Common investment goals for beginners turn vague money dreams into clear plans. When you set investment goals, you make a roadmap for all your money choices. Ever wonder why some new investors do well, while others struggle, even with the same income?

A 2024 survey by Bankrate found 22% of people regret not saving for retirement early. This shows why planning your finances early is key.

“Goals-based investing aims to meet specific goals, not just follow the market,” I tell new clients. Helping hundreds of first-time investors, I’ve seen how clear goals help make better choices.

Knowing your financial goals makes your journey easier. Each goal has a role in your wealth, from safety nets to growth engines.

Quick hits:

- Emergency funds prevent debt cycles

- Home down payments need specific timelines

- Retirement planning rewards early starters

- Education funding grows through consistency

- Short-term goals build investing confidence

Emergency fund accumulation benchmark amount

Your emergency fund is like a shield for your money. It keeps your long-term investments safe from surprises. This emergency fund is not for making money. It’s your safety net against big problems.

I suggest starting with three months of your basic needs. This is about $12,000-15,000 for most families. It helps you deal with emergencies without hurting your big plans.

When you figure out how much you need, just think about the basics. This includes your home, food, and car costs. You won’t need extra money for fun stuff when things get tough.

Targeting Three Months Essential Expenses

For most families, three months is enough. But if you’re single or your job is unstable, you might need six months. Your situation is different, so your fund should match.

Where should you keep this money? It should be easy to get to when you need it. High-yield savings and money market funds are good choices.

Now, saving for emergencies is more rewarding than before. You can get 4-5% interest without losing quick access to your money.

Certified Financial Planner professionals advise keeping 3 – 6 months of essential outlays in a dedicated emergency fund, giving households a time-tested buffer against income shocks and surprise costs. Ref.: “CFP Board. (2025). Emergency Fund. Let’s Make a Plan.” [!]

Don’t try to make more money with your emergency fund. Its main job is to be safe and easy to get to. Once it’s full, you can start thinking about your next big investment goal.

| Emergency Fund Option | Current Yield Range | Access Speed | Best For | Considerations |

|---|---|---|---|---|

| High-Yield Savings Account | 4.0-5.0% | 1-2 business days | Most emergency situations | May require minimum balance to avoid fees |

| Money Market Fund | 4.5-5.2% | 1-3 business days | Slightly higher yields | Not FDIC insured, though historically stable |

| Cash Management Account | 3.8-4.5% | Immediate (with debit card) | Fastest access needs | May offer fewer features than dedicated accounts |

| Traditional Savings Account | 0.01-0.25% | Immediate (with transfer) | Convenience of local banking | Significantly lower returns erode purchasing power |

| Certificate of Deposit | 4.5-5.5% | Delayed (early withdrawal penalties) | Portion of larger emergency funds | Early access incurs penalties; best for tiered approach |

Your emergency fund is the first line of defense for your money. It lets your other investments stay safe during tough times. Build this safety net first. Then, you can focus on growing your money with less worry.

Top high-yield savings accounts now pay up to 4.44 % APY—about seven times the 0.6 % national average—so parking cash in legacy savings can cost hundreds in forgone interest every year. Ref.: “Goldberg, M. (2025). Best High-Yield Savings Accounts of June 2025. Bankrate.” [!]

Saving for upcoming large purchase

Big purchases need smart saving plans. These plans should fit your time frame and how much risk you can take. Whether it’s a house or a new car, you need a special plan for each goal.

When saving for the middle term, finding the right balance is key. You want growth but also safety as your goal gets closer. That’s why I suggest special accounts for each big purchase.

The money for these goals should follow a simple rule. The closer you are to needing it, the safer it should be. This way, you reach your goals without taking too much risk.

Down Payment Goal for Property

For a house, aim to save 20% of the price. This avoids extra monthly costs without adding to your debt. With homes costing around $400,000, you’ll need about $80,000.

This big goal takes 3-5 years to save for. Choose investments that match this time frame. For 3-5 years, a mix of 60% bonds and 40% stocks is good. As you get closer, switch to 80% bonds and 20% stocks to keep your savings safe.

Don’t keep your down payment in a low-yield account for years. Setting a goal with the right investments can speed up your savings without too much risk.

“Explore More: How to Make 50/30/20 Budget with Clear Practical Step by Step“

Vehicle Replacement Fund Within Timeline

Buying a car is different but needs a similar plan. Aim for at least 50% down to save on costs. For a $35,000 car every 7-10 years, save $300-400 monthly in a special account.

The return needed for a car fund is less than for a house. But the rule is the same: match your investment to your timeline. For a car in 2-3 years, choose a mix of short-term bonds and no more than 30% stocks.

Automate your savings to keep making progress. I’ve seen clients who save automatically are three times more likely to reach their goal than those who save whatever’s left at the end of the month.

| Purchase Type | Target Amount | Typical Timeline | Recommended Allocation | Monthly Savings (Example) |

|---|---|---|---|---|

| Home Down Payment | 20% of purchase price | 3-5 years | 60% bonds/40% equities | $1,300-$2,200 for $80K goal |

| Vehicle Purchase | 50-100% of vehicle cost | 2-7 years | 70% bonds/30% equities | $300-$400 for $17.5K goal |

| Major Renovation | 100% of project cost | 1-3 years | 80% bonds/20% equities | $550-$850 for $20K goal |

There are many ways to invest for these goals. For short times, high-yield savings are good. But for longer goals, bonds, ETFs, and some stocks are better.

Keep these funds separate from your emergency and retirement money. This way, you won’t use your long-term investments for quick buys. Each goal gets the right amount of risk.

The key to financial success is simple, consistent actions. Not complicated strategies.

By planning for big purchases, you build a pattern of success. Each goal you reach boosts your confidence and skills for bigger challenges ahead.

“Related Articles: Examples of Common Investment Goals for Beginners“

Building retirement seed capital early

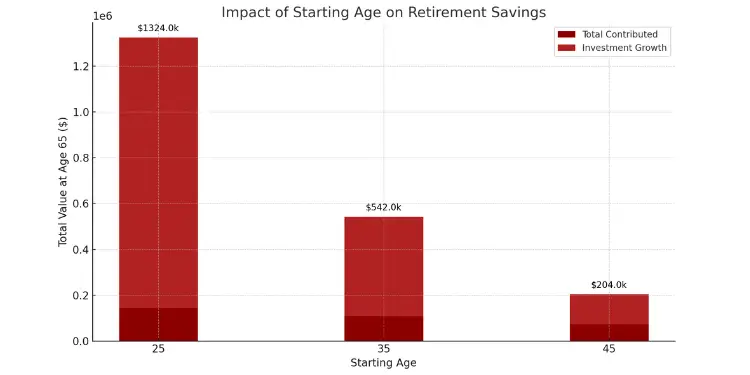

Starting to save for retirement in your twenties is very important. It can make a big difference in how much money you have later. I’ve seen that starting at 25 can lead to 2-3 times more wealth than starting at 35, even with the same amount of money.

Compounding is key here. It means your money grows faster over time. Think of it like planting seeds that grow into big trees with time.

For those new to saving for retirement, don’t miss out on employer matches. These can double your money right away. Many people miss this chance, leaving free money behind.

Try to save 15% of your income for retirement, including any employer matches. If that seems too much, start with 6-10% and add 1% each year. This way, you can slowly get used to saving more.

| Starting Age | Monthly Investment | Value at Age 65 | Total Contributed | Investment Growth |

|---|---|---|---|---|

| 25 | $300 | $1,324,000 | $144,000 | $1,180,000 |

| 35 | $300 | $542,000 | $108,000 | $434,000 |

| 45 | $300 | $204,000 | $72,000 | $132,000 |

When you’re saving for retirement, you can take more risks. If you have 25+ years to go, you can put 80-90% of your money in stocks. This way, you can handle market ups and downs and get better returns over time.

Don’t wait for the perfect time to start saving. Even $100 a month in a basic stock fund can add up over time. I’ve seen people wait too long, missing out on early growth.

The best time to plant a tree was twenty years ago. The second best time is now.

Retirement investing is about being in the market for as long as you can. Studies show that trying to time the market usually doesn’t work. It’s better to keep investing regularly.

Make saving automatic by setting up automatic transfers from your paycheck. This way, you won’t have to think about it, and you’ll keep saving.

For beginners, start with simple, low-cost funds. As you learn more, you can try more complex options. This way, you can grow your savings over time.

Starting to save early is not just about money. It’s about freedom and options for the future. Every dollar you save now means more choices later, like early retirement or pursuing your dreams.

“For More Information: 50/30/20 vs 80/20 Rule Detailed Comparison Guide“

Funding future continuing education costs

Funding education costs is a big goal for families and career people. It’s different from other financial goals on your investing journey. It’s about planning for your kids’ college or your own learning.

Education costs are a big challenge because they come at a set time and cost more each year. Unlike retirement, you can’t delay education expenses. A college degree now costs $100,000 to $200,000 at public schools.

Parents should start saving early for their kids’ education. The 529 plan is the best way to do this. It offers tax breaks that help your money grow faster.

Earnings in 529 plans compound tax-deferred, and qualified withdrawals for tuition, fees, and even computers are federally tax-free, making them one of the most efficient tools for college saving. Ref.: “Internal Revenue Service. (2025). 529 Plans: Questions and Answers. IRS.” [!]

To save for 50-75% of college costs, you might need to save $250-500 each month from birth. This might seem like a lot. But remember, you only have 18 years to save for college, not 30-40 years for retirement.

If you’re saving for your own education, have a separate account. This way, you won’t use your retirement money for school. Aim to save 3-5% of your income for school funds. This can help you advance in your career.

Education funding needs a special plan that changes as college gets closer. Unlike retirement, you can’t keep growing your money too close to college time.

| Time Until Enrollment | Equity Allocation | Fixed Income Allocation | Cash Equivalent | Key Strategy Focus |

|---|---|---|---|---|

| 15+ years | 80-90% | 10-20% | 0% | Maximum growth |

| 10-15 years | 60-70% | 30-40% | 0% | Growth with moderate protection |

| 5-10 years | 40-50% | 50-60% | 0-5% | Balanced growth and protection |

| 1-5 years | 20-30% | 60-70% | 10-20% | Capital preservation with modest growth |

| Less than 1 year | 0-10% | 30-40% | 50-70% | Maximum capital preservation |

Success in education funding comes from being consistent. Set up automatic monthly savings. This helps your money grow faster and avoids emotional decisions.

Consistently contributing the IRA maximum from age 25 instead of 35 can more than double your nest egg by 70, thanks to four extra decades of compound growth. Ref.: “Fidelity Investments. (2025). Continuous Contributions and Compounding. Fidelity.” [!]

When choosing a 529 plan, don’t just look at your state’s plan. Some plans offer better investments or lower fees. Your financial situation is unique, so compare total returns, not just tax benefits.

For your own education, consider using taxable accounts or Roth IRAs. These options are more flexible if your plans change or if new opportunities come up.

Grants, scholarships, and employer help can lower what you need to save. But don’t rely on them alone. Plan as if you won’t get this help.

Education funding is very rewarding. It’s about investing in your kids’ future or your own career. Use the same careful strategy for this goal as you do for other parts of your portfolio. This way, you’ll create opportunities that last a long time.

“You Might Also Like: How to Prioritize Multiple Investment Goals as a Beginner“

Preparing capital for entrepreneurial ventures

Starting a business needs smart money planning. It’s different from saving for retirement or school. I’ve helped many move from being an employee to a business owner. The right money plan can help your business survive.

Most small businesses start with $50,000 to $100,000. This is true across many fields. But, don’t forget to save 6-12 months of living expenses for yourself too. This makes getting money for your business very hard.

Business money planning is different from saving for retirement. Retirement money grows over time. But, business money needs to be easy to use and grow a bit. You need to balance these needs without losing either.

“Read More: How Investment Goals Influence Portfolio Strategy for Beginners“

Setting Timeline for Business Launch

Planning when to start your business is key. Most people need 3-5 years to save enough. This time lets you save carefully and avoid taking too much risk.

Business money is different from retirement money. It needs to be easy to use and grow a little. I suggest a 60% fixed income and 40% equity in a brokerage account. As you get closer to starting, move to 80% fixed income and 20% equity to keep your money safe.

Setting clear money goals helps you stay on track. For example, aim to save $25,000 by a certain date, then $50,000 by another. This makes your goal feel real and achievable.

Remember, business money is risky. Don’t mix it with your retirement or emergency funds. Having enough money to start also helps you make smart early decisions.

I recommend saving 6-12 months of living expenses in a separate fund. This fund should be just for you and not for your business. It gives you peace of mind when your business is new and unpredictable.

| Capital Milestone | Timeline (Years) | Recommended Asset Allocation | Purpose |

|---|---|---|---|

| Initial $10,000 | Year 1 | 60% Fixed Income / 40% Equity | Concept Development |

| $25,000 | Year 2 | 60% Fixed Income / 40% Equity | Market Research & Planning |

| $50,000 | Year 3 | 70% Fixed Income / 30% Equity | Initial Setup & Equipment |

| $75,000+ | Year 4-5 | 80% Fixed Income / 20% Equity | Launch Capital & Operating Expenses |

| Personal Survival Fund | Parallel to Business Capital | 100% High-Yield Savings | 6-12 Months Personal Expenses |

Structuring goal hierarchy for clarity

Many investors try to reach many goals at once without a plan. This doesn’t work well. Only 65% of those with plans do better than those without. But, 70% who make plans don’t stick to them.

Your success in investing depends on a clear goal plan. Here’s how:

Tier 1: Foundational Security – Save three months’ worth of expenses. Pay off high-interest debt. Make sure to get your employer’s retirement match.

Tier 2: Essential Future Needs – Save six months’ worth of expenses. Put 15% into retirement. Also, save for education costs.

Tier 3: Aspirational Objectives – Buy property. Start a business. Aim for early retirement.

Don’t try to fund many goals at once. Each goal should be clear and reachable. Use SMART criteria: Specific, Measurable, Achievable, Realistic, and Time-based.

Read also:

- “Related Topics: Saving vs Investing for Financial Goals Explained“

- “Further Reading: How to Adjust Investment Goals Over Time“

Write down your goals on a one-page plan. Set dollar targets and timelines. Setting financial goals before investing helps you see what your money is for.

Choose the right accounts for your goals. Use high-yield savings for short-term goals. Tax-advantaged accounts are best for long-term goals.

Check your investment plan every quarter. Those who review yearly reach their goals 40% faster. Your plan should match your personal values, not just advice.

{kind=link}