To figure out how much you need for an investment goal, you need the right formulas. You can’t just guess. You need to know how much time, returns, and risks will affect your money. Did you know inflation can cut your goal by up to 50% in 20 years?

Recent data from the Federal Reserve shows 68% of Americans think they need less for retirement than they really do. Warren Buffett said, “Someone’s sitting in the shade today because someone planted a tree a long time ago.”

I’ve seen many Phoenix investors change their fortunes by using the right math. Over 12 years, I’ve helped clients reach their goals with precise calculations. Those who didn’t use math well often didn’t meet their goals.

Your investment plan starts with knowing the formulas that work. It’s not about using random online tools. It’s about learning the math that pros use every day.

Quick hits:

- Future value adjusts for inflation

- Compound interest dramatically changes outcomes

- Time horizon affects required contributions

- Risk tolerance determines return assumptions

- Regular recalculation prevents goal drift

Specify Target Amount Timeline And Priority

Setting clear investment goals with specific timelines is key. It separates successful investors from those who just hope for good returns. In my 12 years helping clients, I’ve seen that being precise is important.

Start by writing down your target amount in today’s dollars. Be exact to the thousand. For example, say “$1.2 million for retirement living expenses” instead of “I need money for retirement.”

Next, pick a fixed end date for your timeline. Use “December 2035” instead of “in about 10-15 years.” This helps you figure out how much you need and how much to save each month.

Fidelity suggests saving at least 1x your salary by age 30, 3x by 40, and so on. But, these are just starting points. You need to adjust them based on your own situation.

Fidelity’s age-based milestones call for saving at least 1× salary by 30, 3× by 40, 6× by 50, 8× by 60, and 10× by retirement at 67—use them as progress checkpoints. Ref.: “Fidelity Investments. (2025). How Much Do I Need to Retire? Fidelity Viewpoints.” [!]

“The difference between a dream and a goal is a deadline and a dollar amount. Without both, you’re simply hoping.”

Then, sort your goals by importance. Label them as essential or discretionary. This helps you decide how much to save and how fast.

Clarify Essential Versus Discretionary Costs

Essential goals are things you can’t do without, like housing and education. You need to plan carefully for these.

Discretionary goals, like vacation homes, are important but not as urgent. You can adjust these if needed without risking your safety.

For essential goals, add a “non-negotiable buffer” of 15-20% above your base plan. This isn’t too cautious; it’s smart.

| Goal Type | Examples | Buffer Requirement | Investment Approach |

|---|---|---|---|

| Essential | Retirement, Housing, Education | 15-20% above target | Conservative, prioritize capital preservation |

| Discretionary | Vacation home, Luxury travel | 5-10% above target | Moderate risk tolerance acceptable |

| Legacy | Inheritance, Charitable gifts | 10-15% above target | Balanced approach, longer time horizon |

When setting financial goals before investing, write down why you chose each goal. This helps you stay focused when the market gets shaky.

Account For Emergency Buffer Requirements

Also, keep an emergency fund for 6-12 months of expenses. This fund protects you from selling investments when prices are low.

For retirement, build a “sequence risk shield” with 1-2 years of liquid assets. This way, you won’t have to sell investments during downturns.

Your emergency fund needs will depend on:

- Income stability (contract work requires larger buffers than tenured positions)

- Family health considerations

- Housing stability (homeowners face different emergency needs than renters)

- Career field volatility

Maintaining a cash reserve covering roughly two years of expenses can help retirees avoid selling assets during early-retirement downturns, mitigating sequence-of-returns risk. Ref.: “Wu, E. & Cui, B. (2025). Beyond Sequencing Risk: Dynamic Withdrawals for Retirement. T. Rowe Price.” [!]

Calculate your monthly essential expenses and multiply by your buffer factor (6-12 months). Keep this money in high-yield savings or short-term Treasuries, separate from your investments.

Before moving on, make sure you’ve documented your target amount, timeline, and priority with buffers. This solid foundation makes your future calculations more accurate and meaningful.

Project Future Cost Including Inflation

Inflation is like a sneaky thief that takes away your money’s value. Over 12 years, I’ve seen many retirement plans fail because of this. It’s because people didn’t think about inflation when they planned.

When you dream of saving $100,000, it won’t buy as much when you need it. This mistake makes your plan fall short every year.

Inflation is as violent as a mugger, as frightening as an armed robber, and as deadly as a hit man.

To figure out your future costs, use this simple formula:

Future Value = Present Value × (1 + inflation rate)^years

For example, a $50,000 home renovation in 10 years will cost $64,004 with a 2.5% inflation rate. So, you need to save $64,004, not $50,000.

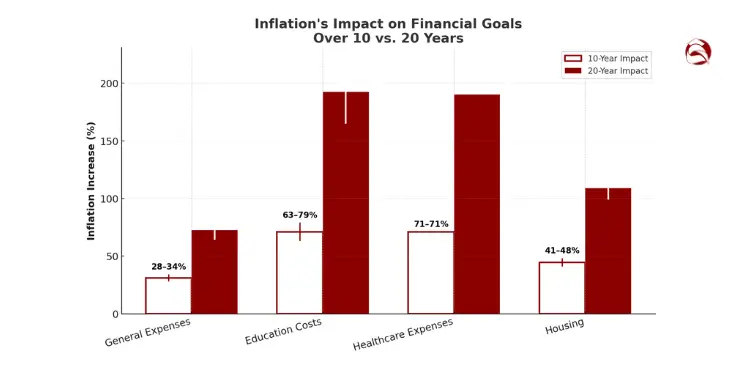

Different things cost more over time, so the Consumer Price Index (CPI) isn’t perfect for planning. I suggest these inflation rates for different goals:

| Expense Category | Recommended Inflation Rate | 10-Year Impact | 20-Year Impact |

|---|---|---|---|

| General Expenses | 2.5-3.0% | 28-34% increase | 64-81% increase |

| Education Costs | 5.0-6.0% | 63-79% increase | 165-220% increase |

| Healthcare Expenses | 5.5% | 71% increase | 190% increase |

| Housing | 3.5-4.0% | 41-48% increase | 99-119% increase |

For long-term plans, use 2.5-3% as your inflation rate. It’s a bit higher than the Federal Reserve’s goal but lower than recent high rates.

College costs are very high and go up fast. Use 5-6% for these costs. Parents are often shocked to see how much college costs will rise in 10 years.

Healthcare costs in retirement also go up a lot. Use 5.5% for these costs. This can change how much you need for retirement a lot.

Don’t use general inflation calculators for planning. They use broad CPI measures that don’t fit your specific needs. Your investments might grow before taxes, but inflation will take away those gains if you don’t plan for it.

While you can’t predict future returns, inflation’s effect is sure. Even small inflation adds up over time. It can turn today’s savings into tomorrow’s shortage.

After figuring out your future costs, write down the real amount you need. This amount, not your original plan, is what your investments must reach. This adjustment can increase your savings by 25-50% for long-term goals. It gives you a realistic plan for success.

Choose Realistic Expected Return Estimates

Investment success often depends on realistic return estimates. As a financial advisor, I’ve seen many plans fail because of too-high return hopes. These hopes never came true.

Your expected return is key to your investment plans. If you guess too high by 2%, you could miss out on hundreds of thousands of dollars. Guess too low, and you might save too much or wait too long for important goals.

A 2024 global survey shows investors anticipate 12.8 % real returns, while advisors peg a more feasible 8.3 %—highlighting the need to temper assumptions to avoid shortfalls. Ref.: “Natixis Investment Managers. (2024). 2024 Global Survey of Financial Advisors—Executive Summary. Natixis Investment Managers.” [!]

Many investors make a big mistake. They use old returns without thinking about today’s market or their mix of investments. This can lead to big mistakes.

For bonds and CDs, I suggest using the current yield minus 0.5%. This helps account for risks like defaults and the chance to reinvest. For example, if a CD offers 4.5%, a safer plan might be 4%.

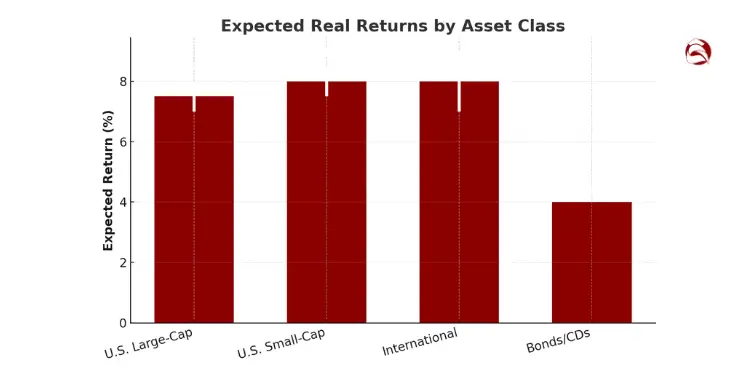

For stocks, think about these safer estimates:

- U.S. large-cap stocks: 7-8% (lower than the usual 10%)

- U.S. small-cap stocks: 7.5-8.5% (less than the usual 12%)

- International stocks: 7-9% (considering risks like currency and politics)

“The biggest investment mistake isn’t picking the wrong stock—it’s using unrealistic return assumptions that make your financial plan look solid when it’s actually built on quicksand.”

Reference Historical Index Averages Carefully

Don’t just look at point-to-point returns. They can be very misleading. Instead, check rolling period returns. Look at all 20-year periods, not just 2000-2020.

This method gives a clearer view of possible outcomes. It shows not just average returns but the range of outcomes you might see.

| Investment Type | Often-Quoted Historical Return | More Realistic Forward Projection | Adjustment Reason |

|---|---|---|---|

| S&P 500 Index | 10-11% | 7-8% | Current valuations, slower growth expectations |

| Corporate Bonds | 5-6% | Current yield minus 0.5% | Default risk, reinvestment risk |

| 60/40 Portfolio | 8-9% | 6-7% | Blended lower expectations, plus costs |

Your actual return depends on your investments. Many people forget to adjust for their mix of investments. A mix of 60% stocks and 40% bonds won’t give 100% stock returns.

Calculate your expected return based on your mix. For example, if you expect 7.5% from stocks and 4% from bonds in a 60/40 mix:

(7.5% × 0.6) + (4% × 0.4) = 6.1%

Then subtract 0.5-1% for costs and mistakes. This includes fees, trading costs, and the chance to make timing mistakes.

Investments with higher returns often come with more risk. Using high return hopes to save less can lead to big adjustments later. A safer estimate can give you a buffer and nice surprises if returns are better than expected.

Remember, the returns shown in ads are ideal. They assume no withdrawals, perfect timing, and no mistakes. Your results will likely be different, making safer estimates key.

“For More Information: Long Term Investment Goals Examples for Beginners”

Calculate Required Principal And Contributions

Every investment plan starts with figuring out how much money you need. This includes both the first amount and the ongoing contributions. After setting your goals and thinking about inflation, you can turn these plans into real steps.

Investors use a goal calculator to plan. There are two main formulas. Knowing both helps you reach your goals in different ways.

The Lump-Sum Formula

If you can invest a lot at once, this formula shows what you need today:

- Required Principal = Future Value ÷ (1 + r)^t

- Where r = expected annual return (decimal)

- Where t = time horizon in years

This formula shows how compound interest helps your money grow over time. The longer you invest, the less you need at the start.

“Explore More: How to Set Realistic Investment Goals Successfully”

The Periodic Contribution Formula

Most people grow their wealth by adding money regularly. This formula is different:

- Future Value = PMT × ((1 + r)^t – 1) ÷ r

- Solving for PMT: PMT = Future Value × r ÷ ((1 + r)^t – 1)

- Where PMT = your periodic payment amount

A good savings goal calculator does these math problems for you. But knowing the math helps you check the results and make changes with confidence.

“The best investment strategy isn’t always about finding higher returns—it’s often about starting earlier and being consistent with contributions.”

Let’s look at an example. For a $500,000 goal in 20 years with 6% returns, you might need:

| Approach | Amount | Advantage |

|---|---|---|

| Lump-Sum Investment | $166,792 | Simplicity, maximum compound growth |

| Monthly Contributions | $1,115 | More accessible, dollar-cost averaging |

| Combined Approach | Varies | Flexibility, balanced commitment |

I’ve made many plans for clients. The math shows a key truth: adding 1-2% more to your income early can save you 5-10% later.

When using any type of investment calculator, watch the frequency settings. Adding money monthly to a savings account grows differently than adding it quarterly to a brokerage account.

Think about if you’ll add more money over time. Many people match their contribution increases with their salary growth. This makes their money grow faster.

Write down how much you need to start and how much to add regularly. Don’t just accept what the calculator says. Change the numbers to fit your own situation and investment goals.

Remember, the growth of your investment isn’t just about returns. It’s also about when you invest. Early money works harder than money invested later. This is a key idea to keep in mind when planning.

Adjust For Taxes Fees And Volatility

Perfect markets don’t exist in real life. To make a good investment plan, we must think about taxes, fees, and market ups and downs. We’ve talked about ideal scenarios before. But in real life, these factors can really cut down your earnings if you don’t plan for them.

Incorporate Marginal Tax Rate Assumptions

Your tax rate affects how much your investments grow in taxable accounts. When figuring out after-tax returns, remember both your federal and state tax rates.

For taxable accounts, cut your expected return by your tax rate on investment income. If you expect a 7% return and pay 25% in taxes, your after-tax return is only 5.25%. This is a big drop over time.

State taxes can be deducted on your federal return in many cases. When figuring out your total tax rate, remember this to avoid overestimating your taxes. Here’s a simple way to do it:

- Find your federal marginal tax rate based on your income.

- Figure out your state income tax rate.

- If you itemize deductions, adjust the state rate by the federal rate.

- Add the adjusted rates together for your total effective rate.

For tax-advantaged accounts like 401(k)s and IRAs, you can use your full expected return during the growth phase. But don’t forget to consider taxes when you withdraw money in retirement based on your tax bracket then.

Many investors don’t realize how much taxes affect their long-term earnings. Estimating your federal tax rate now and in retirement gives a clearer picture of what you’ll have to spend.

“Read More: How to Adjust Investment Goals Over Time”

Add Safety Margin Against Downturns

Markets rarely give average returns in one year. Your investment journey might start in a bull market or a tough downturn. Adding a safety margin to your plans is key.

I suggest a “stress test” for important goals: see how your plan does if returns are 2% less for the first five years. This simulates starting in a tough market.

For big financial goals, think about increasing your contribution rate by 10-15% above what you’ve calculated. This creates a safety net against the risk of poor early returns damaging your long-term success.

| Safety Margin Type | Implementation Method | Best For | Impact on Required Savings |

|---|---|---|---|

| Conservative Return Estimate | Reduce expected return by 1-2% | Essential goals | Increases by 15-30% |

| Contribution Buffer | Save 10-15% above calculated amount | Medium-term goals | Increases by 10-15% |

| Time Extension | Add 1-2 years to timeline | Flexible goals | Minimal increase |

Don’t forget about investment fees when figuring out your returns. Even low-cost index funds charge 0.03-0.15%. Actively managed funds can cost 0.5-1.5%. Add another 0.25-0.5% for advisory fees if you have them.

Sales charges and other fees can really cut down your returns over time. A small 1% annual fee difference can mean about 20% less money after 20 years. When picking investments, look closely at all expense ratios, transaction costs, and account fees.

Our savings plan assumes saving 15% of income from age 25 (including employer match), investing more than 50% in stocks, retiring at 67, and keeping the same lifestyle. Your situation might be different, so you might need to adjust these assumptions.

For most investors, I recommend this simple approach: calculate your needed savings rate with reasonable returns, then add a 10% buffer. This simple step adds a lot of protection against taxes, fees, and market ups and downs without making your goal seem too hard.

Map Contribution Schedule To Pay Periods

Now we connect the dots between planning and action. Even the best plans fail without action. Start by matching your contribution schedule with your pay cycle. This simple step helps you track progress toward your investment goals easily.

Automatic enrollment with a 6 % default contribution rate drives plan participation to 82 % and supports the 12–15 % total savings rate most experts recommend. Ref.: “Greig, F., Hahn, K., & Tan, F. (2024). Job Transitions Slow Retirement Savings. Vanguard Research.” [!]

For those paid monthly, invest every month. If you get paid biweekly, invest every two weeks. This way, you avoid missing payments and stay on track.

“Related Topics:

Automate Transfers For Behavioral Advantage

Automation turns good plans into real results. Set up direct deposits to your investment accounts before they reach your checking. My clients who automate save 12-15% more than those who don’t.

Freelancers and those with variable income, start with a base contribution rate. Then, invest a fixed percentage of any extra income.

Remember, stable investments are safer but may not grow as much. Riskier investments could grow more but are riskier. Choose wisely based on your goals.

Check your progress every quarter to make small changes. The best beginners treat investing like a must-do, like paying rent. This approach makes investing real and effective.

{kind=link}