Millions of Americans fall behind on retirement savings every year. If your investment portfolio isn’t where it should be, making smart changes can help. Did you know nearly one-third of Americans nearing retirement have no savings at all?

Recent surveys show 29% of adults 55 and older have no retirement savings. Another 15% have less than $10,000 saved. These numbers highlight a big problem that needs quick action.

“The best time to start saving was twenty years ago. The second best time is today,” says old financial wisdom. This advice is true for those needing to speed up their retirement planning.

In my twelve years helping investors, I’ve seen big changes when they use targeted retirement catch-up strategies. Even those starting late can build big savings with careful planning.

Quick hits:

- Assess your current financial position honestly

- Maximize tax-advantaged account contributions immediately

- Adjust asset allocation for appropriate growth

- Consider delaying retirement by 2-3 years

- Develop additional income streams strategically

Measure Current Savings Against Target

To close your retirement savings gap, first measure how wide it is. This step helps you plan your next moves. Without knowing the gap, your efforts won’t be focused.

Calculate your retirement number by multiplying your yearly expenses by 25. For example, if you need $60,000 a year, you’ll need $1.5 million. This assumes a 4% withdrawal rate for a steady income in retirement.

But, adjust this number based on your life. If you expect big healthcare costs or lots of travel, you might need more. If you’ll have less housing costs or pension income, you might need less.

Then, compare your current savings to age-based benchmarks. These milestones help you see if you’re on track:

| Age | Target Savings (Multiple of Annual Income) | Example at $100,000 Income | Key Action if Behind |

|---|---|---|---|

| 30 | 1x | $100,000 | Increase savings rate by 2-3% |

| 40 | 3x | $300,000 | Boost contributions by 5-7% |

| 50 | 6x | $600,000 | Maximize catch-up contributions |

| 60 | 8x | $800,000 | Consider delaying retirement age |

Don’t worry if you’re behind these benchmarks. Knowing the gap is the first step. It lets you take the right actions.

Make a simple spreadsheet to track your savings. It should have four columns:

- Current retirement savings (total across all accounts)

- Target savings based on your age and income

- The shortfall (the difference between target and current savings)

- Monthly savings needed to close the gap by your target retirement age

When checking your savings, include all accounts. This means 401(k)s, IRAs, and HSAs. Also, include any taxable investments for retirement. This gives a full picture of your savings.

If you’re 50 or older, you can save a lot more. The limits and catch-up contributions vary by account type. For 2025, you can save up to $39,000 annually if you’re 50+ with both an IRA and a 401(k). This doubles if you’re married and both qualify.

VERIFIED SOLUTION:

IRS Notice 2024-73 confirms 2025 limits of $23,500 for 401(k)s (plus a $7,500 catch-up) and $7,000 for IRAs (plus a $1,000 catch-up), enabling savers aged 50+ to shelter up to $31,000 per year tax-deferred. Ref.: “Internal Revenue Service. (2024). 401(k) Limit Increases to $23,500 for 2025, IRA Limit Remains $7,000. IRS News Release IR-2024-197.” [!]

When setting your savings goal, think about your retirement age. You don’t have to retire at 65. Changing your retirement age can greatly affect how much you need to save. Working longer means more time to save and fewer years to fund your savings.

After assessing your savings, figure out how much more you need to save. This amount will guide your future strategies.

“Further Reading:

Boost Savings Rate With Budget Adjustments

When your retirement savings are low, look at your budget first. It’s often easier to save more by spending less. This way, you don’t need to make more money.

Increasing your savings rate by 5% can fill a $100,000 gap in 10 years. Many people double their retirement savings by cutting spending. It’s about knowing where your money goes.

Start by tracking your spending for 30 days. You might spend 20% more than you think. Use a spreadsheet or app to see your true spending.

After tracking, find big savings areas:

- Housing: Downsizing can save hundreds monthly. It also cuts maintenance and utility costs.

- Transportation: Keeping your car longer saves money. Each year without a car payment adds $4,000-$6,000 to your retirement.

- Food: Plan meals to save $200-400 monthly. This cuts down on restaurant visits and grocery waste.

Then, decide where to put your savings. Tax-advantaged accounts grow your money the most:

- Workplace retirement plans with matching contributions (free money)

- Health Savings Accounts (HSAs) if eligible (triple tax advantage)

- Traditional or Roth IRAs (tax-deferred or tax-free growth)

Put your savings into a “catch-up” account. This account gets money automatically on payday. It helps your savings grow without tempting you to spend it.

Cut Discretionary Spending Sustainably Now

Successful retirement plans focus on lasting changes. Quick cuts don’t work for long. Make lifestyle changes you can keep for years.

Start by canceling unused subscriptions. Americans spend $273 monthly on services they don’t use. Use this money for retirement instead. Cutting $100 monthly in subscriptions saves $1,200 a year for retirement.

C+R Research’s 2024 nationwide survey shows consumers underestimate subscription costs by 266% and pay an average of $273 per month—redirecting just half of this amount could add more than $100,000 to a 10-year catch-up plan. Ref.: “C+R Research. (2024). Subscription Service Statistics and Costs.” [!]

“The most successful retirement savers aren’t those who make dramatic short-term sacrifices. They’re the ones who make modest, sustainable changes they can maintain for decades.”

Next, find cheaper ways to enjoy things. Coffee lovers might buy a home brewer instead of daily coffee. Travelers might choose domestic trips until they catch up on savings.

Pay off high-interest debt first. It’s better to earn 8% on investments than pay 18% interest on credit cards. Use your trimmed budget to pay off debt before saving more for retirement.

Use a “24-hour rule” for big purchases. This helps you decide if you really need something. Look for ways to save money by timing purchases, negotiating, or buying used.

Make sure your family agrees with budget cuts. Involve your spouse or partner in setting goals. Celebrate your progress together. This makes budgeting a team effort toward your future.

Now, put your savings into better investments. In the next section, we’ll talk about how to grow your retirement faster.

Tilt Portfolio Toward Higher Growth Assets

For investors who are behind on their financial goals, changing your portfolio can help. You might need to add more growth assets to reach your investment goals. This is because your current mix might not be enough to catch up.

I’ve helped many clients in Phoenix with this issue over 12 years. The solution is to make smart changes to your investment mix. This is not about taking big risks, but about making informed choices.

Age-based formulas might not work when you’re trying to catch up. Your portfolio should match your catch-up plan and risk level, not just your age.

Increase Equity Allocation Responsibly Today

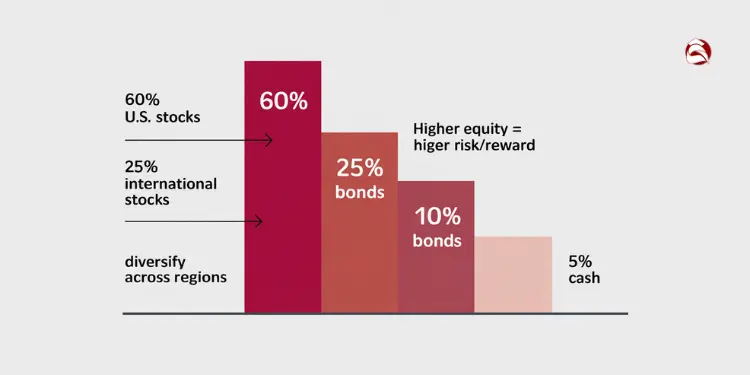

When you need to move faster, I suggest adding more stocks. For example, a 55-year-old might go from 45% stocks to 55-60%. This is more than the usual age-based rule.

Morningstar finds that small-cap value and emerging-market equities outperformed broad indexes by roughly 2 percentage points a year from 2008-2023—but endured two drawdowns greater than 30% in the same period, highlighting the need to match higher-growth tilts with sufficient risk capacity. Ref.: “Johnson, B. (2023). It’s Too Soon to Say the Value Premium Is Dead. Morningstar.” [!]

Make these changes slowly over 6-12 months. This method helps avoid big risks and makes it easier to adjust.

Here are some ways to grow your investments:

- Invest in small-cap value stocks for better long-term growth

- Add international stocks, like those in emerging markets, for higher growth

- Put money in sectors like healthcare, tech, and consumer goods for strong growth

But don’t forget to keep some money safe. Have 3-5 years’ worth of living expenses in stable assets. This way, you can grow your investments while keeping your money safe.

“Related Topics: Setting Financial Goals Before Investing Matters for Success“

Utilize Factor Funds For Upside

Factor investing is another way to grow your money. It focuses on specific traits that research shows lead to better returns.

Three key factors have shown strong evidence of long-term success:

- Value: Buying companies that are cheaper than they should be

- Momentum: Investing in stocks that are going up in price

- Quality: Choosing companies with strong finances and steady earnings

Extensive research by Fama & French demonstrates that portfolios tilted toward value, momentum, and quality factors earned 1.5–3 percentage-point excess annual returns versus cap-weighted benchmarks across 1963-2023 datasets. Ref.: “Fama, E. F. & French, K. R. (2015). A Five-Factor Asset Pricing Model. Journal of Financial Economics.” [!]

Factor funds and ETFs can help you get these benefits. They offer a way to diversify and possibly earn more than regular index funds.

Which factor works best can change with the market. Value does well when the economy is recovering. Quality is better in uncertain times. So, using a mix of factors is usually best.

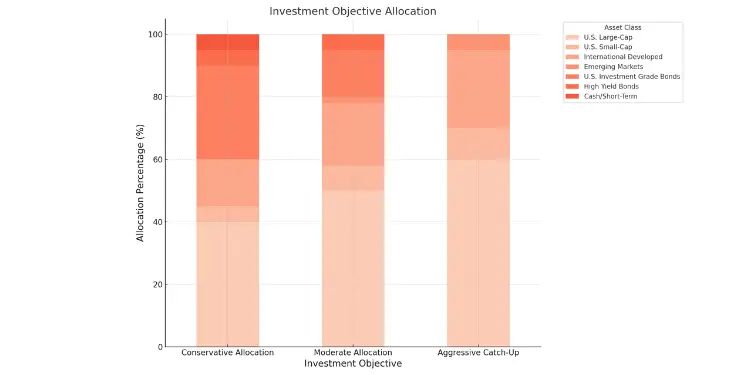

| Investment Objective | Conservative Allocation | Moderate Allocation | Aggressive Catch-Up |

|---|---|---|---|

| U.S. Large-Cap | 40% | 50% | 60% |

| U.S. Small-Cap | 5% | 8% | 10% |

| International Developed | 15% | 20% | 25% |

| Emerging Markets | 0% | 2% | 5% |

| U.S. Investment Grade Bonds | 30% | 15% | 0% |

| High Yield Bonds | 5% | 5% | 0% |

| Cash/Short-Term | 5% | 0% | 0% |

Your investment plan should be tailored to you. The aggressive catch-up plan might work for someone with a stable job, low debt, and 7-10 years before needing the money. Your mix should match your catch-up goals and risk level.

After optimizing your portfolio for growth, the next step is to increase the money going into these investments. We’ll discuss how to do this next.

“Read More: Saving vs Investing for Financial Goals Explained“

Maximize Allowed Catch Up Contributions

Catch-up contributions are a big help for those 50 and older. They let you save more for retirement. This is great because you earn more and spend less on family when you’re older.

In 2025, you can save a lot. For 401(k)s, you can put in $23,500 plus an extra $7,500 if you’re 50+. That’s $31,000 total. IRAs let you save $7,000 plus $1,000 more if you’re 50+, for $8,000 a year.

Those 60-63 can save even more. You can add $11,250 to employer plans. This is a big chance to grow your wealth.

| Account Type | Standard Limit (2025) | Catch-Up Amount | Total Limit Age 50+ |

|---|---|---|---|

| 401(k)/403(b) | $23,500 | $7,500 | $31,000 |

| IRA (Traditional/Roth) | $7,000 | $1,000 | $8,000 |

| 401(k) (Ages 60-63) | $23,500 | $11,250 | $34,750 |

To make the most of these limits, do three things right away:

- Adjust payroll deductions now – Even mid-year changes can significantly impact your annual savings. Don’t wait until January to increase your contributions.

- Schedule automatic annual increases – Set up 1-2% contribution increases each year to painlessly boost your savings rate over time.

- Redirect raises and bonuses – Commit to directing all compensation increases to retirement accounts before lifestyle inflation absorbs these funds.

Using catch-up contributions wisely can really add up. By age 65, you could have $250,000 more in your retirement account. This extra money can make a big difference in your retirement.

I’ve seen many people change their retirement plans by using catch-up contributions smartly. One person started saving $300,000 at 50 but saved over $1.2 million by 65. They used catch-up contributions and made smart investment choices.

“Explore More: How to Avoid Overspending on House Purchase Budget“

Schedule Income Deferral Into Retirement

Creating a plan to save more for retirement is important. First, figure out how much you need to save from each paycheck. Most people should save at least 20-25% of their income.

If saving too much is hard, start small. Increase your savings by 2% every three months. This way, your budget can adjust slowly while you save more for retirement.

Business owners and self-employed people have even more options. They can set up a Solo 401(k). This lets you save as an employer and employee, saving over $70,000 a year. This is a big tax benefit that helps you save faster.

“The most effective retirement catch-up strategy I’ve implemented combines maximizing catch-up contributions with strategic tax planning. This approach not only builds retirement assets faster but often reduces current tax burdens as well.”

Remember, saving more is just the first step. You also need to find ways to make more money now. This will help you save more and keep earning in retirement.

Create Supplemental Income Through Side Hustles

Starting a side hustle can help you save money for retirement. It’s better than trying to save every penny. Even $1,000 a month can add $120,000 to your savings in 10 years.

If you’re 50 and just starting to save, you can save up to $39,000 a year. Saving this way for 10 years can grow your savings to about $590,000 by age 60. This is a big start in a short time.

The best side hustles use your skills. Consulting can make $75-150 an hour. This is more than general gig work. It helps you save now and earn later.

Here are some good side hustles based on your skills:

- Industry-specific consulting – Offer your expertise to smaller companies or startups for 5-10 hours weekly

- Knowledge monetization – Create online courses or write guides based on your professional skills

- Real estate investments – Purchase rental properties that generate both income and appreciation

- Skilled freelancing – Provide specialized services in writing, design, or data analysis

- Part-time professional work – Leverage your credentials in a flexible position within your field

Put all your side hustle money into retirement accounts. If you can, use Roth accounts for their tax benefits. This can add $1,000-3,000 a month to your savings.

“The most effective retirement catch-up strategy combines aggressive saving with strategic income expansion. Your expertise is often your most valuable and underutilized asset.”

Choose a side hustle that fits your skills, time, and growth goals. A consulting business can grow to replace your main income. But driving for rideshare services might not grow as much.

Side hustles are great with other retirement plans. Social Security and 401(k)s are good, but side hustles add tax benefits. This mix helps you reach your retirement goals faster.

You might need to change your plan based on your age. If you’re older, choose side hustles that last long. If you’re younger, pick ones that grow faster. The goal is to get to retirement faster with more money.

Monitor Trajectory And Revise Aggressiveness

Fixing your retirement plan isn’t a one-time thing. You need to keep watching and change things often. I suggest checking your progress every three months and doing a big check-up once a year.

Make a simple chart to track three important things:

1. Savings rate as a percent of your income (try for 20-30% during catch-up)

2. How fast your investments are growing compared to your goals

3. How much you’ve closed the gap (shortfall reduction)

By 65, you’ll have big choices to make. Will you work longer? Change your lifestyle? Or take more risks with your retirement plan?

“For More Information:

Change your plan when it makes sense. In good times, lock in gains by moving some money to safer places. In bad times, stay strong and maybe take more risks if you can.

The best catch-up plans treat the gap as a project, not a fear. Setting clear goals makes market moves mean something. It shows how you’re getting closer to your savings goals.

Being steady is better than making big changes. Closing the gap might take 5-10 years of hard work. But with regular checks and smart changes, you’ll get there.

{kind=link}