When I bought my first home at 32, a realization hit me hard. I had a mortgage but no safety net for my family. This made me think about protection options.

According to recent data, 41% of Americans have no life insurance coverage. Yet, 85% think families need some financial protection. Many people don’t know if they need a policy.

Not sure if you need coverage? Ask yourself: Would your death cause financial trouble for your loved ones? If yes, getting coverage is a good idea. A policy is a deal between you and an insurer. Your payments can help those who depend on you.

My neighbor Tom waited too long to decide. He thought his savings were enough. But, he found out he needed more to cover his mortgage, college costs, and income needs.

We’ll help you figure out if you need financial protection. We’ll explore coverage tools, policy types, and smart timing strategies without spending too much.

- Learn how to calculate your family’s actual protection needs

- Discover which policy types match different life stages

- Understand when coverage might be unnecessary

- Find the balance between adequate protection and affordable premiums

Start with a Family Financial Check

Before buying life insurance, look at what your family would face without you. I once thought we needed less than we really did. It took a kitchen table full of papers to see the truth.

Life insurance helps your family pay for things they need. If your partner depends on your income, they might struggle without it. Planning now can save them from financial trouble later.

Estimate Income Gaps and Long-Term Needs

First, figure out how much income your family will lose without you. This is the base of how much life insurance you need. Just multiply your yearly income by how many years your family needs support.

For example, if you make $60,000 a year and want to support your family for 15 years, you need $900,000. Financial advisors often suggest 10-20 years of support, based on your kids’ ages and your spouse’s income.

Also, remember the value of benefits like health insurance from your job. These can add up fast if your family has to buy them themselves.

Financial advisors recommend 10-15 years of income replacement for families with children. Ref.: “Life Happens (2023). How Much Life Insurance Do I Need?. Life Happens.” [!]

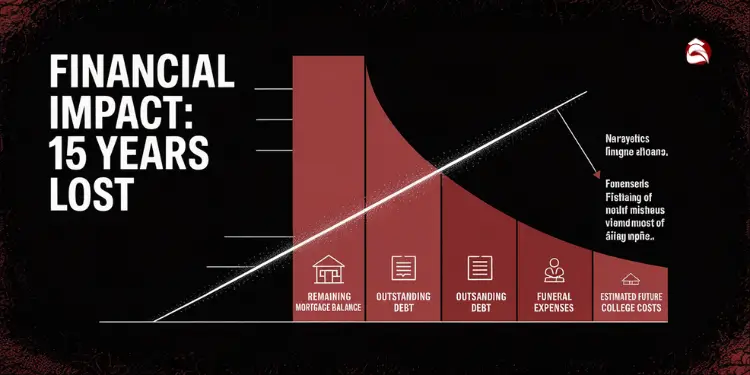

Factor In Debts, Obligations, and Future Costs

Then, list all debts your family will have to pay if you’re not there. The average household has big debts:

- Mortgage: $250,000 (average)

- Car loans: $35,000

- Student loans: $40,000

- Credit card debt: $8,000

Average funeral costs reached $7,848 in 2021, often requiring separate budget consideration. Ref.: “National Funeral Directors Association (2021). Statistics. NFDA.” [!]

Think about future costs too. College can cost $25,000 to $50,000 per year. And final expenses, like funerals, are about $8,300 in 2023.

Make a simple spreadsheet with these numbers. The total might surprise you. Most people don’t realize how much they need until they add it all up.

Your financial situation will change over time. As you pay off debts or take on new expenses, you’ll need to update your insurance. Experts say to check your coverage every 3-5 years or after big life changes.

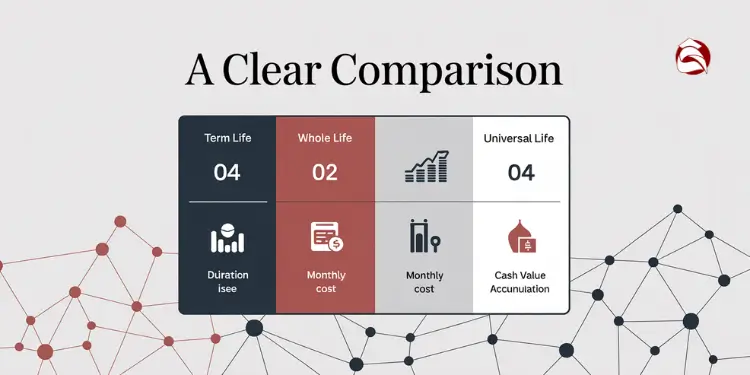

Term vs. Permanent Life Insurance

Choosing between term and permanent life insurance is key for your family’s future. It’s like deciding between renting or buying a home. Each option has its own benefits.

Term life insurance covers you for a set time, like 10, 20, or 30 years. The cost stays the same, making it easy to budget. For example, a healthy 35-year-old might get a $500,000 policy for $25-35 a month.

Term insurance is great when you need it most, like when you have kids or a mortgage. But, it ends when the term is up, unless you renew it at a higher price.

Permanent life insurance lasts forever and has fixed costs. A $500,000 policy might cost $300-500 a month. This means your rates won’t change, no matter what.

| Feature | Term Life Insurance | Whole Life Insurance | Universal Life Insurance |

|---|---|---|---|

| Duration | 10-30 years | Lifetime | Lifetime |

| Monthly Premium | $25-35 for $500K | $300-500 for $500K | $200-400 for $500K |

| Premium Flexibility | Fixed | Fixed | Adjustable |

| Cash Value | None | Guaranteed growth | Variable growth |

Whole life offers predictable death benefits and fixed premiums. It costs more than term insurance. Universal life insurance is more flexible but has investment risks.

“read also: Vital purpose of earthquake insurance“

Understand Cash Value in Permanent Policies

Permanent life insurance has a cash value part that term insurance doesn’t. This part grows over time, tax-free.

Whole life insurance grows cash value at a set rate. It’s safe but might not grow as fast as other investments. The company invests it carefully, focusing on safety.

Universal life insurance might grow faster but is riskier. Your cash value can grow or fall with the market. Some policies guarantee a minimum return, while others don’t.

The cash value in permanent policies can be used for emergencies or retirement. But, loans reduce the death benefit, and early withdrawals may have fees.

For most families, term insurance is best during high-need years. I chose it when my kids were young and we had a mortgage. It was affordable and gave us peace of mind.

Permanent policies are better in certain situations. They’re good for lifelong needs, equalizing inheritances, or estate planning. Don’t let agents push you to expensive permanent coverage if term is better for you.

The right policy isn’t about which type is better—it’s about which one better serves your family’s specific needs and financial goals.

Think about your protection needs, budget, and long-term goals when choosing. Many families use a mix of term and permanent policies. This approach gives them the best of both worlds.

Calculate Optimal Coverage Amount and Duration

Finding the right life insurance coverage isn’t a guess. It’s about using formulas that fit your family’s needs. When I first bought a policy, I just multiplied my salary by ten. But, this method didn’t always work for my family’s finances.

Life insurance is meant to replace your financial help to your family. The right coverage amount should match your family’s needs and goals. Too little coverage can leave your family in trouble. Too much means you’re spending money that could grow your family’s wealth.

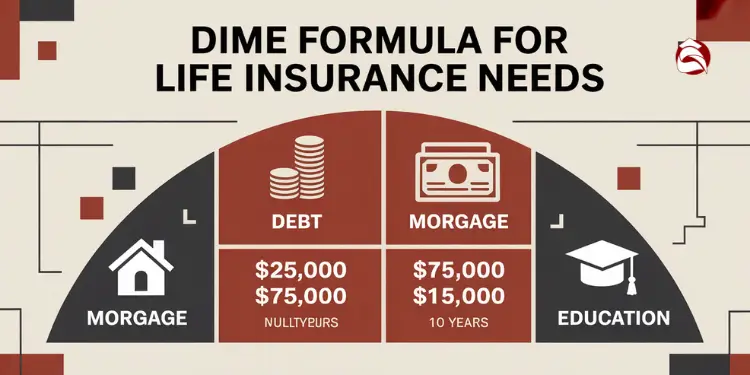

Apply the DIME Formula to Calculate Your Coverage

After my first child was born, I knew I needed more coverage. The DIME formula helped me figure out exactly what my family needed if I were gone.

DIME stands for:

- Debt: All debts except the mortgage (credit cards, auto loans, personal loans)

- Income: Your yearly income times the number of years your family needs support

- Mortgage: The balance left on your home loan

- Education: The cost of college for your kids

The DIME method—summing Debt, Income, Mortgage, and Education obligations—is widely endorsed, including by John Hancock as a comprehensive way to calculate needed coverage Ref.: “How Much Life Insurance Do I Need?” John Hancock (2024). How much life insurance do you need? [!]

Let’s see how it works with real numbers. For a typical family, the calculation might look like:

| DIME Component | Amount | Calculation |

|---|---|---|

| Debt | $30,000 | Credit cards, auto loans, etc. |

| Income | $1,050,000 | $70,000 × 15 years of support |

| Mortgage | $200,000 | Remaining balance |

| Education | $120,000 | $60,000 × 2 children |

| Total Coverage Needed | $1,400,000 | Sum of all components |

This formula gives you a clear starting point. Most online life insurance calculators are too simple. Take the time to run your own numbers or use a detailed calculator that includes all DIME factors.

Adjust for Inflation and Life Changes

The coverage amount you calculate today won’t be the same in 15 or 20 years. I learned to add 2-3% for inflation each year. A $1 million death benefit might seem big now, but inflation will reduce its value over time.

Your coverage should last as long as your biggest financial commitment. For many, this is until the mortgage is paid off or your youngest child goes to college. For example, if you’re 35 with a 5-year-old, a 20-year term would cover until your child is 25.

“The right amount of life insurance coverage provides security without wasting money on unnecessary protection. It’s about precision, not excess.”

I check my life insurance coverage every 3-5 years or after big life events like:

- Having another child

- Buying a bigger home

- Changing jobs or income

- Getting married or divorced

- Taking on a lot of new debt

Each of these events can change how much life insurance your family needs. What seemed enough before having kids might not be enough after.

Remember, your life insurance needs change. The policy should reflect your current financial situation, not what it was years ago. Using these methods ensures your family gets exactly what they need—no more, no less.

“Read more: Why get umbrella insurance coverage at all?

Why Timing Affects Your Life Insurance Costs

Buying life insurance at the right time can save you a lot of money. I learned this the hard way. Waiting two years to buy life insurance cost me $15 more each month because I turned 35 and got a little high blood pressure. This small delay will cost me $3,600 more over 20 years.

Insurance companies look at two main things when setting your premiums: your age and health. Both increase the cost as you get older. This makes buying early very smart.

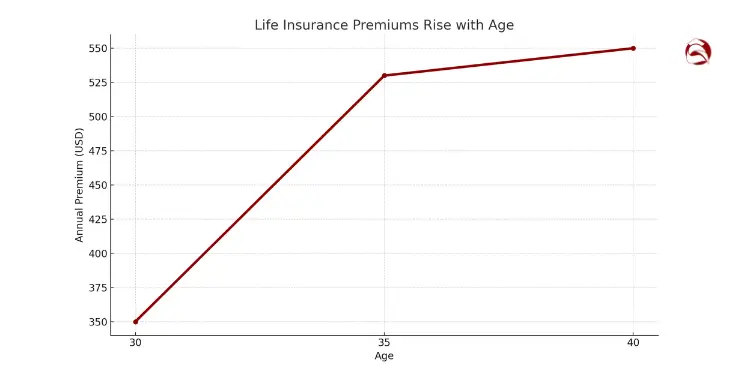

A healthy 30-year-old might pay $350 a year for a 20-year term life insurance policy. But waiting until 40 could make it $550 a year. This $200 difference adds up to $4,000 more over the policy’s life. That’s money you could have kept.

| Age at Purchase | Annual Premium | 20-Year Total Cost | Extra Cost for Waiting |

|---|---|---|---|

| 30 | $350 | $7,000 | $0 |

| 35 | $450 | $9,000 | $2,000 |

| 40 | $550 | $11,000 | $4,000 |

When you buy a life insurance policy, your rate is locked in for the whole term. This is true even if you get sick later. So, buying when you’re healthy is very valuable.

Save More by Buying While You’re Young and Healthy

Your health is more important than your age when insurance companies set your premiums. They use categories like Preferred Plus, Preferred, Standard Plus, and Standard. Each step down means a 20-30% increase in your premium.

The best time to buy life insurance is usually in your late 20s to early 30s. You’re likely healthy then but may be starting to take on big financial responsibilities like getting married or buying a home.

If you’re thinking about starting a family soon, get life insurance now. Pregnancy can make it harder for women to get insurance. Having it before you have kids is important for their protection.

Many people wait to buy life insurance, thinking they’ll get healthier first. But, the chance of getting sick increases with age. The best time to buy life insurance is today.

“The cost of waiting to buy life insurance is one of the most expensive financial mistakes I see families make. A healthy 35-year-old who waits just five years could pay 50% more for the same coverage.”

Even if you’re single now but plan to have kids later, buying insurance early is smart. Your age and health only get worse, and insurance companies charge more for that.

Term life insurance is very affordable for young adults. A healthy 25-year-old might pay less than $20 a month for $500,000 in coverage. This is a small price for a lot of protection that would cost more later.

Life insurance also gives peace of mind for your future family and parents. It can help pay off debts like student loans that wouldn’t go away when you die. The right policy, bought at the right time, brings lasting financial security.

Combine Work Benefits with Personal Life Insurance

Using both your employer’s group life insurance and personal policies makes your family safer. When I first started working, I only had my employer’s $50,000 policy. This was not enough to cover my family’s needs for more than six months.

Most jobs give you basic life insurance for free. It’s usually 1-2 times your salary. But, it’s not enough to cover most families if the main breadwinner dies.

Your employer’s policy is a good start. But, it’s not enough for most families. For example, if you make $60,000 and have a big mortgage and kids, you might need $600,000 in coverage.

“Read also: What is the purpose of mortgage life insurance?“

Identify Gaps in Group Coverage

Don’t think your work policy is enough. Here’s why:

- It’s not portable, so you lose it when you change jobs

- It has coverage caps, like $50,000-$250,000

- You can’t customize it to fit your needs

- It doesn’t grow in value like some personal policies do

To figure out what you need, subtract your employer’s coverage from your total needs. For example, if you need $800,000 and your employer offers $200,000, you need a $600,000 personal policy.

| Coverage Type | Advantages | Limitations | Best For |

|---|---|---|---|

| Employer Group Policy | Free or low-cost, no medical exam | Not portable, limited coverage | Basic foundation coverage |

| Supplemental Group Policy | Convenient payroll deduction, may have guaranteed issue | Often more expensive, tied to employment | Those with health issues |

| Personal Term Policy | Portable, customizable, often cheaper for healthy people | Requires medical underwriting | Long-term core coverage |

Some jobs offer extra coverage you can buy. Always compare these rates with personal policies. An agent can help you choose the best option.

A funeral can cost over $7,500. Without your income, your family might struggle with these costs. A personal policy can help cover these expenses and provide long-term security.

The best plan is to use your employer’s policy and a personal term policy. This way, you have immediate coverage and long-term protection, no matter where you work.

“Most people are significantly underinsured when they rely solely on employer coverage. I recommend clients secure at least 80% of their needed coverage through personal policies they control.”

Update your life insurance beneficiaries after big life changes like getting married or having kids. Your needs will change as your family grows and your finances change. Check your coverage every year to make sure it’s right for you.

Talk to a Licensed Advisor Before You Buy

After looking into life insurance, talking to a financial advisor or insurance agent can help. They make things clearer that websites might not. They explain complex policy details well.

Read More:

Prepare Questions for Licensed Advisors

Before you meet with an advisor, make a list of questions:

- What financial strength ratings does this insurance company have? (Look for A+ or better from AM Best)

- Can I review the actual policy document to check exclusions?

- Which riders might benefit my family’s situation?

- How does the claims process work?

- Why is this specific policy right for my needs?

You can buy life insurance online, through a broker, or directly from companies. Some need medical exams, others just health questions. Look at quotes from at least three places to find the best deal.

Independent brokers work with many companies. They give advice that’s not biased. The goal is to find the right coverage, not the most expensive.

Without life insurance, your family might struggle financially. But with the right advice, life insurance can protect them. Trust your gut and pick coverage that makes you feel secure for your family’s future.

{kind=link}