Is managing money truly as complex as many Americans think? A 2024 Debt.com survey found that 89% of people who budget say it helps them get out of or stay out of debt.

“You must gain control over your money or the lack of it will forever control you,” says financial coach Dave Ramsey. This wisdom changed my money management after years of chaos.

I’ve tried many systems, from simple spreadsheets to expensive apps. I found something key: the best personal budget isn’t about fancy features. It’s about finding what fits your life naturally.

Today, options range from free templates to premium apps costing up to $17.99/month, like EveryDollar. This variety can make people unsure, not moving toward their financial goals.

The right system should be a helpful friend, not another task. After trying seven apps, I learned how to pick tools that last.

This guide will help you choose based on your habits, tech comfort, and money goals. Whether you’re paying off debt, saving for a home, or controlling daily spending, we’ve got you covered.

- Choose a Budgeting System That Fits Your Lifestyle, not the other way around.

- Why Free Budgeting Tools May Be Best for Beginners

- Tailor Your Budgeting Tool to Your Financial Goals

- Prioritize Consistency Over Complexity in Expense Tracking

Assess Your Tech Comfort and Tracking Preferences First

I spent $84 on fancy budgeting apps before I learned a lesson. I needed tools that fit my money habits, not the other way around. This taught me that the best budgeting method isn’t always the same for everyone.

Before looking at specific tools, know your tech comfort and how you track money. Do you love new tech or prefer simple ways? Your choice helps narrow down what’s best for you.

Ask yourself these key questions about your preferences:

- Do you want automatic syncing with your bank accounts, or do you prefer manual entry for greater awareness of your spending?

- Are you detail-oriented, wanting to categorize every transaction, or do you need a big-picture view of your monthly expenses?

- How much time can you realistically commit to maintaining your financial plan each week?

- Do you prefer mobile apps or desktop programs for managing important information?

Your answers show which tools fit your life best. If you love tech and automation, cloud apps might be great. If you like hands-on control, a customized spreadsheet could be perfect.

The best budget is the one you’ll actually stick with. Everything else is just wishful thinking.

Think about your financial goals too. Different tools help with different goals. Some focus on saving for emergencies, while others help with debt or tracking income.

Your money habits are very important. I’ve seen friends give up on fancy budgeting systems because they didn’t fit their habits. One friend loved detailed tracking and used a complex spreadsheet. Another found success with a simple envelope system.

Take five minutes to write down your preferences now. Knowing yourself will save you time and money. The goal is to find the tool that works best for you, not the “best” one.

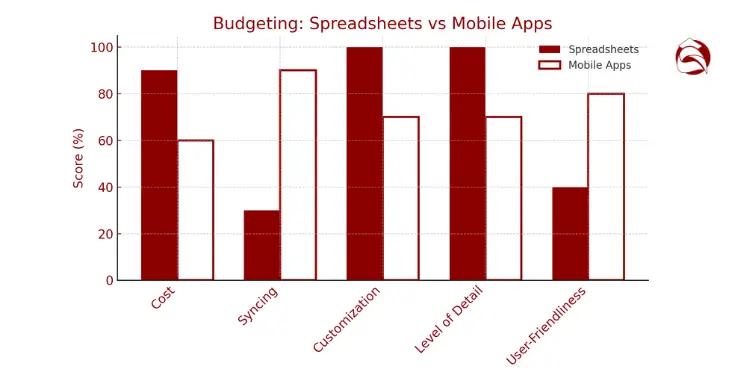

Compare core features of spreadsheets versus mobile budgeting apps

Choosing between a budget spreadsheet and a mobile app is a big decision. It depends on whether you want control or convenience. I’ve tried both and found they each have their own benefits.

Spreadsheets let you control your budget exactly how you want. You don’t pay monthly fees. But, mobile apps make it easy to stay on budget because they’re always with you.

| Feature | Budget Spreadsheets | Mobile Budgeting Apps | Best For |

|---|---|---|---|

| Cost | Free to low one-time cost | Free to $15/month subscription | Spreadsheets for budget-conscious users |

| Customization | Unlimited flexibility | Limited to app design | Spreadsheets for unique financial situations |

| Data Entry | Manual input required | Automatic transaction import | Apps for busy individuals |

| Accessibility | Computer access needed | On-the-go via smartphone | Apps for frequent travelers |

| Learning Curve | Moderate to steep | Generally gentle | Apps for beginners |

With spreadsheets, you have full control over your budget. I made a budget worksheet that worked great for my freelance income. But, entering data every week can be hard to keep up with.

Mobile apps like YNAB and Mint connect to your accounts and categorize your spending. They’re easy to use but might not offer as much privacy or customization. Apps like YNAB focus on zero-based budgeting, while Mint uses the 50/30/20 rule.

“The best budgeting tool isn’t the most sophisticated one—it’s the one you’ll actually use consistently month to month.”

When choosing, think about what each tool can do for you. If you’re paying off debt, look for tools with debt snowball features. If saving for retirement is your goal, find tools that help you track your progress.

Don’t get caught up in features you won’t use. Focus on how each tool helps you manage your money every day. Look for tools that help you stay within your budget in important areas.

Look for Real-Time Sync and Category Alerts Capability

Two key features to look for are real-time sync and category alerts. These features make tracking your money much easier.

Real-time sync keeps your budget up to date. I once spent too much on dining out because my app wasn’t updating fast enough. By the time I saw the problem, I’d already gone over my budget.

Look for apps that update quickly. Most premium apps offer real-time syncing, while free ones may update daily or require manual refreshes. Google Sheets can update fast with bank feed add-ons, but it takes some tech know-how to set up.

Category alerts help you avoid overspending. Good budgeting tools warn you before you go over budget. For example, they might say you’re close to using up your grocery budget.

Some apps even predict when you might overspend. They warn you early, based on your spending patterns. This helps you change your spending before it’s too late.

When trying out tools, see if you can customize alerts. Can you set different limits for different categories? Can you choose how you get notifications? These small features make a big difference in how well you stick to your budget.

It’s also important to categorize your expenses well, no matter the tool. Both spreadsheets and apps let you separate fixed and variable expenses. This makes it easier to find areas where you can save more.

The goal is to change your spending habits as you go. The right tool should help you stay on track every day. It should feel like a partner in managing your money, not just another app or file.

Evaluate cost data security and collaboration needs objectively

When picking a budget tool, look at its security and how it helps you work together. Tools range from free to over $100 a year. But, the price doesn’t always mean it’s the best.

Think if you really need to pay for it. Many people spend money on tools but only use simple features. Remember, the tool’s cost is part of your budget.

Security is key, but many forget about it until it’s too late. Budget tools handle your financial info, like debt and spending. This info is very personal.

If you’re not sure about digital tools, you can use paper. But, digital tools usually offer better security. They keep your financial plan safe.

“read more: How to fill budget categories for category clarity“

Check Encryption Standards and Two-Factor Authentication Options

Security can’t be ignored with financial tools. A friend’s budget app was hacked, showing how important it is. Look for tools with strong security, like 256-bit encryption.

When selecting budgeting tools, prioritize those offering robust security measures such as 256-bit encryption and two-factor authentication (2FA). These features are essential for protecting sensitive financial data from unauthorized access. Ref.: “TechRadar. (2022). Best budgeting software of 2025. TechRadar.” [!]

This level of protection keeps your data safe, even if the company gets hacked. Check for security certifications like SOC 2. It shows the service has been checked for security and budget.

Two-factor authentication (2FA) is a must for financial tools. It adds an extra layer of protection. Good 2FA options include:

- Authentication apps (like Google Authenticator)

- SMS verification codes

- Biometric verification (fingerprint or face recognition)

- Email verification (least secure option)

Don’t trust services that only use email for 2FA. Email accounts are often hacked first. Look for tools with extra security features like IP login restrictions and session timeout controls.

For shared finances, you need tools that let everyone work together. Look for tools that support multiple users. This is important for budgets that need to be shared.

| Collaboration Need | Recommended Features | Example Tools |

|---|---|---|

| Couples managing finances | Shared view with privacy options | Honeydue, Zeta |

| Family budgeting | Multiple user accounts with permissions | YNAB, EveryDollar |

| Roommates sharing expenses | Expense splitting, limited access | Splitwise, Tricount |

Honeydue allows couples to view and manage their finances together, offering shared views with privacy options. You can link bank accounts and credit cards. But, you choose what to share.

Honeydue enables couples to manage finances collaboratively by linking bank accounts, categorizing expenses, and setting bill reminders. Users can choose which accounts and transactions to share, maintaining individual privacy while promoting joint financial planning. Ref.: “Honeydue. (2025). Honeydue • Finance App for Couples. Honeydue.” [!]

The free app sorts your expenses for you. You can also make your own categories. It alerts you when you’re close to your spending limits.

Think if you need separate budgets or one shared one. It depends on your relationship. Some couples want to share everything, while others like to keep some things private.

Be honest about what you need. I’ve seen couples spend a lot on tools they didn’t use. Sometimes, simple spreadsheets and meetings work better than fancy tools.

Remember, tools that are easy to use might not be as secure. Think about what you’re comfortable with. If you have a lot of money or privacy concerns, local spreadsheets might be safer.

Test drive shortlisted tools using one week of real spending

Test a budgeting tool for a week using your actual spending data. This shows more than any review. I saved a lot by testing tools first. It helps find a tool that fits your spending habits, not the other way around.

Most premium budgeting services offer free trials from 7 to 30 days. Free options can be tried right away. Start by adding a week’s worth of real transactions. This gives enough data without too much setup time.

See how the tool works with your spending. Does it sort your transactions right? Can it handle irregular income or expenses? Notice how easy it is to use every day.

The most sophisticated budgeting tool is worthless if you don’t actually use it consistently.

Check the mobile version, even if you use the desktop more. You’ll want to check balances before buying things. If you share finances, have everyone test it. A tool that works for you might confuse others.

How often you check your budget depends on you. If you’re sure about your money, once a month might be enough. Others might check weekly or after every buy.

Tools like Goodbudget focus on planning, not just tracking. It uses the envelope system for budgeting. This lets you control your money better.

Create a Simple Evaluation Scorecard

Make a scorecard during your test week. Rate each tool based on what matters to you. This helps you see past marketing and find the best tool for you.

| Evaluation Criteria | Questions to Ask | Importance (1-5) | Tool A Score | Tool B Score |

|---|---|---|---|---|

| Ease of Use | How intuitive is the interface? How many clicks to complete common tasks? | Your rating | Your score | Your score |

| Transaction Categorization | Does it accurately sort your spending? How easy is it to create custom categories? | Your rating | Your score | Your score |

| Reporting Capabilities | Are the insights meaningful? Can you easily track progress toward goals? | Your rating | Your score | Your score |

| Mobile Experience | Is the app responsive? Can you quickly check balances before purchases? | Your rating | Your score | Your score |

| Overall Satisfaction | Did you actually enjoy using it? Will you continue using it long-term? | Your rating | Your score | Your score |

Look closely at how apps handle recurring expenses. Some tools save time by predicting future buys. Others show spending in charts and graphs.

The goal is to find a tool you’ll use all the time. A simple spreadsheet can be better than a fancy app you won’t use. Use your test week to mimic how you’ll really use the tool.

By the end of your trial, you’ll know which tool is best. This careful approach helps you make choices based on real use, not just promises.

Decide on final tool and migrate historical data smoothly

After your one-week trial, it’s time to choose your budgeting tool. Make sure the transition is smooth. Many people fail because they don’t stick with the new system.

Start with a “clean slate” approach. Begin with current balances instead of old data. This makes tracking your monthly cash flow easier.

If you need to track taxes or expenses, import old data. Many tools can do this for you. But, you might need to sort some transactions yourself.

Customize Your Tool for Long-Term Success

Customize your tool to fit your needs. Add subcategories for important expenses. This makes your budget easier to manage.

Set budget amounts based on your actual spending patterns. Use real figures as your baseline. Adjust these as you improve your finances.

Try both old and new systems for a month. This helps catch any missing transactions. It’s a small step to avoid big mistakes.

“The most successful budgeters I know don’t just pick a tool—they customize it to fit their life and financial goals. Your budget should work for you, not the other way around.”

Manage Subscription Costs and Renewals

Mark your calendar for when trials end and renewals happen. Many forget about auto-renewals. Some apps are free, while others charge a fee.

For example, EveryDollar’s premium costs $79.99 a year or $17.99 a month. Compare this to other options to make smart choices.

Empower offers more than basic budgeting. It tracks net worth and investment management. It’s easy to use on any device.

Empower provides tools for budgeting, net worth tracking, and investment management, catering to users seeking a comprehensive financial overview. Its features include automatic transaction categorization and personalized financial insights. Ref.: “Empower. (2025). What features are available on the Empower app? Empower.” [!]

“read also: How to close budget month in minutes daily“

Document Your Setup for Future Reference

Document your setup, including login info and customizations. Store it securely. This is useful if you need to reset or switch tools.

Take screenshots of your setup. Set reminders to review your budget. This keeps your system safe, even if you change devices.

Most budgeting apps are available on both iOS and Android platforms. But, features and syncing may differ. Make sure it works on all your devices.

| Budgeting Tool | Free Version Features | Premium Cost | Best For | Data Migration Ease |

|---|---|---|---|---|

| EveryDollar | Basic budget categories, manual transaction entry | $17.99/month or $79.99/year | Zero-based budgeting fans | Moderate (manual entry required) |

| Mint | Automatic syncing, bill tracking, credit score | Free (ad-supported) | Beginners tracking multiple accounts | Easy (automatic import) |

| YNAB | 34-day free trial only | $14.99/month or $98.99/year | Detailed budget management | Complex (learning curve) |

| Empower | Basic budgeting, net worth tracking | $3.99/month | Investment tracking alongside budgeting | Easy (automatic categorization) |

| Excel/Google Sheets | Fully customizable templates | Free (Excel requires Office) | DIY budgeters who want total control | Manual (high customization) |

Schedule quarterly reassessment to verify chosen tool is right

I learned a hard lesson about sticking with a spreadsheet too long. It stopped working for me, but I didn’t change. Your perfect budgeting tool today might not fit your needs six months later.

Mark four dates on your calendar each year to check your budget. Ask if tracking money is easy or hard. Are you using all the app’s features? Has your money situation changed?

Read More:

Look for signs your budget needs an update. Maybe you’re missing transactions or using old categories. Or maybe you’ve moved to a new financial goal.

Catherine Hawley, a CFP in Monterey, says you don’t need to track every detail. “You just need to know you’re in a good range.” Tracking your spending doesn’t have to be hard.

Going back to basics, like using pen and paper, can be better than apps. The best tool is one you’ll use every day. By checking your tools every quarter, you can keep up with your financial changes.

{kind=link}