The 50/30/20 budget calculator makes managing your money easy. It uses just three simple percentages. This way, you split your after-tax income into three parts: needs (50%), wants (30%), and savings (20%).

Many Americans have trouble with money, even when they earn well. The Federal Reserve says almost 40% of adults can’t handle a $400 emergency without borrowing.

Financial advisor Suze Orman says, “A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” I used this budget method and felt less worried about money in just two months.

Planning your finances doesn’t need complicated spreadsheets or accounting degrees. It just needs a simple plan that balances today and tomorrow.

Quick hits:

- Simplifies complex financial decisions instantly

- Works with any income level

- Eliminates guilt around personal spending

- Creates automatic savings habit patterns

- Reduces financial stress significantly

How the calculator breaks down percentages

The 50/30/20 calculator is simple. It divides your money into three parts for better money management. This makes budgeting easy for everyone, no matter their money knowledge.

When you put in your monthly income, the calculator shows how much for each part. This way, you can avoid spending too much and save enough.

Needs Wants Savings Formula Overview

The 50/30/20 rule splits your money into three parts:

- 50% for Needs – These are things you must have. This includes your home, food, and insurance.

- 30% for Wants – These are things that make life better but aren’t needed. This includes fun activities and shopping.

- 20% for Savings – This is for saving money for the future. It includes your emergency fund and retirement.

Let’s say you make $3,000 a month. The calculator would split it like this:

- Needs: $1,500 (50% of $3,000)

- Wants: $900 (30% of $3,000)

- Savings: $600 (20% of $3,000)

Nearly 50 percent of U.S. renter households already spend more than 30 percent of income on housing, and millions are “severely cost-burdened” at 50 percent or more. In high-rent markets you may need to raise the “Needs” cap temporarily while pursuing cost-reduction or income-boosting tactics. Ref.: “U.S. Census Bureau. (2024). Nearly Half of Renter Households Are Cost-Burdened. News Release CB24-150.” [!]

This makes it easy to see if you’re spending too much. If your bills are more than $1,500, you might need to cut costs.

The beauty of the 50/30/20 approach lies in its simplicity. Instead of tracking dozens of individual expenses, you focus on just three big-picture categories that keep your financial life in balance.

Personal-finance researchers credit the rule’s enduring popularity to its low “decision cost”: simple percentage cues reduce cognitive load and improve first-time budget adherence compared with line-item tracking. Ref.: “White, M. C. (2024). Why a 60/30/10 Budget Could Be the New 50/30/20. TIME.” [!]

Comparison with Zero Based Tools

The 50/30/20 rule is different from zero-based budgeting. Knowing the difference helps you pick the best budgeting method for you.

| Feature | 50/30/20 Calculator | Zero-Based Budgeting |

|---|---|---|

| Core Principle | Allocates income by percentages into three categories | Assigns every dollar a specific job until income minus expenses equals zero |

| Detail Level | High-level category tracking | Detailed tracking of individual expenses |

| Time Investment | Minimal setup and maintenance | Requires regular detailed tracking and adjustments |

| Best For | Beginners and those who prefer simplicity | Detail-oriented people who want maximum control |

The 50/30/20 calculator is easy to use and doesn’t need much work. You don’t have to track every little thing you buy. Just stick to the three main categories.

Zero-based budgeting, on the other hand, tracks every dollar. It’s more precise but takes a lot of time and detail. Many start with 50/30/20 and move to zero-based as they get better at managing money.

The 50/30/20 calculator also adjusts when your income changes. If you get a raise, it shows how much more you can spend or save. You don’t have to change your whole budget.

For beginners, the 50/30/20 calculator is a great start. It’s easy to follow and helps you build a strong financial base. As you learn more, you can add more details to your budget.

Input fields you need to gather

Planning your budget starts with the right financial data. You need specific numbers for the 50/30/20 calculator to work well. Knowing these numbers helps you divide your money wisely.

Monthly Take Home Income Figure

Your take home pay is the base of your budget. It’s the money you get after taxes and other deductions. This is different from your gross income.

To find your take home pay, look at your latest pay stub. Find the “net pay” amount. If you get paid more than once a month, add those amounts together.

If your income changes, use the last three to six months to find your average. This gives a better budget baseline.

“Understanding the difference between gross and net income is key. Your budget should be based on what you can spend, not what you earn.”

If you’re self-employed or have many income sources, include all your earnings. Remember to set aside money for taxes. The 50/30/20 calculator needs your full financial picture.

Typical Bills and Variable Expenses

Next, list your monthly expenses. These are fixed bills and variable costs. Fixed costs stay the same, while variable costs change.

First, list your fixed expenses:

- Housing (rent or mortgage)

- Utilities (electricity, water, gas, internet)

- Insurance premiums (health, auto, home)

- Loan payments (student loans, car payments)

- Minimum debt payments (credit cards, personal loans)

Then, track your variable expenses:

- Groceries and household needs

- Transportation costs (gas, public transit)

- Healthcare not covered by insurance

- Childcare or dependent care costs

Look at your bank and credit card statements from the last three months. This helps you find your average spending. Many apps can help categorize your expenses.

Make sure to separate your necessary expenses from things you want but don’t need. Knowing how the 50/30/20 budget works helps you sort your expenses right.

Use a simple spreadsheet to organize your expenses. This makes it easier to enter numbers into the calculator later.

Be honest and thorough when collecting your expense data. If you underestimate, you might overspend. If you overestimate, you might feel stressed. Your goal is to reflect your real financial situation.

With your income and expenses ready, you can use the calculator. It will show if your spending matches the 50/30/20 rule.

Interpreting results for smart decisions

The 50/30/20 budget calculator is more than just numbers. It shows you how to balance your money. Seeing those percentages is like getting a map to financial health.

Let’s talk about what each percentage means. The “needs” category (50%) is for things you must have. This includes your home, food, and bills. If you spend more than 50% here, you might be in trouble.

The “wants” part (30%) is for fun stuff. This is for eating out, movies, and things you don’t really need. It’s where you enjoy life.

The “savings” part (20%) is for your future. It’s for saving for emergencies, retirement, and paying off debt. This helps you secure your future.

Spotting Imbalances

If you’re spending too much on needs, don’t worry. It’s a chance to make smart changes. Here are some ideas:

- Downsize housing if rent/mortgage consumes too much income

- Refinance high-interest debt to lower monthly payments

- Negotiate bills or find more affordable alternatives

- Increase income through side work or career advancement

Life situations can change your budget needs. Families need more money than singles. High-cost places like San Francisco might make your needs higher too.

Set goals based on your real situation. If you’re at 65/30/5, aim for 60/25/15 first. This is a step toward 50/30/20.

“Discover More: Should I use 50/30/20 budget or another budgeting method“

Prioritizing Your Adjustments

First, build a small emergency fund. Even $1,000 can help a lot. Then, pay off high-interest debt.

If you spend too much on wants, cut back. Find things you can live without. Sometimes, we spend on things that don’t make us happy.

The 50/30/20 rule is a guide, not a rule. Your budget should fit your life. The best budget is one you can keep up with.

“Learn More About: 50/30/20 budget for college students easy campus money management plan“

Taking Action Based on Results

Based on your calculator, here’s what to do:

- High debt obligations: Create a debt snowball or avalanche repayment plan

- Low savings percentage: Automate transfers to your emergency fund

- Excessive needs: Review fixed expenses for possible cuts

- Inflated wants: Track spending for a month to find patterns

Large-scale studies show default automatic enrollment and auto-escalation policies lift average savings rates, even after employee turnover, by roughly 0.5–0.7 percent of income per year — a small but measurable compounding boost when automation is in place. Ref.: “Choi, J. J. & Laibson, D. (2023). Do Automatic Savings Policies Actually Increase Savings? NBER Working Paper.” [!]

Check your calculator every quarter. It helps you see how you’re doing. With regular checks, you’ll get closer to the balance you need.

Customizing percentages for personal goals

Your financial journey is unique. Our budget calculator lets you adjust percentages to fit your goals. The 50/30/20 rule is a good start, but you might need something different.

Financial success is not one-size-fits-all. Your income, location, family size, and goals affect your budget. Our calculator helps you create a budget that’s just right for you.

“Further Reading: 50/30/20 budget example for a typical monthly income“

Adjusting Sliders for Unique Priorities

The interactive sliders in our calculator let you change the 50/30/20 percentages. If you live in San Francisco or New York, you might need to spend more on housing. If you have big medical bills, our calculator can help you reflect that.

Here are some examples of when you might need to adjust your budget:

- High-cost living areas might require a 60/30/10 budget split

- Young professionals with lower bills could shift to a 40/30/30 ratio to boost savings

- Parents with growing families might need a 55/25/20 breakdown

- Those tackling debt could benefit from a 50/20/30 approach, with the extra 10% toward repayment

The best budget isn’t the one that follows a rigid formula – it’s the one that helps you sleep at night while moving you toward your goals.

As you adjust the sliders, the calculator shows how it changes each category. This helps you find the right balance for your unique priorities.

“Related Topics: How to make 50/30/20 budget with clear practical step by step“

Saving More Than Standard Twenty

While the traditional rule allocates 20% to savings and debt repayment, many experts now recommend saving more. Our calculator makes it easy to increase this percentage to help you reach financial independence faster.

Here are ways to boost your savings beyond the standard 20%:

- Temporarily reduce your “wants” category to 20% and increase savings to 30% when saving for a specific goal like a home down payment

- Allocate additional income from bonuses or tax refunds entirely to savings

- Gradually increase your savings rate by 1% every few months until you reach your target

- Direct any debt payment amounts to savings accounts once the debts are paid off

When you have high-interest debt, consider paying more than the minimum. The calculator shows how this can save you money on interest over time.

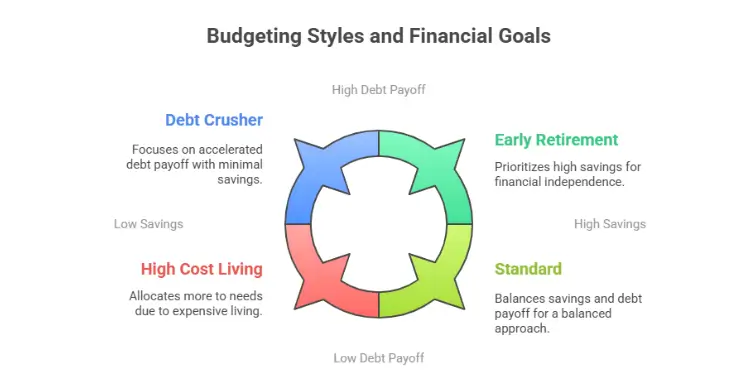

| Budget Style | Needs % | Wants % | Savings % | Best For |

|---|---|---|---|---|

| Standard | 50% | 30% | 20% | Balanced approach |

| High Cost Living | 60% | 30% | 10% | Expensive cities |

| Debt Crusher | 50% | 20% | 30% | Accelerated debt payoff |

| Early Retirement | 40% | 20% | 40% | Financial independence |

Your savings strategy should change as your financial situation does. You might start with an emergency fund, then move to retirement contributions, and later to investment accounts.

The beauty of our calculator is that it grows with you. As your income or goals change, you can adjust your percentages. The framework stays the same, but the numbers change to fit your life’s chapter.

“Read More: 50/30/20 budget breakdown of needs, wants, and savings“

Common mistakes to avoid when entering

Starting with the right data is key to good budgeting. But, many people struggle with budget calculators. Even the best tools can’t help if the info is wrong. Let’s look at common mistakes and how to avoid them for better budgeting.

One big mistake is forgetting about irregular costs. Things like insurance, taxes, and holiday gifts don’t show up monthly. But they really affect your money. To fix this, divide your yearly costs by 12 and add it to your monthly budget.

Creating dedicated “sinking funds” for predictable yet irregular expenses (insurance renewals, holidays, tuition) prevents emergency-fund raids and high-interest borrowing when those bills arrive. Ref.: “Barroso, A. (2022). Get on Top of Planned Expenses With Sinking Funds. NerdWallet.” [!]

For example, if you pay $1,200 a year for insurance, add $100 each month. This way, you won’t be surprised by big expenses.

Another mistake is mixing wants with needs. The 50/30/20 rule is flexible, but knowing what’s a need and what’s a want is important. A basic phone plan is a need, but a new phone every year is a want.

Basic food is a need, but fancy brands are wants. Be clear about what you’re spending on. This helps keep your budget real.

“The difference between successful people and really successful people is that really successful people say no to almost everything.” – Warren Buffett

Another mistake is counting the same expense twice. If you list your mortgage payment, don’t also list the parts of it. This makes your budget look worse than it is.

Many people use their gross income instead of after-tax income. But the 50/30/20 rule needs your after-tax income. Using your pre-tax income makes your budget too high.

To get your after-tax income, start with your take-home pay. If you have variable income, average it out after taxes.

Underestimating variable costs is also a problem. Things like food and entertainment often cost more than we think. Look at your past spending to find better estimates.

For example, if you spent $400, $480, and $520 on groceries, use $467 as your monthly cost. Don’t aim for $350 if that’s not realistic.

It’s tempting to dream big with your budget. But being too optimistic won’t help. Your budget calculator needs real numbers to guide you.

Some forget to include savings goals beyond twenty percent. If you’re saving for a big purchase or following zero-budgeting vs. percentage budgeting, include these in your budget.

Lastly, not updating your budget can make it outdated. Big changes like a new job or moving can change your income and expenses. Check your budget regularly to keep it current.

Remember, making these mistakes can be frustrating. But, it’s all part of learning. With practice, your budget calculator will help you reach your financial goals.

“For More Information:

Downloadable sheet and mobile version links

Want to use the 50/30/20 budget more? I’ve made free Excel and Google Sheets templates for you. They help you budget easily and save your progress. This way, you can see how close you are to your financial goals.

Need to budget on the go? Many mobile apps have 50/30/20 features. Mint is free and tracks your money automatically. YNAB costs $14.99 a month but lets you customize more. NerdWallet’s app also helps with budgeting and checks your credit score.

Like to use paper? Our PDF worksheets let you budget without a screen. Many people find it helps them stick to their budget better.

Find the best way to budget for you. Even the best calculator won’t help if you don’t use it. Emma, a workshop student, used our basic spreadsheet last year. She tracked her spending and paid off $5,800 in debt. She also started saving for emergencies.

Get the right tools to manage your money. Download what you like below and start now.

{kind=link}