Trimming your budget is the fastest way to own a home today. When clients ask how to save faster, I tell them the truth. Cutting spending quickly gets you the keys to your new home.

Did you know cutting spending by $500-700 a month can help you save for a down payment 6-8 months faster? This simple math has a big impact.

Warren Buffett said, “Do not save what is left after spending, but spend what is left after saving.” This idea changes how you handle money when getting ready to understand the hidden costs of buying a home.

Over 200 first-time buyers have moved from renting to owning in under 18 months. They did it by using these smart saving tips.

In today’s market, saving for a down payment is key. Starter homes need $15,000-$25,000 down (National Association of REALTORS®, 2023). Saving well is your most important asset.

First-time buyers put down a median 8 % of the purchase price in 2024—the highest share since 1997—confirming that the $15k–$25k target cited above matches national norms. Ref.: “National Association of REALTORS® (2025). Typical Home Buyer’s Annual Household Income Climbed to Record High. NAR.” [!]

Quick hits:

- Eliminate three unnecessary monthly subscriptions

- Refinance high-interest debt immediately

- Automate savings before seeing income

- Track spending with dedicated apps

- Negotiate lower rates on essentials

Slash discretionary spending categories aggressively

Most people have a big chance to save money for a house. By cutting back on things they don’t need, they can save a lot faster. It’s not about giving up things, but about choosing wisely.

Instead of just trying to make more money, cutting costs works faster. Every dollar saved today means more money for your house tomorrow. Let’s look at two big areas where people can save a lot.

Eliminate Unused Subscriptions and Memberships

Today, many people pay for things they don’t use. My clients are often surprised by how much they spend on things they don’t use. Melissa found $127 a month in charges she didn’t need.

This $127 a month is $1,524 a year. It’s enough to cover most of her closing costs. The problem is not one big charge, but many small ones.

Start your audit today with these steps:

- Review your last three bank and credit card statements

- Highlight every recurring charge, no matter how small

- For each subscription, ask: “Would I prefer to have this service or a house sooner?”

- Cancel immediately—don’t fall for retention offers

The balance between managing debt and saving for a down payment gets easier when you cut out unnecessary expenses. Most of my clients find $75-150 a month in savings without feeling a big change in their lifestyle.

Swap Dining Out for Meal Prepping

Dining out is a big expense for many. Eating out costs 4-5 times more than cooking at home. When Michael started meal prepping, he saved $540 a month, adding $6,480 a year to his down payment.

Researchers warn that “time poverty” often derails home-cooking efforts—plan batch-prep sessions and storage strategies to avoid burnout and food waste while still reaping the cost benefits. Ref.: “Tiwari, A. & Drewnowski, A. (2017). Cooking at Home: A Strategy to Comply With U.S. Dietary Guidelines at No Extra Cost. American Journal of Preventive Medicine.” [!]

The goal is not to never eat out, but to eat at home most of the time. Make a meal plan with 10-12 recipes that cost less than $3.50 per serving. This helps avoid the temptation to order takeout.

Successful meal preppers follow this system:

- Shop once weekly with a specific list based on planned meals

- Prep components (chopped vegetables, cooked proteins) on Sundays

- Assemble lunches for the workweek in portable containers

- Allow one strategic restaurant meal weekly as a reward

Saving money on food can help you buy a house faster. Every $10 you save on food is $10 you can use for your down payment.

| Expense Category | Average Monthly Before | Average Monthly After | Annual Savings | Down Payment Impact |

|---|---|---|---|---|

| Subscriptions | $127 | $35 | $1,104 | Covers appraisal and inspection fees |

| Dining Out | $540 | $180 | $4,320 | 1% down on $430,000 home |

| Coffee Shops | $95 | $25 | $840 | Covers title insurance |

| Impulse Shopping | $210 | $75 | $1,620 | Covers moving expenses |

| Total Impact | $972 | $315 | $7,884 | Reaches 20% down payment 18 months faster |

Cutting back on discretionary spending can save you a lot of time. The Federal Reserve Bank of Boston says cutting back by 25% can save you 40% faster. For homebuyers, this means buying a house sooner. Remember, this is a temporary effort for a big reward.

Negotiate recurring bills for better rates

Every month, you pay bills that can be changed to save money. In nine years, I’ve seen people miss out on $150-300 by not asking for better rates. Just 2-3 hours of effort can make a big difference in your savings.

Most bills are not set in stone. They can be changed with a simple ask. Companies expect some people to ask for better deals. If you don’t ask, you miss out on savings. These savings help you reach your home buying cost goals faster.

Shop Insurance Providers and Cable Alternatives

Insurance is a big area to save money. Most people pay too much because they don’t shop around. My client Jessica saved $1,240 a year by getting a better deal.

Start by getting quotes from 3-4 different insurance companies. They all price risks differently. If you find a better deal, call your current company with the new quote.

For cable and internet, call the retention department right away. Use this script:

“I’ve been a loyal customer for [X years], but I’m considering canceling because [competitor] is giving [specific package] for [specific price]. What’s your best rate for me?”

This can save you $35 a month. If not, streaming services are cheaper and just as good.

Don’t forget about student loans. Saving 1% on a $30,000 loan can save you $50 a month. This can help you buy a home faster.

Cell phone plans are also negotiable. With so many options, you can get a better deal. Many people pay for too much data.

The Consumer Financial Protection Bureau says you can save $240-360 a year by negotiating. For a first-time buyer, this means reaching your down payment goal faster.

Keep track of your savings in a spreadsheet. Seeing your progress can keep you motivated. Every dollar saved brings you closer to owning a home.

Read more: How to track home buying expenses during the process

Optimize transportation costs with smarter choices

Your daily commute might be the hidden treasure trove of savings you need to accelerate your path to homeownership. In my nine years helping first-time buyers, I’ve discovered that transportation expenses typically consume 15-20% of household budgets. This makes your travel habits one of the most powerful levers you can pull when you need to save for a down payment.

Think about it: unlike many expenses that feel fixed, transportation offers multiple options for immediate savings. The beauty of transportation adjustments is that they can be implemented quickly and the financial benefits start flowing immediately to your home fund.

Transportation consumes 17 % of the average household budget—second only to housing—making commute changes one of the most powerful levers for accelerating down-payment savings. Ref.: “U.S. Bureau of Labor Statistics (2024). Consumer Expenditures—2023. BLS News Release.” [!]

The money saved on transportation isn’t just expense reduction—it’s a direct investment in your future home equity. Every dollar not spent on depreciation can instead build appreciation.

Carpool, Bike, and Embrace Public Transit

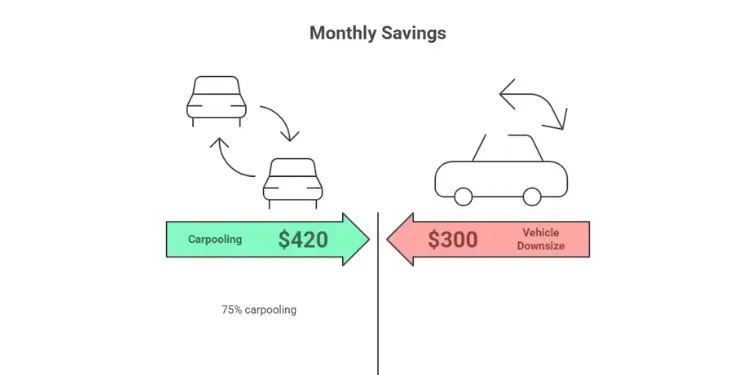

Let me share a quick success story. My client David organized a four-person carpool that cut his solo driving by 75%, saving him $420 monthly. That’s over $5,000 annually redirected straight to his down payment fund!

For urban dwellers, public transit offers substantial savings. When you factor in reduced gas, maintenance, insurance, and parking costs, the average commuter saves $210 monthly by switching from driving to public transportation.

The American Public Transportation Association calculates that a two-person household can save over $10,000 annually by downsizing from two cars to one and using public transit. That’s enough to significantly boost how much home you can afford.

- Carpooling: Find colleagues who live nearby and establish a rotation schedule

- Biking: For distances under 5 miles, consider cycling to save money while improving health

- Public transit: Calculate the true cost comparison (including parking, maintenance, and stress)

- Walking: When possible, walking short distances eliminates transportation costs entirely

Many of my clients initially resist these changes, viewing them as sacrifices. But they often discover unexpected benefits beyond the financial savings—reduced stress, more reading time, and even new friendships formed during carpools.

Read more: How to avoid overspending on house purchase budget

Refinance or Downsize Existing Vehicle Loan

If alternative transportation isn’t feasible in your situation, look at your current vehicle expenses. Auto loan refinancing can yield immediate monthly savings if your credit score has improved.

Current rates may allow you to drop your APR by 2-3 percentage points. On a $25,000 loan, this could free up $50-75 monthly that can go straight toward your dream home fund.

For even more dramatic savings, consider temporary vehicle downsizing. Trading a $35,000 vehicle with a $550 monthly payment for a reliable $15,000 model can free up over $300 monthly while providing dependable transportation.

| Vehicle Strategy | Monthly Savings | Annual Impact | 5-Year Home Fund |

|---|---|---|---|

| Carpooling (75%) | $420 | $5,040 | $25,200 |

| Public Transit Switch | $210 | $2,520 | $12,600 |

| Vehicle Downsize | $300 | $3,600 | $18,000 |

| Loan Refinance (2%) | $60 | $720 | $3,600 |

Remember this: a vehicle typically depreciates while a home generally appreciates. Every dollar diverted from transportation to housing represents a fundamental shift from expense to investment.

Switching from solo driving to public transit saves more than $13,000 per year on average, according to the latest APTA Transit Savings Report—enough to cut months off your home-saving timeline. Ref.: “American Public Transportation Association (2023). Transit Savings Grow as Auto Costs and Gas Prices Increase. APTA.” [!]

When you create a budget for home savings, transportation adjustments offer both immediate and substantial impacts. I’ve seen clients cut their saving timeline by 30% through transportation changes alone.

The temporary adjustments you make today can permanently change your financial trajectory. As you figure out how much home you can afford, don’t overlook the power of rethinking how you get from point A to point B.

Reas also: Essential single income home buying budget strategies

Monetize unused assets for extra income

There’s hidden money in your home that can help you buy a house faster. Many first-time buyers miss out on this chance. By making money from things you don’t use, you can save more for a down payment without spending less on things you love.

Rent out spare room or parking space

That unused bedroom could help you buy a home sooner. In Greenville, I’ve seen rooms make $500-900 a month. This can add $6,000-10,800 a year to your savings.

For example, Sarah rented her second bedroom for 14 months. She made $11,200, almost half her down payment. This way, you can save faster without spending less on other things.

If you don’t have a spare room, think about renting out your parking space. In busy areas, you can make $150-300 a month. I’ve seen clients in downtown areas cover their moving costs with just six months of parking rentals.

Even unused garage or basement space can make $75-150 a month. These amounts add up fast when you’re saving for a home.

Don’t forget about your stuff. Photography gear, tools, or sports equipment can make $100+ a month. These items are already yours, so they can help pay for your home.

This strategy is great because lenders see its value. The FHA lets you count expected rental income when you apply for a mortgage. This means you can afford more home than you think.

There are ways to make money with your house before you own it. Every dollar you make is twice as good as cutting expenses. It’s because you’re adding to your savings, not taking away.

I tell first-time buyers: “Temporary roommates lead to permanent homeownership.” It’s a short-term sacrifice for a big win. When you need to pay closing costs or your first home payment, you’ll be glad for the extra money.

Monetizing assets works with your regular savings. While you save a part of your paycheck, these passive incomes work for you. They can often cover closing costs without touching your main savings.

Read also:

Automate savings and track progress closely

Automation is a key tool in buying a home. It helps you save faster than saving by hand. First-time buyers usually save 15-25% of their income.

First, connect your checking account to a house fund. Set transfers to go out right after payday. This way, you save without thinking about it.

Small savings can add up quickly. Saving $100 less each week means $5,200 more for your down payment each year. It’s a way to save without missing out.

Keep track of your savings each week. Use a spreadsheet or app. Saving $1,000 a month gets you to $50,000 in over 4 years. Saving $1,500 a month cuts that time to under 3 years.

Think about making small changes to save more. Downsizing or finding a roommate can lower your costs. This helps you save faster and get closer to owning a home.

Being consistent is more important than saving a lot at once. Regular savings builds the discipline needed for homeownership. Automate your savings and watch your progress to confidently start looking for a house.

{kind=link}