Can you buy a house on low income today? Yes, you can. Even with high prices, there are ways to own a home. You might be closer than you think.

The national median home price is now $419,200. This is a big jump from early 2020. But, there are special mortgage options for those with moderate incomes.

“Homeownership isn’t just for the rich,” I tell my clients. “It’s about finding the right options.”

In Greenville, I’ve helped many families buy homes, even with low incomes. It takes knowing about special financing strategies. Most people don’t find these on their own.

Quick hits:

- Down payments as low as 3%

- Income-based assistance programs available nationwide

- Credit requirements more flexible than advertised

- Payment assistance for qualifying applicants

- Specialized loans for various occupations

Improve Credit Profile Before Application

Improving your credit score is key to owning a home on a budget. A better score means lower interest rates and smaller monthly payments. Spend at least 30 days improving your credit before you apply for a loan.

FICO updates can lag one full billing cycle; rapid-score gains in 30 days are uncommon unless major balances are paid down immediately. Ref.: “Fair Isaac Corporation. (2022). What Should My Credit Utilization Ratio Be? myFICO Blog.” [!]

Most loans need a score of 620 or higher. FHA loans might accept scores as low as 580. But, if your score is 500 or higher, you might need to pay more upfront.

Dispute Errors on Credit Report

Get your free credit reports from annualcreditreport.com. This is the only place where you can get free reports from all three major bureaus. About 20% of first-time buyers find errors that hurt their score.

An FTC follow-up study found roughly one in five consumers disputed report errors that, once corrected, raised their credit tier. Ref.: “Federal Trade Commission. (2015). FTC Issues Follow-Up Study on Credit Report Accuracy. Federal Trade Commission.” [!]

Check your reports for unknown accounts, wrong payment histories, or old negative info. Even small mistakes can harm your score.

If you find errors, write a dispute letter to each bureau. Include proof like payment confirmations. The bureaus must fix errors within 30 days. One client’s score went up by 28 points after fixing a mistake.

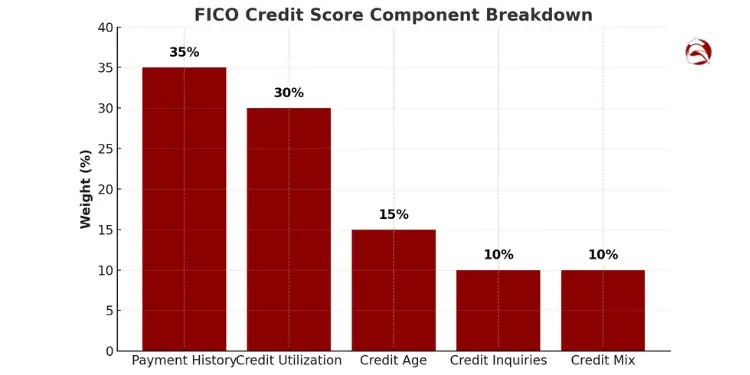

Lower Utilization Through Strategic Payments

Credit utilization is a big part of your score. Try to use less than 30% of your credit. Using less than 10% can improve your score by 15-25 points fast.

Pay your credit cards twice a month instead of once. This keeps your utilization lower. It’s a smart way to boost your score.

Keeping utilization below 10 %—by splitting payments—can add 15-25 points to many borrowers’ FICO® scores within two reporting cycles. Ref.: “Experian. (2023). How Long Will High Credit Utilization Hurt My Credit Score? Experian.” [!]

Focus on paying off cards that are almost full first. This can improve your score by 42 points in 60 days. One family saved $87 a month on their mortgage with this strategy.

Avoid new credit inquiries and big purchases. Each inquiry can lower your score by 5-10 points. New accounts also hurt your average account age.

Improving your credit score can save you thousands. The Department of Housing and Urban Development offers free counseling. It includes tips on improving your credit for low-income buyers.

HUD-approved housing counselors provide no-cost credit and budgeting guidance, assisting over one million households annually. Ref.: “U.S. Department of Housing and Urban Development. (2025). Housing Counseling Program Overview. HUD.” [!]

Explore Government Backed Mortgage Programs

When it’s hard to get a loan, government-backed mortgage programs can help. I’ve helped many first-time buyers in Greenville find homes. These programs open doors to homeownership that wouldn’t be possible without them.

These loans have big benefits. They need less money down, are easier on credit, and have good interest rates. This makes it easier to buy a home, even if you don’t make much money.

I’ve helped many clients find the right program for them. Each one has its own benefits. Let’s look at which one might be best for you.

Balance your housing needs and desires within your budget by consulting Balancing needs vs wants home buying on a budget.

Review FHA USDA VA Eligibility Criteria

FHA loans are popular among my clients with low incomes. They need only 3.5% down with a credit score of 580 or higher. If your score is between 500-579, you’ll need 10% down.

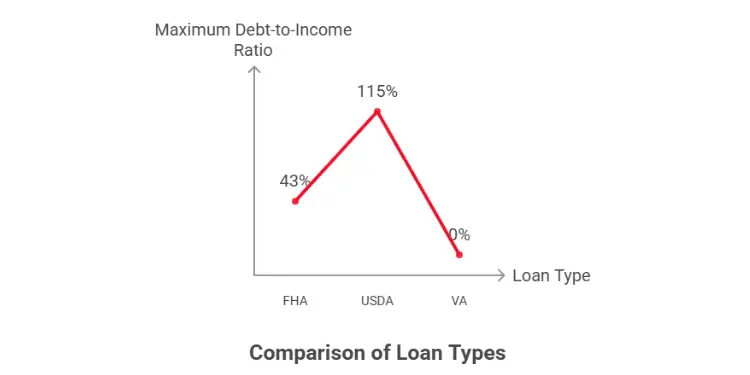

FHA loans are flexible with debt-to-income ratios. They usually cap at 43%. But, I’ve helped clients with ratios up to 50% get approved. This is because they have other good factors like steady jobs or savings.

| Loan Type | Minimum Credit Score | Down Payment | Income Requirements | Special Considerations |

|---|---|---|---|---|

| FHA | 580 (3.5% down) 500 (10% down) | 3.5-10% | No specific limits | Mortgage insurance required |

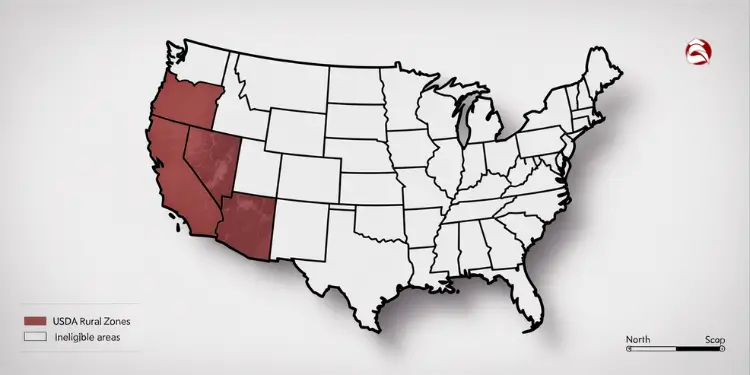

| USDA | 640 typically | 0% | ≤115% of area median income | Property must be in eligible rural area |

| VA | 620-640 typically | 0% in most cases | No specific limits | Military service requirement |

USDA loans are great for rural buyers. They offer 100% financing, meaning no down payment. But, you must buy in a rural area and your income can’t be too high.

USDA Guaranteed Loans limit applicant income to ≤ 115 % of the area’s median household income. Ref.: “U.S. Department of Agriculture. (2025). Single Family Housing Guaranteed Loan Program Income Limits. USDA Rural Development.” [!]

I helped a family buy their first home with a USDA loan. They thought it was years away. Their mortgage payment is now less than their rent.

VA loans are the best for military members. They offer no down payment, no mortgage insurance, and good interest rates. Most lenders want a credit score of 620-640, but it’s not required by VA.

“Government-backed loans aren’t charity—they’re smart economic policy. When more Americans can afford homes, communities stabilize and grow stronger.”

When planning your budget, remember to include mortgage insurance premiums and funding fees. These can add a lot to your monthly payment.

FHA loans carry both an upfront and an annual Mortgage Insurance Premium (MIP) that can last for 11 years—or the life of the loan—depending on LTV, adding to monthly costs. Ref.: “Investopedia Staff. (2015). Do FHA Loans Require Escrow Accounts? Investopedia.” [!]

It’s smart to talk to at least three lenders who specialize in government-backed loans. Get pre-approved for all programs you might qualify for. This gives you more options when looking for a home and helps you compare costs.

These programs can approve buyers with high debt-to-income ratios. This means more people can own homes, even with low incomes. The key is finding the right program for your situation.

Don’t worry about income limits or credit scores. I’ve seen buyers with low scores get loans with the right preparation. It’s often about fixing specific credit issues, not just waiting for a better score.

Leverage Down Payment Assistance Grants

For many, down payment grants make owning a home possible. In nine years, I’ve seen many stop at this hurdle. But, over 2,000 programs nationwide offer help.

These programs give $5,000-$10,000 to help with costs. A kindergarten teacher got $8,500 to buy a $165,000 condo.

Where to Find Down Payment Help

Look for help in these places:

- State Housing Finance Agencies – Every state has programs for first-time buyers. You need to take a homebuyer education class.

- Local Government Programs – Many cities and counties help in certain areas to revitalize neighborhoods.

- National Initiatives – Federal programs offer big benefits for those who qualify.

Programs like HomeReady and Home Possible need only 3% down. You can use grants and gifts for your down payment.

Master budgeting techniques suitable for various income levels with 50/30/20 budget basics for first time budgeters.

Profession-Based Assistance Programs

Some jobs qualify for special help. The Good Neighbor Next Door program gives teachers and others a 50% discount. It’s a Federal Housing Administration program that requires a three-year stay.

Many employers, like hospitals and universities, help with down payments. A nurse used her hospital’s $10,000 program to buy a home.

“I never thought I could afford a house on my salary. The down payment assistance program not only made it possible but also covered most of my hidden costs of buying a house. I’m paying less monthly for my mortgage than I was for rent.”

Qualifying for Assistance Programs

Most programs need these things:

- You must buy a primary residence, not an investment.

- You need to finish a 4-8 hour homebuyer education class.

- You must meet minimum income standards, usually 80% of the area’s median income.

- Your credit score must be high enough, but it’s often easier than other loans.

Don’t worry if you’ve owned a home before. Many programs let you qualify if you haven’t owned in three years.

When you apply, have your income, assets, debts, and tax returns ready. Programs have limited funds, so apply quickly. Contact your state’s housing finance agency to find out what you qualify for.

Freddie Mac’s DPA One database lists many programs. Start there, then look for local options. Some clients use more than one program to get the most help.

Some programs give you a tax credit instead of cash. The Mortgage Credit Certificate (MCC) program gives up to $2,000 a year. This can help you buy more home.

With the right help, buying a home with a low income is possible. Just know where to look and act fast.

Consider the financial implications of your home choice in Starter home vs forever home budget considerations.

Partner with Co Borrower or Guarantor

Adding a co-borrower to your mortgage can help you buy your first home. In Greenville, I’ve helped many buyers who thought they couldn’t afford a home. With a co-borrower, they could.

When you don’t have enough income, a co-borrower can help. You can borrow more money and get better interest rates. This makes buying a home easier.

Explore innovative ways to make homeownership more affordable in House hacking first home guide for new buyers.

Understand Joint Tenancy Ownership Implications

Co-borrowing means you and your partner share the mortgage and property title. This means you both have to make payments and own the property equally.

Last year, I helped Sarah and her sister buy a $275,000 home. Sarah made $42,000 and her sister made $65,000. Together, they could afford it. Their combined income met the home’s requirements.

This helped them in three ways:

- They had a better debt-to-income ratio

- They could put down more money, lowering their mortgage insurance

- One partner’s better credit score got them a lower interest rate

Unlike other loans, co-borrowers don’t have to live in the house. For example, parents can help their kids buy a home without moving in.

Draft Co-Ownership Operating Agreement

Before you sign any mortgage papers, make a co-ownership agreement. It costs $500-800 but saves you from big problems later. I’ve seen agreements between family members fall apart when things get tough.

Your agreement should cover:

| Agreement Component | Key Questions to Address | Why It Matters |

|---|---|---|

| Payment Structure | Who pays what percentage of mortgage, taxes, and insurance? | Prevents confusion about monthly financial responsibilities |

| Maintenance Costs | How will repairs and improvements be funded? | Avoids disputes when unexpected expenses arise |

| Decision Authority | Who makes decisions about property changes? | Establishes clear process for renovations and modifications |

| Default Procedures | What happens if one party can’t make payments? | Protects both parties’ credit and investment |

| Occupancy Rights | Who lives in the property and under what conditions? | Clarifies living arrangements and possible rental income |

Get a real estate attorney to make your agreement. They’ll make sure it’s right for you. This is a big investment for your future.

Learn about the various grants and programs that can reduce upfront purchase barriers in Low income home buyer grants and programs reducing upfront purchase barriers.

Establish Exit Strategy for Partnership

Planning for when the partnership ends is key. Life changes can affect your needs or ability to keep the partnership.

Your exit plan should include:

- How to buy out the other partner

- How to split the equity

- When to review the partnership

- How to sell the property if you can’t agree

Programs like Fannie Mae’s HomeReady mortgage let non-occupant co-borrowers help. This means parents or relatives can help you qualify without living in the home. It’s a great option for those with lower credit scores or income.

The housing choice voucher and single family housing guaranteed loan programs also offer help. They have more flexible rules for co-borrowers and income.

Before you start, talk to a mortgage lender and real estate attorney. They’ll check if a co-borrower is right for you. They’ll also find the best mortgage options for your situation.

Remember, a co-borrower helps today but you should plan to refinance alone later. This way, you’ll own the home fully and free your co-borrower from their obligation.

Read also: Essential home buying budget checklist for new buyers.

Optimize Budget to Afford Repayments

Before you start, make sure you can afford it. Use the 28/36 rule. This means your housing costs should be less than 28% of your income. And your total debt payments should be under 36%.

If you make $40,000 a year, your housing costs can’t be more than $933 a month. This is important to know before you apply for pre-approval.

Knowing all the costs of buying a house is key. The down payment is just the start. Closing costs are 2-5% of the house price. You also need cash for the lender.

Read also:

Reduce Recurring Expenses Through Frugality Tactics

Start by checking your subscriptions. You might find $50-150 a month in savings. Call your service providers to get better deals. This can save you $30-50 a month.

Track your spending for a month. You might find ways to save $200+ on food. Or $100+ on gas by using different ways to get around.

Open a savings account just for housing costs. Put in your mortgage payment minus your rent each month. This helps you save for a down payment and shows you can handle the costs.

Being a homeowner means more than just a mortgage. You’ll need to budget for maintenance, property taxes, and insurance. These costs can be 1-3% of your home’s value each year. Making these budget changes can help you qualify for loans you thought you couldn’t get.

{kind=link}