and next steps

- Technical concepts are explained in terms you understand

If your meetings feel like one-way presentations, it’s time to talk to your advisor. The best relationships involve real dialogue that addresses your concerns and offers professional advice.

Essential Questions For Your Next Review

To make the most of your next advisor meeting, ask these focused questions:

- “How has my progress toward specific goals changed?”

- “What adjustments do you recommend based on recent market conditions or changes in my situation?”

- “Are there any tax-efficiency opportunities we should consider before year-end?”

- “How are my investment costs affecting my long-term returns?”

- “What risks should I be more aware of in the current environment?”

These questions ensure your advisor covers both performance tracking and forward-looking strategy. They also show your engagement, leading to more tailored advice.

Regular advisor meetings are key to long-term investment success. With preparation and purpose, these sessions turn abstract financial ideas into practical steps. The regularity of these meetings, not just their content, is what sets successful investors apart from those who react to market noise.

Transitioning Toward Self Directed Investing Over Time

As you learn more about investing, your relationship with a financial advisor might change. Many start with full-service help but learn to manage parts of their money on their own. This shift can save money while you keep moving toward your financial goals.

Evaluating Robo Advisory Platforms Support

Robo-advisors are a mix between traditional advisors and self-management. They cost 0.25% to 0.50% a year, much less than advisors. They’re great for simple portfolio management but not for complex plans.

Think about what parts of your money are easy to manage on your own. A good advisor can tell you where to start.

Read More:

Gradually Shifting Toward Cost Effective Independence

Getting to manage your own investments should be a slow process. Start by handling a small part of your money. Keep your advisor for the tricky stuff.

Make goals to know when you’re ready for more independence:

– Manage a small portfolio segment well

– Make smart tax choices

– Know when to ask for help with tough issues

Remember, the cheapest option isn’t always the best. Sometimes, paying for advice is worth it, like during big life changes or when the market is shaky.

{kind=link}