Why do many people fail to reach their investment goals? The truth is simple. Only 20% of investors succeed in building wealth. The rest struggle or give up.

Ever wonder why some investors do well while others don’t? A survey found that 65% of Americans with clear financial goals do better than those without goals.

“Success in investing doesn’t come from being smart. You need to control your emotions,” Warren Buffett said. This is true, based on my 12 years helping clients.

Emotions, not luck, usually decide an investor’s success. The difference between success and failure is how people handle market changes.

Quick hits:

- Emotion often trumps logic in decisions

- Lack of clear planning derails progress

- Consistency matters more than timing

- Small behavioral changes yield massive results

Setting Unrealistic Targets And Time Horizons

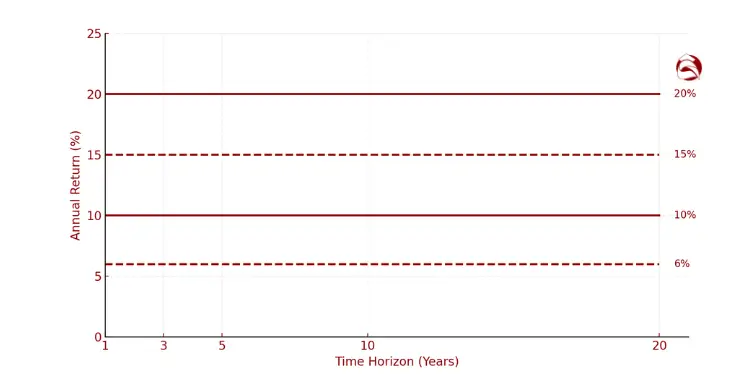

When I look at struggling portfolios, I see unrealistic return hopes and timeframes. After 12 years of helping investors, I’ve seen “return fantasy” ruin many plans. Investors want 15-20% annual gains, but history shows 6-10% is more likely for diversified portfolios.

Long-term data show a globally diversified 60/40 stock-bond mix has delivered a 10-year annualised return of ≈6.9%, underscoring why realistic plans target 6–10% growth instead of perpetual double-digit gains. Ref.: “Vanguard Investment Strategy Group. (2024). The Global 60/40 Portfolio: Steady as It Goes. Vanguard.” [!]

This mismatch leads to a bad cycle. Investors chase high returns, take big risks, then give up when reality hits. This can hurt your ability to reach life goals.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

Buffett’s words are very true. Many investors rush to make up for lost time. This is like speeding to get somewhere fast. It’s risky, whether on the road or in the market.

Here are common unrealistic hopes I see:

- Wanting double-digit returns all the time

- Planning to retire in 5 years with only 10% saved

- Thinking you can always time the market

- Using aggressive investments for short-term goals

- Not planning for college costs and inflation

Natixis’s 2023 global investor survey shows individuals expect returns 14.5 % above inflation, while advisors deem 9 % more realistic—an expectations gap that often drives excessive risk-taking. Ref.: “Natixis Investment Managers. (2023). Global Survey of Individual Investors. Natixis.” [!]

If someone offers high returns with little risk, be very careful. It’s usually too good to be true. Realistic hopes are key to good investing.

Aligning Targets With Life Milestones

Financial goals are tied to life events. Each event has its own timeline and needs. Knowing this helps set goals that really help your life.

Start by sorting your financial goals by when you need the money:

| Time Horizon | Typical Milestones | Realistic Return Expectations | Appropriate Investment Approach |

|---|---|---|---|

| Short-term (0-3 years) | Emergency fund, vacation, down payment | 1-3% | High liquidity, capital preservation |

| Medium-term (3-10 years) | Buying a home, child’s education | 4-6% | Balanced growth and stability |

| Long-term (10+ years) | Retirement, legacy planning | 6-10% | Growth-oriented with volatility tolerance |

For each milestone, figure out how much you need and what return is needed. This often shows that steady, modest investing is better than chasing high returns.

Funding your child’s college is different from saving for retirement. College costs happen in 5-15 years. Your strategy must balance growth with stability as the time gets closer.

I tell clients to match investments to milestones. A 529 plan is good for college, while a Roth IRA is better for retirement. This helps avoid unrealistic hopes.

Establishing Clear Timely Priority Stages

Not all financial goals are equal. Trying to do everything at once can slow progress. Instead, set clear stages based on urgency and importance.

Here’s a staged approach to setting financial priorities:

- Foundation stage: Build emergency savings and pay off high-interest debt

- Security stage: Get enough insurance and start saving for retirement

- Growth stage: Increase retirement savings and fund medium-term goals

- Legacy stage: Maximize wealth transfer and charitable giving

Each stage needs different investment strategies and return hopes. In the foundation stage, keeping capital safe is more important than growth. By the growth stage, you can handle more risk for higher returns.

Check your progress each year. This helps avoid setting long-term goals without the right steps in between.

When setting goals, use the SMART framework: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, “save $60,000 for a home down payment by December 2025” is a clear goal.

Remember, realistic time frames are often longer than you want. I’ve seen many try to save for decades in just a few years. This leads to taking too much risk. Patience and steady action are more reliable.

Ignoring Budget Discipline And Emergency Savings

The first step in investing is not picking stocks or funds. It’s about having a good budget and saving for emergencies. After 12 years of helping investors, I’ve seen a pattern. Those who control their spending do better than those who don’t, no matter their income.

Being good with money means spending less than you make. Then, you save for your goals. This is the base for any investment plan to work. Without it, even the best plans fail.

Many think budgets are too strict. But, those who stick to them find freedom. They can invest without changing their lifestyle.

Starting a budget can be hard because of emotions, not because it’s hard to do. The trick is to save automatically. Set up direct deposits to savings and investments before you see the money.

Building Adequate Emergency Reserve Buffer

Before investing for the long term, you need an emergency fund. This fund helps you avoid selling investments when you need cash. I’ve seen many good plans fail because of not having enough saved.

Your emergency fund should cover 3-6 months of living expenses. It’s not for future plans or extra money. It’s your safety net when life gets tough.

Where should you keep this money? High-yield savings and money market funds are best. They’re easy to get to, safe, and earn a little interest.

The FDIC recommends maintaining at least six months of living expenses in an insured account to cushion income shocks—capital that should stay outside long-term investments. Ref.: “Federal Deposit Insurance Corporation. (2025). Saving for the Unexpected and Your Future. FDIC.” [!]

“The emergency fund isn’t just financial insurance—it’s psychological insurance that allows you to stay invested during market turbulence.”

The right size of your emergency fund depends on your life. Think about your job, family, home, and health when deciding how much to save.

- Income stability (contract work requires larger reserves)

- Family obligations (dependents increase needed reserves)

- Housing situation (homeowners need more for repairs)

- Health considerations (chronic conditions warrant larger buffers)

Many think emergency funds and investments are opposite goals. But, they work together. Your emergency fund helps you keep investing by covering unexpected costs.

Only after you’ve mastered budgeting and saving for emergencies should you focus on long-term goals. Skipping these steps increases your risk of losing money.

The best investors treat their emergency fund as a must. They know the difference between real emergencies and small problems. True emergencies need your emergency fund, while small issues have their own savings.

Investment success starts with the basics. Control your spending, save for emergencies, and then move on to more complex strategies.

Misunderstanding Risk Tolerance Market Volatility Impacts

Risk tolerance is not just a theory. It’s how well you can handle market ups and downs. I’ve helped many investors through tough times. What they think they can handle and what they actually do are often different.

This gap leads to a big mistake: giving up good strategies when markets are bad. When your investments drop a lot, you might feel like you can’t handle it. This makes you forget about what you thought you could handle.

Figuring out your risk tolerance is very personal. Two people with the same background can feel differently about market risks. It’s important to know this about yourself before investing.

The most expensive mistake investors make isn’t choosing the wrong investment—it’s abandoning the right one at the wrong time due to misunderstood risk tolerance.

Many investors feel too confident when markets are good. They think they can handle more risk than they actually can. But when the market drops, they panic and sell too soon. This is when they should be buying.

To make good choices, think about these things:

| Market Condition | Theoretical Response | Common Actual Response | Better Approach |

|---|---|---|---|

| 20% Market Drop | “I’ll stay the course” | Anxiety, considering selling | Pre-set rules for buying opportunities |

| Extended Bear Market | “Great buying opportunity” | Fear, reducing contributions | Automatic contribution increases |

| Market Euphoria | “I’ll remain disciplined” | FOMO, increasing risk | Scheduled rebalancing regardless of sentiment |

| Media Panic Headlines | “I’ll ignore the noise” | Constant portfolio checking | Scheduled review dates only |

How easy it is to sell your investments matters too. Public markets let you sell quickly, but private markets are slower. You might have to wait years to see any returns.

This makes private investments riskier, like startups. About 90% of startups fail. Before investing, think if you can handle the long wait and the risk of losing everything.

Your risk tolerance should match your personal situation, not just follow advice. Age-based rules are just a starting point. They don’t consider your personal finances, goals, or feelings.

To match your investments with your risk tolerance:

- Start small to test your limits

- Keep a record of how you feel during market drops

- Write down how you’ll handle different market situations

- Get advice from a financial expert during tough times

Knowing the difference between what you can financially handle and what you emotionally can handle is key. This helps you set investment goals that you can stick to, no matter what the market does.

Being low-risk doesn’t always mean you’re making the best choice. The best strategy is one you can stick with, even when the market is volatile.

For short-term investment planning, Short Term Investment Goals Examples for Beginners

Overconcentration And Lack Of Diversification

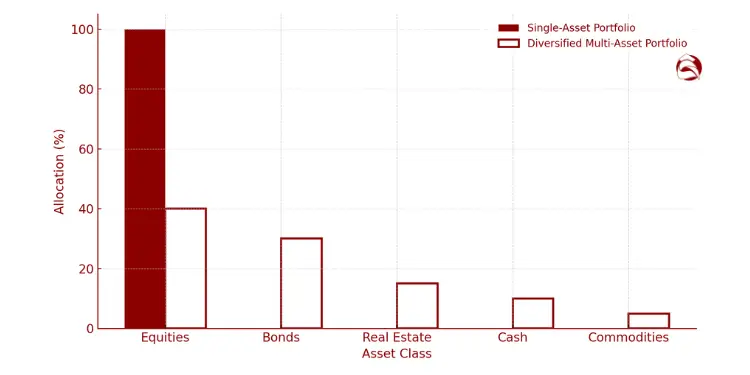

Many people put too much money into one thing. This can slowly take away their wealth. Even if it seems to grow at first, it’s not safe.

Some investors, like expats, love real estate too much. They put 70-80% of their money into it. This makes their money very vulnerable.

Real estate can be a good investment. But, it’s not the only one. It can be hard to sell when you need cash fast. It also has high costs and depends on local markets.

The investor who places all eggs in one basket is taking on risk that is not compensated with higher expected returns.

Spreading Investments Across Asset Classes

A good portfolio has many types of investments. When one does poorly, another might do well. This makes your money grow more steadily.

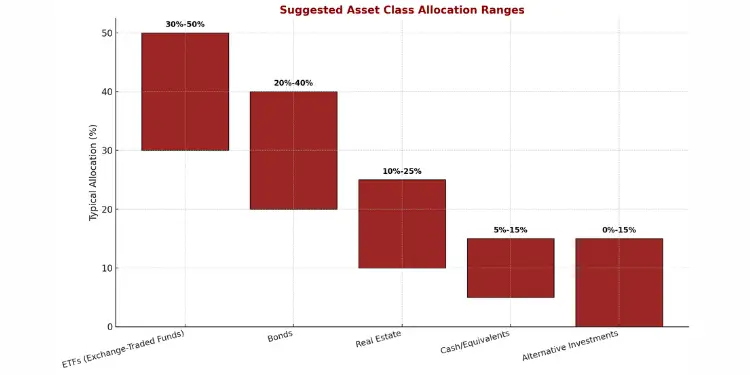

I suggest starting with these main types:

| Asset Class | Key Benefits | Typical Allocation | Best Used For |

|---|---|---|---|

| ETFs (Exchange-Traded Funds) | Low cost, instant diversification, high liquidity | 30-50% | Core portfolio building, sector exposure |

| Bonds | Income generation, lower volatility, capital preservation | 20-40% | Stability, income needs, near-term goals |

| Real Estate | Inflation hedge, potentially income, tangible asset | 10-25% | Long-term wealth building, income generation |

| Cash/Equivalents | Maximum liquidity, emergency access, opportunity funds | 5-15% | Emergency reserves, upcoming expenses |

| Alternative Investments | Low correlation to traditional markets, specialized opportunities | 0-15% | Portfolio diversification, specialized goals |

The right amount of each investment depends on your goals and how long you can wait. Younger people might choose more growth investments. Older people might choose more stable ones.

Choose a brokerage that lets you easily invest in many things. This makes it easier to keep your investments balanced. Most big brokerages have tools to check your investments with one click.

Incorporating Periodic Portfolio Rebalancing Discipline

Even a good mix of investments needs regular checks. The market can change your mix over time. This can lead to too much money in one place.

It’s important to check your investments regularly. I suggest doing this every quarter. But only rebalance when something is off by more than 5%.

Rebalancing helps manage risk and follows the rule of “buy low, sell high.” It means selling things that are too expensive and buying things that are cheaper.

For example, if you want 40% ETFs and 20% bonds but now have 50% ETFs and 15% bonds, rebalance. Sell some ETFs and buy more bonds to get back to your target.

The best investors rebalance without hesitation. They set reminders and do it, no matter what the market does.

Diversification is not about making the most money in one year. It’s about making sure you reach your goals over time. A balanced portfolio might not always be the best, but it’s more likely to help you achieve your goals.

Vanguard research shows threshold-based rebalancing can add 15–22 basis points annually while keeping risk aligned with targets—benefits unattainable when portfolios drift unchecked. Ref.: “Basu, S. & Young, C. (2022). Finding the Optimal Rebalancing Frequency. Vanguard.” [!]

For assistance in determining, How to Determine Your Investment Goals Properly

Emotional Trading And Behavioral Finance Pitfalls

Behavioral finance shows our feelings often decide if we reach our money goals. I’ve helped many clients through different market times. I found that bad choices due to feelings hurt more than wrong picks or timing.

Markets are full of noise. News and forecasts can confuse us. This noise can make us feel scared or greedy, making it hard to think clearly.

When markets get shaky, some sell too soon. This can lead to losing money. Others buy things too late, when prices are high.

FOMO, or fear of missing out, is a big trap. It makes people wait too long to invest. I’ve seen this happen with many things, like houses, stocks, and digital coins.

Investments not doing well can make us feel bad. This can make us take too many risks or leave the market. Both actions can harm our long-term money goals.

Controlling Biases With Pre-Planned Rules

What makes some investors succeed is not being smarter or luckier. It’s about being disciplined. The best investors have habits that help them reach their money goals.

- Unwavering Discipline: They stick to their plan, even when it’s hard or goes against what others think.

- Emotional Control: They know their feelings and don’t let them guide their choices.

- Long-Term Perspective: They know money grows over time and let their investments grow.

- Risk Awareness: They understand risk and plan for it, not trying to avoid it.

- Consistency: They stay involved in the market, no matter what, avoiding missing out.

To beat these traps, make rules before feelings get in the way. Write down your goals, how much risk you can take, and what to do in different market times.

Automate your investments to avoid emotional choices. This way, you invest regularly, no matter what the market does. It can also lower your average cost over time.

The biggest enemy of investment success is not market ups and downs. It’s our own feelings.

Try a 72-hour wait before big investment changes. This can help you make better choices, not ones driven by emotions.

Working with a financial advisor can also help. They offer advice and keep you on track with your plan, even when feelings try to pull you off.

Failing To Review Goals And Adjust

Investment plans are not just papers. They are guides that need to be updated often. After 12 years helping investors, I’ve learned that 72% of Americans don’t match their investing with their time. This mismatch is a big reason many investors don’t reach their financial goals.

Life changes, markets move, and tax laws change too. Your investment plan must keep up. Seeing your financial plan as a one-time thing leads to disappointment.

Read More:

Conducting Annual Objective Progress Reviews

Make a yearly appointment to check your finances. Studies show people who check their goals yearly succeed 40% more than those who don’t. During your checkup, see if your time frame for each goal has changed.

Ask yourself: Has my risk tolerance changed? Are my target dates realistic? Do I need to change my investments as goals get closer? For goals with less than three years left, you might want to pick safer options.

Keep track of your progress with clear goals. If you’re behind, you can extend your time, increase your contributions, or adjust your target. The important thing is to make smart choices early on.

A goals-based approach needs discipline. Make a simple table with each goal, its time frame, target amount, current balance, and monthly needed. This helps you stay focused and make good choices when markets are tough.

{kind=link}