Budgeting mistakes can stop your dream of owning a home fast. I’ve helped many new homeowners in Greenville for nine years. I see the same money mistakes over and over again.

Did you know 44% of Americans wish they knew more about the hidden costs of buying a before buying? “Planning months before seeing homes can make all the difference,” says Maria Sanchez, a housing counselor.

I recall a client who was upset when she found out her monthly payment was $400 more than she thought. She didn’t think about property taxes and insurance. This made me change how I help first-time buyers.

Quick hits:

- Create separate savings for closing costs

- Calculate true monthly payment including escrows

- Budget for post-purchase home maintenance expenses

- Get pre-approved before serious house hunting

Misjudging upfront home purchase costs

Many first-time home buyers only save for their down payment. They forget about thousands in extra costs. This narrow focus can ruin your homebuying plans at the worst time.

Recently, I talked to a young couple. They saved 3% for a $240,000 home. But they didn’t have the $7,200 for closing costs. Their dream home slipped away because they didn’t plan for all costs.

Buying a home means many upfront costs need planning. Your down payment is just the start. You’ll need more money when you buy a house.

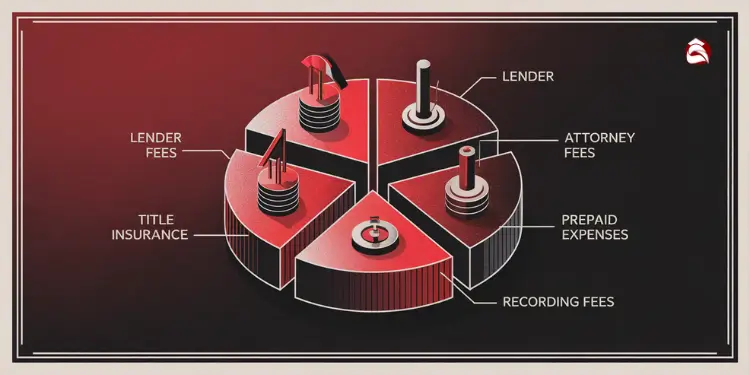

Underestimating Closing Fee Line Items

Closing costs are 2-5% of your loan amount. They cover many necessary services. These costs are not optional. They make sure your home purchase is legal and sound.

What are you paying for? Closing costs include:

- Lender fees (origination, application, and processing)

- Title insurance and title search

- Attorney fees

- Prepaid expenses (property taxes and homeowners insurance)

- Recording fees and transfer taxes

Set aside at least 3 % of the purchase price exclusively for closing costs; national data show buyer fees typically run 2 – 5 %. Ring-fencing this cash prevents last-minute funding gaps and safeguards your down-payment. Ref.: “Ortega, M. (2025). Closing Costs Explained: What Are Closing Costs and How Much Are They? Zillow.” [!]

I suggest saving for closing costs. Aim for 3% of your home price. This way, you won’t use your down payment for these costs.

“The most expensive mistake first-time buyers make isn’t overpaying for a house—it’s failing to budget for all the costs beyond the down payment.”

Forgetting Inspection Appraisal Contingency Funds

Smart buyers save for home inspection, appraisal, and repair negotiations. These costs are important before buying.

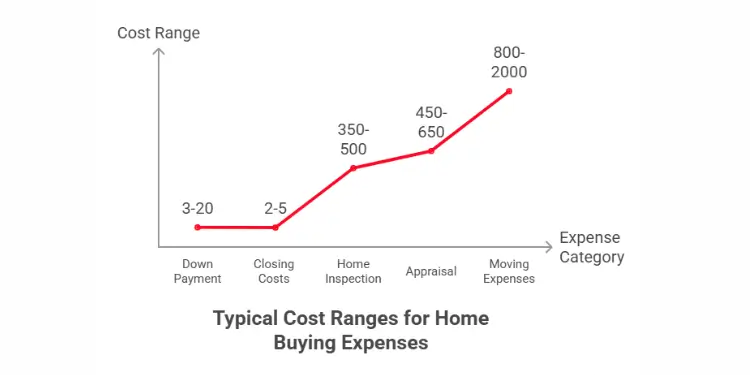

A home inspection costs $350-500. It’s a must for first-time buyers. It helps avoid costly problems later.

The appraisal costs $450-650. Your lender needs it to check the home’s value. You’ll pay it before closing.

Plan for a professional home-inspection fee of roughly $300 – $500; this range remains the industry norm in 2025 and is considered non-negotiable by most lenders and purchase contracts. Ref.: “Daugherty, G. (2025). How You Can Use a Home Inspection to Negotiate a Better Deal. Investopedia.” [!]

Don’t forget about contingency funds. These are for repairs after the inspection. Save $1,500-2,000 for this.

One client found $1,200 in electrical repairs during inspection. They had funds ready. They negotiated with the seller to split the cost.

I tell all my first-time buyers to make a detailed list of expenses. This includes:

| Expense Category | Typical Cost Range | When Due | Negotiable? |

|---|---|---|---|

| Down Payment | 3-20% of purchase price | At closing | No |

| Closing Costs | 2-5% of loan amount | At closing | Partially |

| Home Inspection | $350-500 | Before closing | No |

| Appraisal | $450-650 | Before closing | No |

| Moving Expenses | $800-2,000 | Around closing | Yes |

Good planning for upfront costs is key. It stops last-minute scrambles. Remember, budgeting for these costs is as important as finding a good mortgage rate.

Ignoring ongoing ownership expenses estimates

Many first-time buyers only think about the mortgage when figuring out how much house they can afford. They forget about the big ongoing costs. This can lead to a big surprise when these costs start coming in.

Getting a mortgage is just the start. Homeownership brings many costs that can affect your budget. Knowing these costs before buying helps avoid financial stress.

In my nine years helping buyers, I’ve learned a key rule. Add 40-50% to your mortgage payment for these costs. This helps my clients avoid being “house-poor” from common mistakes.

Property Taxes, Insurance and Maintenance Reality

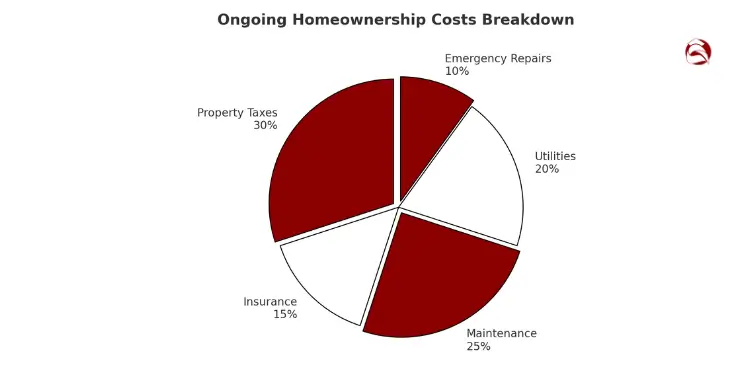

Property taxes are a big cost that goes up every year. In Greenville, they’re about 1.2% of your home’s value. For a $300,000 home, that’s $3,600 a year or $300 a month.

Greenville County’s effective property-tax rate averages 0.66 % of market value—higher than the South-Carolina median—and rises with reassessment. Omitting annual tax escalation can leave budgets short by hundreds of dollars per month. Ref.: “Tax-Rates.org Editorial Team. (2025). Greenville County, South Carolina Property Tax Rate 2025. Tax-Rates.org.” [!]

Homeowners insurance is also a must. Most pay $1,200-$1,800 a year for a standard policy. If your home is in a flood zone, you’ll pay more.

Utilities can surprise buyers moving from apartments. The bigger space means higher bills for:

- Electricity: $100-200 monthly

- Water and sewer: $40-80 monthly

- Natural gas: $30-100 monthly (seasonal)

- Waste services: $20-40 monthly

I tell my clients to ask utility companies about costs before making an offer. This gives them important budget info they often miss.

Home maintenance is often overlooked. Budget 1% of your home’s value annually for it. For a $300,000 home, that’s $3,000 a year or $250 a month.

| Maintenance Item | Typical Cost | Frequency | Annual Budget |

|---|---|---|---|

| HVAC Service | $150-300 | Twice yearly | $300-600 |

| Gutter Cleaning | $150 | 1-2 times yearly | $150-300 |

| Lawn Care | $50-200 | Monthly (seasonal) | $400-1,600 |

| Emergency Repairs | Varies | Unpredictable | $1,000-1,500 |

Don’t forget about hidden costs like pest prevention and air filters. These can add up fast.

Consumer-finance data indicate that setting aside 1 – 4 % of your home’s value annually—1 % for routine upkeep plus up to 3 % for unexpected repairs—aligns most closely with actual homeowner spending patterns and prevents deferred-maintenance shocks. Ref.: “Dehan, A. (2024). What Are the Most Common Home Maintenance Costs? Bankrate.” [!]

The best buyers set up a “home maintenance fund” with automatic monthly payments. This way, they’re ready for any unexpected repairs.

“The difference between homeowners who thrive and those who struggle often comes down to anticipating these ongoing expenses. When you budget realistically from day one, you avoid deferring maintenance that leads to costly major repairs down the road.”

Before making an offer, make a detailed monthly budget. This will show you can afford less house than you thought. It makes for a stress-free homeownership experience.

“Explore More: How to save money when buying house on budget”

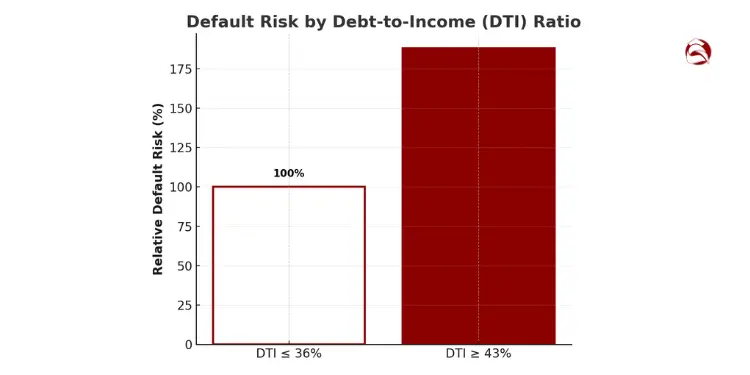

Overstretching debt to income ratios

Going too far with debt when buying a home is a big mistake. I’ve seen it happen many times. It can lead to big problems.

Lenders might say you can handle a high debt-to-income ratio. But that’s the max, not what’s best. I tell my clients to keep their housing costs under 28% of their income.

Let’s look at an example. If you make $70,000 a year, your max monthly payment should be $1,633. This includes your mortgage, taxes, and insurance. Going over this can make you “house poor.”

The house price to income ratio is key. It shows if buying a home is right for you. If it’s off balance, you’ll feel stressed.

Ignoring this rule can lead to trouble:

- You can’t save for emergencies.

- You might skip important home repairs.

- You could end up with credit card debt for everyday things.

- Retirement savings might suffer.

- Financial worries can ruin your life.

Before you start looking for a house, figure out how much you can afford each month. Don’t just look at the loan amount. This approach can save you a lot of stress.

I suggest a simple test for first-time buyers. Try living on the difference between your current housing costs and your new mortgage payment for three months. This test shows if you can really handle the higher payment.

If the higher payment is too tight, look into loans that help you own a home:

| Loan Type | Down Payment | Credit Score Minimum | Key Benefit |

|---|---|---|---|

| FHA Loan | 3.5% | 580 | Lower credit requirements |

| VA Loan | 0% | 620 (varies) | No down payment for eligible veterans |

| USDA Loan | 0% | 640 (typical) | Zero down for rural properties |

| Conventional | 3-20% | 620+ | Lower PMI with 20% down |

The FHA offers loans with only 3.5% down and a 580 credit score. VA loans let military members buy homes with no down payment. USDA loans also offer no-down-payment options for rural areas.

Buying a home that’s too expensive is risky. It can lead to foreclosure if you lose your job or get sick. A big mortgage payment leaves you with little money for other things.

The hardest talks I have are with buyers who can’t afford their loans. The joy of owning a home turns to stress when every month is a struggle.

Buying a home that fits your budget is more than just a property. It’s about keeping your financial freedom and peace of mind. This balance makes a house a true home.

“Related Topics: How to make home buying budget step by step”

Skipping professional financial guidance early

Many first-time home buyers skip getting professional financial advice. This mistake can ruin their dreams. In Greenville, I’ve seen many buyers fail because they didn’t plan well.

Getting pre-approved for a mortgage is just the start. Many think it’s enough to start looking for homes. But, it’s not enough to find the best loan or avoid financial trouble later.

Experts help you know how much house you can really afford. This is more than just what you can borrow. It’s about what you can afford to pay each month.

“Check This Out: Frugal home buying tips for budget conscious buyers”

Benefits of Fee-Only Housing Counselors

HUD-approved housing counselors offer free or low-cost advice. They don’t make money from your home purchase. This means they give you honest advice without bias.

These counselors check your finances and explain loan options. They also find programs that can save you money. Many clients have found programs that cut their down payment in half.

HUD’s evaluation of 18,000 loans shows buyers who completed pre-purchase housing counseling were 33 % less likely to become 90-day-delinquent within two years, dramatically boosting long-term homeownership sustainability. Ref.: “Mayer, N. & Temkin, K. (2013). NeighborWorks Pre-Purchase Counseling Impact Study. U.S. Department of Housing and Urban Development.” [!]

Working with a housing counselor was the best decision we made. They found us a first-time homebuyer program that covered half our down payment and helped us understand the true costs of homeownership. Without their guidance, we would have overextended ourselves financially.

First-time buyers who work with counselors are 30% less likely to face foreclosure. This shows how valuable they are. They help you:

- Create a budget for housing costs

- Improve your credit score for better rates

- Find and apply for homebuyer programs

- Choose the right mortgage for you

- Get ready for loan approval

I suggest meeting with counselors 6-12 months before house hunting. This gives you time to improve your credit or save money.

“For More Information: How to stick to home buying budget without fail”

Comparing Lender Preapproval Scenarios Thoroughly

Don’t settle for the first lender who pre-approves you. Being a serious buyer means having solid financing. Compare different lenders to find the best deal.

Compare at least three lenders’ offers on the same day. Look at interest rates, fees, loan terms, and down payment requirements. A small difference in interest rate can save a lot of money over time.

Ask lenders to show you different down payment and loan scenarios. This helps you find the best financing for your situation. When deciding between a starter home or a forever home, these scenarios are key to planning your finances.

| Lender Scenario | Down Payment | Interest Rate | Monthly Payment | Total Cost (30 years) |

|---|---|---|---|---|

| Conventional 30-year | 20% ($60,000) | 6.5% | $1,517 | $546,120 |

| Conventional 30-year | 10% ($30,000) | 6.75% | $1,751 | $630,360 |

| FHA 30-year | 3.5% ($10,500) | 6.25% | $1,852 | $666,720 |

| VA Loan (if eligible) | 0% ($0) | 6.0% | $1,799 | $647,640 |

Note: Table based on a $300,000 home price. Monthly payments include principal, interest, taxes, and insurance estimates. Actual rates and costs will vary.

The table shows how different loans affect your costs. Many buyers focus only on down payments without thinking about the long-term costs.

When comparing lenders, ask about closing times and communication. A lender who can close quickly and talks well with sellers’ agents can help you win a home.

Remember, pre-approval letters expire after 60-90 days. If you’re looking for a long time, you’ll need to get re-approved. This is why it’s good to start with a lender early.

Getting financial advice early makes you a better buyer. It helps you avoid mistakes and gives you a strong position when you find the right home.

“Read More:

Relying on unstable future income projections

Buying your first home can be tricky. Using income that hasn’t arrived yet is risky. I’ve seen buyers plan for money that never comes.

28% of first-time buyers in 2024 faced financial trouble. This was because they based their budget on income they thought would come. But it didn’t.

When figuring out how much house you can buy, only use your current income. Lenders look at your income from the past two years if you’re self-employed. Job changes can also affect approval, even if you make a lot.

Save six months’ worth of housing costs before buying. This fund helps when income is less than expected or when repairs pop up.

I’ve helped clients wait to buy when their income was unsure. They all said thanks later. The smartest first-time buyers plan for their lowest income, not the highest.

Buying a home means you need to be financially stable for a long time. The right home is joyful when you can really afford it. But rushing because of income hopes can turn your dream into a financial problem.

{kind=link}