Compound interest is a powerful tool for growing wealth. It turns small savings into big money over time. Ever wonder why some investors get huge results with just a little money?

In the U.S., 67% of adults don’t get compound growth. This means trillions of dollars are left unclaimed. Warren Buffett said, “My wealth came from America, luck, and compound interest.”

I’ve helped clients for 12 years. I’ve seen how time in the market beats trying to time it. For example, $5,000 a year at 8% grows to $566,416 in 30 years. That’s $416,416 from just compounding.

Having clear financial goals is key to investing well. It helps fund retirement, education, or create income. The basic rules are the same.

Quick hits:

- Start early to maximize growth

- Reinvest earnings for big results

- Consistent contributions beat timing

- Patience makes small sums grow big

Beginning early dramatically magnifies compound growth; SEC investor-education data show that saving and investing in your 20s can more than double ending balances versus waiting until your 40s, even with identical contributions. Ref.: “U.S. Securities and Exchange Commission. (2018). SEC Promotes Investor Awareness During National Financial Capability Month. SEC.gov.” [!]

Comparing Compounding Periods And Growth Pace

Knowing how compounding periods affect your investment’s growth is key. The interest rate is important, but how often it compounds matters a lot. This can make a big difference in how fast your money grows.

Most people look only at the highest interest rates. But, I’ve seen that how often interest compounds can change your outcome a lot. This is true even if the annual interest rate is the same.

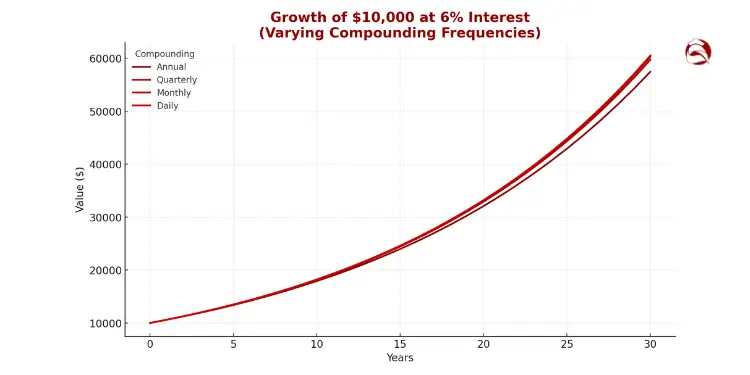

Compounding periods vary a lot. They can be daily, weekly, monthly, quarterly, biannually, or yearly. The more often interest compounds, the faster your money grows.

The Real Impact of Compounding Frequency

Let’s look at an example. If you invest $10,000 at a 6% annual interest rate, you’ll have $10,600 after one year. This is your principal plus 6% interest.

But, if that 6% compounds daily, your balance will be about $10,618. The $18 difference might seem small, but it grows over time. This is because that extra $18 also earns interest.

More-frequent compounding measurably boosts returns: a 1 % savings account compounded daily yields about $5 extra per $1,000 after one year, and the gap widens exponentially over decades. Ref.: “Kopp, C. M. (2024). How Interest Works on a Savings Account. Investopedia.” [!]

After 30 years, the difference between daily and annual compounding on that $10,000 investment is over $7,400. This shows why delaying your investment goals can affect your future a lot.

Compounding Across Financial Products

Different financial products compound interest in different ways. High-yield savings accounts compound daily but credit it monthly. CDs compound daily or monthly, depending on the bank.

Bond investments compound semi-annually. Some investment accounts compound quarterly. Always check the compounding period, not just the interest rate.

A slightly lower interest rate with more frequent compounding can sometimes beat a higher rate with less frequent compounding. This detail is often missed in simple financial comparisons.

| Compounding Frequency | Value After 1 Year | Value After 10 Years | Value After 30 Years | % Increase vs. Annual |

|---|---|---|---|---|

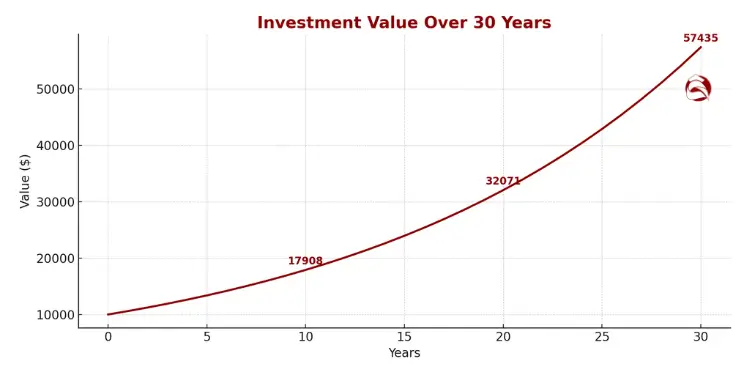

| Annual | $10,600 | $17,908 | $57,435 | Baseline |

| Quarterly | $10,614 | $18,140 | $59,871 | 4.2% |

| Monthly | $10,617 | $18,194 | $60,226 | 4.9% |

| Daily | $10,618 | $18,221 | $60,858 | 6.0% |

CDs quote different compounding schedules, so the only apples-to-apples comparison is the APY—which already folds in frequency; ignoring APY risks selecting a lower true yield despite a higher stated rate. Ref.: “Webber, M. (2024). Do CDs Pay Compound Interest? Investopedia.” [!]

Calculating Your Personal Growth Trajectory

To see how compounding frequency affects you, use a compound interest calculator. These tools let you change variables like principal, interest rate, compounding frequency, and time.

When working with clients, we often compare different scenarios. This shows how small differences in compounding frequency can make a big difference over time. The more often interest compounds, the faster your money grows.

This knowledge is very important for retirement planning. The difference between quarterly and daily compounding can fund an extra year of retirement or leave a big legacy for your heirs.

Optimizing Your Compounding Strategy

To make compound interest work for you, consider these steps:

- When comparing savings accounts or CDs, ask about compounding frequency

- Check your investment statements to see how often interest compounds

- Reinvest dividends automatically for continuous compounding

- Remember, fees and taxes can reduce your compounding frequency

The compounding period is your growth accelerator. The more often, the faster your money grows. While you can’t control market returns, you can choose accounts with better compounding terms.

Understanding these mechanics puts you ahead of most investors. They focus only on interest rates. The real growth comes from the combination of rate, time, and compounding frequency.

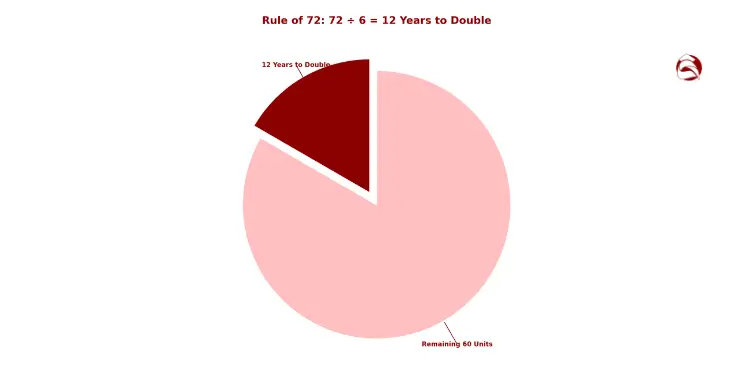

Calculating Returns With Rule Of Seventy Two

Learning the Rule of 72 changes how you see your investment time. It helps you set goals that are real. This simple formula shows the power of compound interest without hard math.

This trick lets you quickly see how long it takes for your money to double. It makes planning your money easier.

The formula is simple. Just divide 72 by your expected return each year. This tells you how many years until your money doubles. For example, a 6% return means your money doubles in 12 years (72 ÷ 6 = 12).

This rule is great because it’s easy to use. You don’t need to do hard math. It works well for most investment returns.

Applying Rule Of 72 Accurately

Using the Rule of 72 is helpful but you need to know its limits. Always use safe return estimates, not the highest ones. The SEC says the stock market has averaged about 10% returns. But, after inflation, a safer guess is 6% to 7%.

For bonds or CDs, the rule is pretty good. But for stocks, use 6-7% instead of 10%. This keeps your money safe from inflation.

The rule assumes steady returns, but the market can change a lot. Early losses can hurt your investment a lot. To plan well, try different scenarios:

- Conservative scenario: 5% return (doubling time: 14.4 years)

- Moderate scenario: 7% return (doubling time: 10.3 years)

- Optimistic scenario: 9% return (doubling time: 8 years)

This way, you see a range of possible outcomes. It helps you get ready for different market situations. The rule is good for starting conversations, not for detailed planning.

“The Rule of 72 isn’t just a mathematical shortcut—it’s a powerful visualization tool that helps investors understand why starting early and staying patient are the cornerstones of successful investing.”

Estimating Doubling Time For Returns

The doubling time shows the power of compound interest. It’s great for explaining investment growth to new investors. Let’s look at simple and compound interest to see the difference.

Simple interest only adds returns to your original amount. A $10,000 investment at 7% simple interest grows $700 each year. It takes 14.3 years to double. But, compound interest doubles it in 10.3 years using the Rule of 72.

As your investment grows, doubling times get shorter. The first doubling from $10,000 to $20,000 takes 10 years at 7% compound interest. The next doubling from $20,000 to $40,000 also takes 10 years. This shows how fast compound interest works.

For real use, make a doubling timeline for your investments. If you’re 35, with $50,000 earning 7% annually, here’s what you might see:

| Age | Portfolio Value | Growth Amount | Planning Implications |

|---|---|---|---|

| 35 | $50,000 | Starting point | Begin consistent contributions |

| 45 | $100,000 | +$50,000 | Review asset allocation |

| 55 | $200,000 | +$100,000 | Consider risk reduction |

| 65 | $400,000 | +$200,000 | Prepare withdrawal strategy |

| 75 | $800,000 | +$400,000 | Legacy planning |

This shows why patience and time are key. The later doublings make more wealth than the early ones. The Rule of 72 makes this clear, showing why short-term ups and downs don’t matter as much as long-term growth.

The rule also shows how inflation can hurt your money. At 3% inflation, your money’s value halves every 24 years. This motivates investors to aim for returns that beat inflation to keep their wealth growing.

When choosing investments, use the Rule of 72 to check if your plan fits your time frame. If you need your money to double in 10 years, you’ll need about 7.2% return. If that’s too high for you, you might need to change your investment plan.

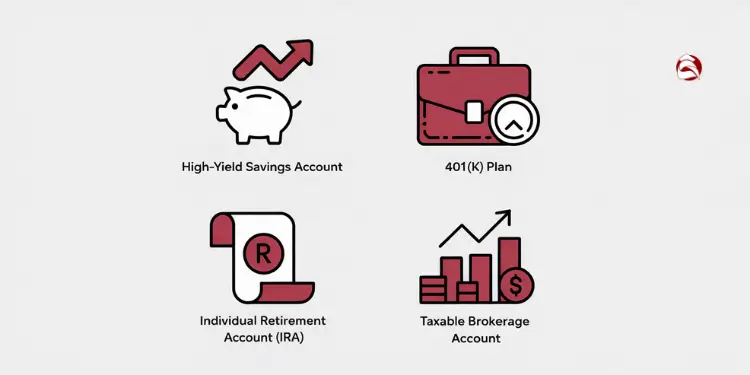

Selecting Accounts That Maximize Compounded Earnings

Your choice of investment accounts is key to growing your wealth. In 12 years of advising, I’ve seen many overlook where to hold their investments. This can cost thousands in lost growth.

The right account structure is like a greenhouse for your money. It helps compound interest grow faster. Let’s look at the best account types for this.

Comparing High Yield Savings Accounts

High-yield savings accounts (HYSAs) are great for short-term goals and emergencies. They offer safety, liquidity, and compound growth. Your money grows daily or monthly, and your principal is protected.

I check HYSA rates weekly. Online banks offer rates from 3.75-4.50% APY. Traditional banks pay less than 0.50%. This difference can add up over time.

When picking HYSAs, look at these four things:

- How often interest compounds (daily compounds faster than monthly)

- Minimum balance needed (some require $10,000+ for top rates)

- Fees (monthly fees can eat into your interest)

- Access rules (some have limits or penalties for withdrawals)

For the best cash management, use a tiered approach. Keep immediate needs in checking. Use an HYSA for 3-6 months of expenses for emergencies. Put funds for short-term goals in higher-yield options if you can.

FDIC insurance covers up to $250,000 per depositor per bank. If you have more than this, spread your money across banks for full protection.

Leveraging Tax Advantaged Retirement Wrappers

Tax-advantaged accounts speed up compounding. After studying hundreds of retirement plans, I found that account structure is more important than investment choice.

401(k)s and IRAs offer tax deductions and tax-deferred growth. This means you get more money to compound from the start. For example, a $6,000 contribution costs only $4,500 if you’re in the 25% tax bracket.

Roth accounts are funded with after-tax dollars but offer tax-free growth and withdrawals. They’re great if you expect higher taxes later or are young with lots of time to grow your money.

IRA earnings grow tax-deferred (or tax-free in a Roth), allowing 100 % of returns to compound without yearly drag—an advantage explicitly affirmed in IRS Publication 590-A. Ref.: “Internal Revenue Service. (2025). Publication 590-A: Contributions to Individual Retirement Arrangements. IRS.gov.” [!]

For the best compounding, prioritize these accounts:

- Employer-matched 401(k) contributions (immediate 50-100% return)

- Health Savings Accounts (HSAs) if eligible (triple tax advantage)

- Roth/Traditional IRA (based on current/future tax situation)

- Unmatched 401(k) contributions

- Taxable brokerage accounts

Self-employed investors should look into SEP IRAs, Solo 401(k)s, or SIMPLE IRAs. These offer higher contribution limits than standard IRAs, boosting your compounding.

Evaluating Low Cost Index Fund Options

Low-cost index funds are great for compound growth. Small fee differences can make a big difference over time.

For example, a $10,000 investment growing at 8% annually in a fund with a 0.05% expense ratio reaches about $99,000 after 30 years. The same investment in a fund with a 1% expense ratio grows to just $76,000—a $23,000 difference from fees alone.

When choosing index funds, focus on these:

- Expense ratio (aim for under 0.10% for U.S. large-cap exposure)

- Tracking error (how closely the fund follows its benchmark)

- Fund size/liquidity (larger funds have tighter spreads)

- Tax efficiency (ETFs are better for taxable accounts)

For core holdings, consider total market funds. They offer broad diversification in one vehicle. Vanguard’s VTI, Fidelity’s FSKAX, and Schwab’s SCHB are good options with low costs.

Remember, index funds don’t eliminate market risk. Your investment will move with the market.

| Account Type | Compounding Advantage | Best For | Typical Annual Return | Liquidity |

|---|---|---|---|---|

| High-Yield Savings | Daily/monthly compounding, FDIC insured | Emergency funds, short-term goals | 3.75-4.50% | High (immediate access) |

| Traditional 401(k)/IRA | Tax-deferred growth, larger initial principal | Long-term retirement, current high tax bracket | 7-10% (market-based) | Low (penalties before 59½) |

| Roth 401(k)/IRA | Tax-free growth and withdrawals | Long-term growth, future higher tax brackets | 7-10% (market-based) | Medium (contributions accessible) |

| Taxable Brokerage | Full flexibility, no contribution limits | Mid-term goals, income generation | 5-8% (after-tax) | High (no restrictions) |

| HSA (Health Savings) | Triple tax advantage | Medical expenses, supplemental retirement | 7-10% (market-based) | Medium (tax-free for medical) |

The account structure you choose is key to successful compounding. By using high-yield savings for short-term needs, tax-advantaged accounts for retirement, and low-cost index funds, you create the best environment for compound interest.

Remember, compounding works best when left alone. Accounts with penalties or restrictions help keep you from interrupting the growth process.

Aligning Contribution Schedule With Investment Horizon

Your investment’s growth depends on matching your contribution schedule with your time frame. Over 12 years, I’ve seen how timing is as important as how much you invest. Compound interest works best when your contributions match your cash flow and goals.

Linking investment goal time horizon and contribution frequency boosts wealth over time. For example, monthly $500 contributions grow more than a single $6,000 annual payment. This is because early money compounds longer, leading to more growth.

Different time frames need different contribution plans:

| Time Horizon | Optimal Contribution Approach | Account Types | Risk Tolerance | Contribution Frequency |

|---|---|---|---|---|

| Short-term (1-3 years) | Lump-sum when possible | High-yield savings, CDs, short-term bonds | Conservative (low risk of loss) | Front-loaded or consistent |

| Mid-term (5-15 years) | Regular consistent contributions | Balanced funds, moderate allocation | Moderate (some fluctuation acceptable) | Monthly or bi-weekly |

| Long-term (20+ years) | Dollar-cost averaging | Tax-advantaged retirement accounts | Aggressive (higher risk for higher returns) | Every paycheck |

| Variable income | Base + sweep strategy | Mix based on goals | Varies with goal | Base monthly + additional when income rises |

For long-term goals over 10 years, regular contributions reduce timing risk. Dollar-cost averaging creates a disciplined savings habit. It averages your purchase prices through market cycles, helping investors during volatile times.

“The most powerful force in the universe is compound interest. The most powerful force in investing is consistent contributions aligned with your time horizon.”

When setting your contribution schedule, consider these factors:

- For retirement (20+ years): Maximize tax-advantaged accounts first, with aggressive early contributions

- For mid-term goals (5-15 years): Balance between tax-advantaged and taxable accounts with moderate, consistent contributions

- For short-term goals (1-5 years): Focus on preservation and liquidity with conservative vehicles

Your contribution schedule should also account for income variability. Commission-based or seasonal income might warrant larger, less frequent contributions. Salary-based income supports consistent monthly additions. The relationship between asset allocation and investment time becomes important when planning your contribution strategy.

Remember, consistency is key. In my experience, $200 monthly without fail outperforms sporadic larger contributions. This consistency creates a psychological advantage while maximizing compound interest’s benefits.

For a simplified explanation of investment goals tailored for newcomers, check out Investment Goals Explained in Simple Terms for Beginners.

Coordinating Paycheck Contributions For Consistency

Automating contributions from your paycheck creates a compounding engine that runs without constant decision-making. This “set and forget” approach removes emotion from the equation and keeps your investment plan on track.

The psychological advantage is significant—money you never see in your checking account doesn’t trigger spending temptations. This mental accounting trick has helped hundreds of my clients maintain discipline through both bull and bear markets.

For employer-sponsored retirement plans, determine your optimal contribution percentage by working backward from your retirement goal. If you need $2 million by age 65, calculate the required monthly contribution based on your current age and expected return rate. At minimum, contribute enough to capture any employer match—this represents an immediate 50-100% return before compound interest even begins its work.

For contributions outside employer plans, establish automatic transfers timed to your pay schedule. Most brokerages and banks allow you to set up recurring investments on specific dates. Consider these practical approaches:

- Split your direct deposit, with a portion going directly to investment accounts

- Schedule automatic transfers 1-2 days after your regular payday

- Set up automatic investment purchases on a fixed monthly schedule

- Implement automatic increases of 1% annually to painlessly boost contributions

For variable income earners, establish a base contribution rate for your minimum expected income, then implement a “sweep” strategy. This approach maintains consistency while capturing upside during higher-income periods. Simply transfer a predetermined percentage of any income above your baseline to investments.

The future interest your investments generate depends heavily on maintaining this contribution consistency. When contributions align perfectly with your investment horizon, compound interest works at maximum efficiency, creating a powerful wealth-building engine that grows stronger with each passing year.

If you’re looking to structure your investment aspirations effectively, the Free Investment Goal Setting Worksheet for Beginners can be an invaluable tool.

Mitigating Taxes Fees Impact On Compounding

Taxes and fees are the real enemies of compound interest. They slowly take away your returns every year. I’ve looked at thousands of investment statements. Small costs of 1-2% can cut your portfolio by 20-30% over decades.

When taxes and fees cut into your interest, compounding works against you. This makes the gap between what you earn and what you keep bigger. Many investors don’t see this until it’s too late.

The most powerful force in the universe is compound interest. The most destructive force in investing is compounding costs.

To keep your money growing, use a strong defense strategy. This will help your investments grow more.

Leveraging Tax-Advantaged Accounts

Start by using tax-advantaged accounts. These accounts let your money grow without taxes until you take it out. IRAs and 401(k)s are good examples. Roth accounts even let your money grow tax-free forever.

For education goals, 529 plans are great. They grow tax-free for qualified expenses. This uninterrupted growth is very powerful.

Scrutinizing Investment Expenses

Look at all costs affecting your investments:

- Transaction costs: Use platforms without trading fees to save money.

- Account maintenance fees: Ask your broker to waive these fees with a simple call.

- Advisory fees: Make sure the cost is worth it for professional help. Extra 0.25% in fees hurts over time.

- Fund expense ratios: Choose funds with costs under 0.20%. A small difference in costs adds up a lot.

Implementing Tax-Loss Harvesting

In taxable accounts, tax-loss harvesting can help. It can add 0.2-0.4% in returns each year. This is a big boost over time.

This method involves selling losing investments to offset gains. But, wait 30 days before buying similar securities to avoid tax rules.

Strategic Asset Location

Not all investments belong in the same account. Put tax-inefficient investments in tax-advantaged accounts. This way, you won’t pay taxes on distributions. Keep tax-efficient investments in taxable accounts.

This strategy helps keep more of your returns for compounding. It doesn’t change your overall investment mix. The benefits grow as your portfolio does.

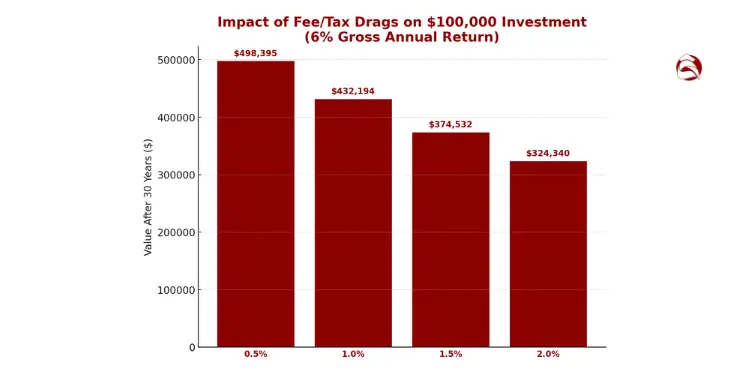

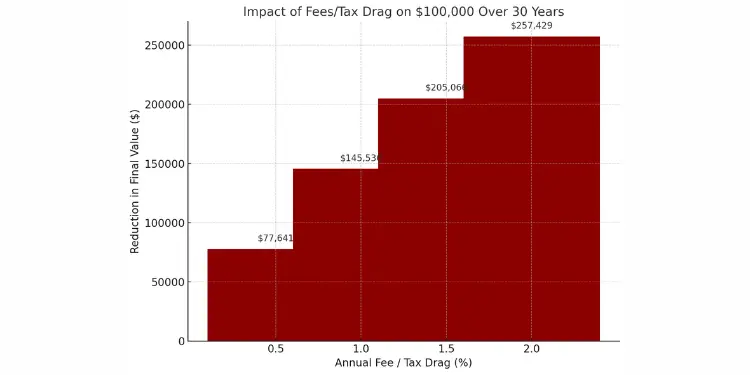

| Annual Fee/Tax Drag | 30-Year Impact on $100,000 | Reduction in Final Value | Recommended Defense |

|---|---|---|---|

| 0.5% | -$77,641 | -14% | Use low-cost index ETFs |

| 1.0% | -$145,536 | -26% | Maximize tax-advantaged accounts |

| 1.5% | -$205,066 | -37% | Implement tax-loss harvesting |

| 2.0% | -$257,429 | -46% | Strategic asset location |

The table shows how important it is to reduce costs. It assumes a 7% return before fees and taxes. The difference in outcomes is huge.

No strategy can guarantee profits or protect against losses. But, by reducing taxes and fees, you keep more money growing. This is the power of compound interest.

Investors who focus on costs outperform those who ignore them. The math is clear: small differences in costs add up to big differences in wealth.

For a deeper understanding: Understanding Compound Interest for Your Investment Goals.

Automating Growth Through Dividend Reinvestment Plans

Dividend reinvestment plans (DRIPs) help your investments grow. When you join a DRIP, your dividends buy more shares. These new shares then earn their own dividends.

Morningstar’s long-term study shows reinvested dividends supplied roughly 40 % of the S&P 500’s total return from 1930 to 2021, underscoring the importance of DRIPs for maximum equity compounding. Ref.: “Metrou, G. (2023). For Dividend Investors, Time Pays. Morningstar.” [!]

Studies show that reinvested dividends add 40-60% to your returns over time. At a 5-6% annual rate, your money doubles in 12-14 years. This is thanks to the power of compounding.

Most brokerages let you reinvest dividends for free. But, remember, reinvested dividends are taxed in taxable accounts. In tax-advantaged accounts, you don’t pay taxes. This means your money grows faster.

Read More:

Tracking Reinvested Distributions Performance Regularly

It’s important to check how your investments are doing. Do this every quarter. Look at how reinvested dividends and interest are helping your money grow.

Watch these important numbers:

1. Dividend growth rate – companies that raise their payouts help your money grow faster

2. Yield on original cost – shows how your returns increase as dividends grow

3. Number of shares acquired through reinvestment – shows how much your investment has grown

To get the best results, balance the current yield with the chance for dividend growth. Even though compound interest takes time, sticking to your reinvestment plan makes your portfolio grow a lot over time.

{kind=link}