Your paycheck shouldn’t just disappear. The right financial plan makes you feel sure about your money.

Do you think you need to track every dollar to be financially successful? According to the American Psychological Association’s 2014 ‘Stress in America’ survey, 72% of adults reported feeling stressed about money at least some of the time.

“Financial freedom isn’t about having more money—it’s about controlling the money you have,” says Ramsey Smith, a top financial advisor.

I changed my money habits and it helped a lot. In just 11 months, I paid off $8,000 in credit card debt that had been a big worry for years.

The big difference is in how you approach money. A zero-based budget gives every dollar a job until there’s nothing left. On the other hand, priority based budgeting puts your most important goals first, then uses what’s left.

Neither way is better for everyone. By the end of this article, you’ll know which personal finance plan fits you best.

- Comparing Zero-Based and Priority-Based Budgeting Methods

- Your personality type affects which method works best

- How well you use the method is more important than the method itself

- The right plan can help you pay off debt and grow your wealth faster

Establishing Financial Priorities Before Choosing a Budgeting Method

Knowing what you spend money on first is key to picking the right budgeting method. Many friends start with complex systems but give up soon. They didn’t know what was important to them financially.

Zero budgeting and priority-based budgeting need you to know your financial values first. This is like building a foundation for your budget. Without it, even the best systems won’t work.

I tried budgeting three times before getting it right. I focused on tools instead of my goals. Once I knew what mattered, budgeting became easier.

Prioritizing Financial Goals Based on Emotional Significance and Urgency

Not all financial goals are the same. You need to rank them by how important they are to you and how urgent they are.

Emotional importance is how much you care about a goal. Think about what keeps you up at night. Rate each goal from 1 to 5, with 5 being the most important.

Objective urgency is about deadlines and costs. Goals with deadlines or penalties are more urgent. Use the same 1 to 5 scale for urgency.

| Financial Goal | Emotional Importance (1-5) | Objective Urgency (1-5) | Total Score | Priority Rank |

|---|---|---|---|---|

| Emergency Fund | 4 | 5 | 9 | 1 |

| Credit Card Debt | 5 | 4 | 9 | 2 |

| Home Down Payment | 4 | 2 | 6 | 3 |

| Vacation Fund | 3 | 1 | 4 | 4 |

Add these scores to find out which goals to fund first. This makes a budget that fits your life, not someone else’s idea.

STATISTICAL EVIDENCE:

Prioritizing financial goals based on emotional importance and urgency can lead to more effective budgeting. A study by the American Psychological Association found that 72% of adults reported feeling stressed about money at least some of the time, highlighting the need for personalized financial planning to alleviate stress. Ref.: “APA survey shows money stress weighing on Americans’ health nationwide. American Psychological Association.” [!]

I was trying to save for retirement, a house, and travel at the same time. But my big worry was not having an emergency fund. I saved most for that first, and my stress went down a lot in three months.

Differentiate Non-Negotiable Expenses From Lifestyle Perks

It’s also important to know the difference between needs and wants. This is the core of good budget planning, no matter the system.

Needs include housing, utilities, and food. These must be paid first.

Wants, like daily coffee, might feel like needs but aren’t. I thought my coffee was essential until I saw how much it cost. It could have filled my emergency fund sooner.

Try this: Imagine not spending on something for 30 days. If it’s hard, it’s a need. If not, it’s a want.

- Non-negotiable: Basic internet service needed for work

- Lifestyle perk: Premium high-speed package for streaming

- Non-negotiable: Grocery budget for home-cooked meals

- Lifestyle perk: Regular takeout or restaurant dining

- Non-negotiable: Basic cell phone plan for essential communication

- Lifestyle perk: Latest smartphone upgrade every year

Knowing what’s essential helps any budget system work better. With zero budgeting, you focus on needs first. With priority-based budgeting, you make sure needs are met before other goals.

Figuring out your financial priorities is very rewarding. When unexpected things happen, you’ll make better choices.

Whether you choose zero budgeting, priority-based budgeting, or something else, this groundwork is key. The best budget is one that supports your goals, not the other way around.

Distinguishing between needs and wants is crucial in budgeting, yet many individuals struggle with this differentiation. The 50/30/20 budgeting rule, popularized by Senator Elizabeth Warren, allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. However, due to rising living costs, some experts suggest adjusting these percentages to better fit individual circumstances.. Ref.: “Budgeting Methods | Examples, Implementation, Pros, & Cons. Finance Strategists.” [!]

How priority budgeting channels funds toward highest value goals first

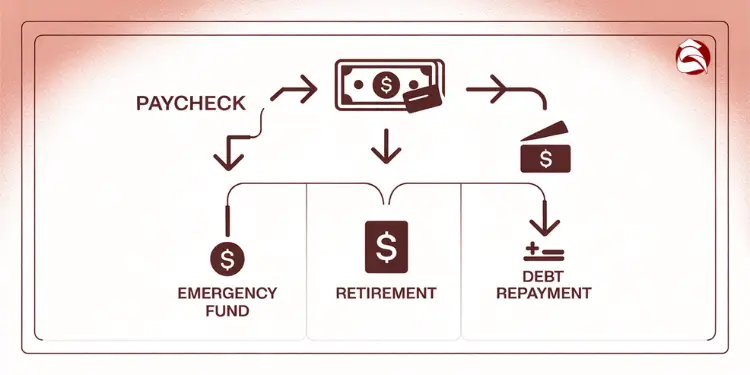

Priority-based budgeting emphasizes funding your top financial goals first, such as savings or debt repayment, before covering other expenses. It’s like saying, “Pay yourself first” before spending on everyday things. This way, your big dreams don’t get ignored by daily costs.

With old budgeting ways, dreams like saving for retirement often get pushed back. People mean to save, but the money goes elsewhere. Priority budgeting changes this by putting goals first.

First, decide how much of your income to use for your top goals. Then, use what’s left for bills and fun stuff. This makes your money match your values.

Automatic Transfers Lock in Savings Momentum Early

Priority budgeting’s secret is automation. Set up automatic transfers right after payday. This way, your goals get money without you having to remember.

Here’s how to start:

- Choose your top 3-5 financial goals (like saving for retirement).

- Decide how much money each goal needs.

- Make automatic transfers happen soon after you get paid.

- Use separate accounts for each goal to keep money separate.

Even modest automatic transfers can accumulate significantly over time; for instance, saving $50 per paycheck amounts to $1,200 annually.

I’ve seen people change their financial lives with this method. One family saved $25 a week for a vacation. After 18 months, they had enough for a debt-free trip.

| Priority Goal | Suggested Transfer Timing | Minimum Effective Amount | Annual Impact |

|---|---|---|---|

| Emergency Fund | Day after payday | $25-50 per paycheck | $600-$1,200 |

| Retirement | Same day as paycheck | 5% of gross income | Varies by income |

| Debt Payoff | 2-3 days after payday | $100 per month | $1,200 + saved interest |

| Major Purchase | Weekly small transfers | $20 per week | $1,040 |

Ongoing Reviews Adjust Goal Funding When Life Shifts

Priority budgeting is flexible for life’s changes. Automated transfers keep things steady, but regular checks let you adjust as needed.

Life changes, and so should your budget. You might get a raise or have a new baby. Priority budgeting lets you adjust your savings plan as life changes.

When you review your budget, ask yourself these questions:

- Have your priorities changed?

- Is your savings right for your income and expenses now?

- Do you need to add or remove goals?

These reviews might mean more savings after a raise or less during emergencies. You can also move money to new goals when old ones are done.

This flexibility makes priority budgeting work for the long haul. It’s better than strict budgets that fail when life gets busy.

Priority budgeting is not just about money. It’s about feeling less stressed and more secure about your future.

Priority budgeting is simple. You don’t have to track every penny. Just make sure your big goals get money first, then manage the rest easily. This fits well with busy lives.

Zero budgeting demands detailed tracking for heightened daily awareness

Zero-based budgeting involves allocating every dollar of income to specific expenses, savings, or debt payments, ensuring no funds are left unassigned, savings, or debt payments, ensuring no funds are left unallocated. It helps you see where your money goes. This way, you know exactly how much you spend.

At first, I thought it was hard to assign every dollar a job. But it’s really about managing your money well. Dave Ramsey says, “A budget is telling your money where to go instead of wondering where it went.”

Start with your income for the period. Then, divide it into categories until you reach zero. This doesn’t mean spending all your money. Some goes to savings and a safety net.

“read also: What is zero budget envelope for organized cash storage“

Category Balances Highlight Overspending In Real Time

Zero-based budgeting shows you how much you spend in real time. You set limits for things like food and entertainment. This helps you make better choices.

Last month, I saw my dining out money drop to $35. This made me cook more. I saved $120 for my vacation.

To track your spending, use tools like budget apps or spreadsheets. Here are some good ones:

- Budget apps: YNAB (You Need A Budget) and EveryDollar are great

- Spreadsheet templates: Excel or Google Sheets are customizable

- Envelope system: Use cash in labeled envelopes for limits

- Banking apps: Some banks track spending for you

Choose a system that’s easy to use. This way, you’ll see where you’re spending too much right away.

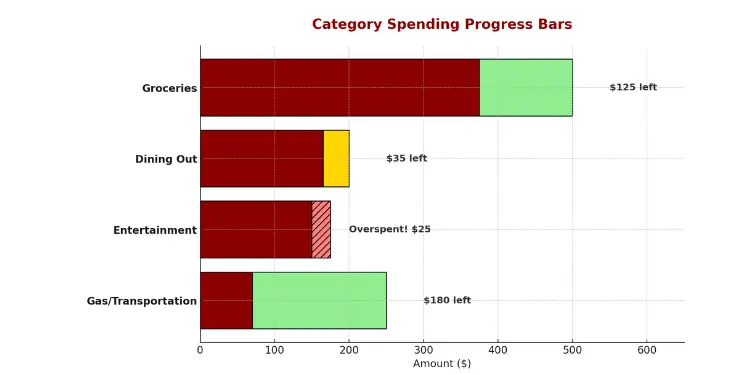

| Category | Monthly Budget | Current Balance | Action Needed |

|---|---|---|---|

| Groceries | $500 | $125 | On track |

| Dining Out | $200 | $35 | Caution needed |

| Entertainment | $150 | -$25 | Overspent! Adjust now |

| Gas/Transportation | $250 | $180 | On track |

Weekly Reconciliation Catches Subscription Creep Rapidly

Weekly reviews are key in zero-based budgeting. They help you stay on track. This way, you catch problems early.

Subscription creep is a big money drain. Small charges add up. A $9.99 service here, a $4.99 app there, and you’re spending a lot.

Here’s a simple 5-step process to save money:

- Schedule a weekly review (Sunday evenings work well)

- Check all transactions from the past week

- Categorize any spending that wasn’t planned

- Compare your spending to your plan

- Adjust your spending for the next week

One client found a $14.99 meal planning app she didn’t use. Another’s music service went up to $14.99 without notice. These changes are clear when you review weekly.

“Zero-based budgeting is justified for each new period. It’s not about restriction—it’s about awareness. When you know where every dollar goes, you gain the power to make intentional choices.”

Zero-based budgeting takes more time than other methods. But it’s worth it for the clarity it brings. It can change how you view money.

Consider experimenting with zero-based budgeting for a month to assess its effectiveness for your financial situation.

Managing debt repayments seamlessly within both budgeting systems

Debt repayment success comes from using payoff strategies well. No matter your budgeting choice, paying off high-interest debt is key. Both zero-based and priority budgeting can help you get out of debt faster.

I had $12,000 in credit card debt for years. But after using a consistent repayment plan, I paid it off. The right strategy can help you control your money and reduce what you owe.

Snowball Strategy Pairs Naturally With Priority Funding

The debt snowball method works great with priority budgeting. It pays minimums on all debts and extra on the smallest first. Once that’s paid, you use that money for the next smallest debt.

Priority budgeting is perfect for this because it focuses on important goals first. Here’s how to use the snowball method with priority budgeting:

- List all debts from smallest to largest balance

- Set up automatic minimum payments for every debt

- Create a separate automatic transfer for your “snowball” amount

- Direct this extra payment to your smallest debt until it’s eliminated

- Move to the next debt, adding the previous debt’s payment amount

Using this method to pay off my credit card debt took 18 months. The small wins kept me going. Seeing debts disappear gave me the motivation to tackle bigger ones.

Priority budgeting supports this strategy because it ranks goals by importance. Making debt elimination a top priority means you fund it first, before spending on wants.

“The debt snowball has helped me pay off $37,000 in just two years. Seeing those smaller debts disappear one by one kept me going when I wanted to give up.”

Avalanche Method Integrates Easily In Zero Budget Categories

The debt avalanche method focuses on the highest-interest debt first. This saves you money on interest over time, but it may take longer to see each debt paid off.

Zero-based budgeting is great for the avalanche method because it tracks every category. This helps you find money to put toward debt each month.

To use the avalanche method with zero budgeting:

- Create specific categories for each debt in your budget

- Allocate minimum payment amounts to each debt category

- Identify your highest interest debt as your primary target

- Assign all additional available funds to this target debt

- Once paid off, redirect those funds to the next highest interest debt

Zero budgeting helps you find extra money for debt repayment. By tracking every dollar, you can often find funds to pay off high-interest debt faster.

This method also lets you see interest savings in real-time. Watching your savings grow each month can be very motivating.

| Feature | Snowball Method | Avalanche Method | Best Budgeting Match |

|---|---|---|---|

| Primary Focus | Smallest balance first | Highest interest rate first | Both work with either system |

| Psychological Benefit | Quick wins and momentum | Mathematical optimization | Snowball: Priority Budgeting |

| Financial Benefit | Motivation to continue | Lower total interest paid | Avalanche: Zero Budgeting |

| Implementation Ease | Simple to track progress | Requires interest rate tracking | Depends on personal preference |

Consistency is key to debt repayment success. Choose a strategy you can stick with every month. Both budgeting systems offer valuable tools to help you stay on track.

For those using the avalanche method, I’ve made a simple spreadsheet. It shows interest savings as you go, keeping you motivated.

Those who integrate their debt strategy with their budget are more likely to become debt-free. Budgeting gives you structure and accountability, even when expenses pop up.

Paying off debt is more than just numbers. It’s about creating a system that fits your life. Choose a method you can keep up with until you’re debt-free.

Comparing long term sustainability when lifestyle changes arise

Traditional financial advice doesn’t work when life changes a lot. Zero and priority budgeting must show they’re good during big changes. It’s not just about being good when things are steady. It’s about being great when life changes a lot.

Handling New Child Expenses Without Derailing Goals

Having a new child is a big test for your budget. You need to change how you spend money to keep reaching your goals.

Zero budgeting means making new categories for child costs. You’ll need to decide which old categories to cut back on. This helps you see where every dollar goes.

But, making these changes takes time. You might feel rushed when you’re already busy.

Priority budgeting is different. It lets you keep your main goals while adding new expenses. This way, you can adjust without losing focus.

My neighbor Sarah did this. She cut her retirement savings to 5% when her daughter was born. Then, she slowly went back to 15% as costs went down.

| Budgeting Approach | Strengths During Child Transition | Challenges During Child Transition | Time Investment |

|---|---|---|---|

| Zero Budgeting | Detailed tracking of new expenses | Complete budget overhaul required | High (3-5 hours monthly) |

| Priority Budgeting | Maintains core financial goals | Less detailed expense tracking | Low (1-2 hours monthly) |

| Traditional Budgeting | Familiar and simple | Often abandoned during transitions | Medium (2-3 hours monthly) |

Adapting to Income Increases and Avoiding Lifestyle Inflation

Getting a raise is a challenge. It’s easy to spend more and lose money. Budgeting is key to keeping your money safe.

Zero budgeting makes you think about where extra money goes. You decide how to use extra dollars. This stops you from spending more without thinking.

It’s like asking if you should save for a vacation or pay off debt. This way, you avoid spending too much.

Priority budgeting is different. It helps you save more of your raise for important goals. This way, you make progress faster.

I save 50% of my raises for retirement and debt. This lets me enjoy some new things while saving more. In three years, I paid off $18,000 in loans and upgraded my home.

Some employers help by splitting your paycheck automatically. This is great for saving more as you earn more.

“The most powerful wealth-building tool is the gap between your income and your lifestyle. Protecting and expanding that gap when your income rises determines your financial trajectory.” – Jonathan Mendonsa, ChooseFI

Priority budgeting might be better for big life changes. It’s simple and keeps your financial goals in mind. It’s easy to adjust during stressful times.

Zero budgeting gives you more control if you like knowing where every dollar goes. It’s good for those who want detailed control during changes.

The most effective budget is one that remains sustainable and adaptable during life’s challenges. For many, that’s priority budgeting with some zero budgeting. It’s about finding what works for you.

Action plan to trial both methods over four pay cycles

Ready to find your perfect budgeting match? Try both zero-based and priority-based budgeting for four pay cycles. Many business leaders use zero-based budgeting. Others prefer priority systems that match spending with community needs.

Track stress levels and time commitment side by side

Make a simple weekly check-in sheet. Rate your financial anxiety (1-5), record minutes spent on budget tasks, and note your confidence level about money decisions. These personal metrics often predict which system you’ll stick with long-term better than financial numbers alone.

Read More:

Decide final framework using tangible progress metrics

After testing both approaches, evaluate concrete results. Track percentage of income saved, debt reduction amount, progress toward specific goals, and overspending incidents. Unlike the traditional budgeting process that focuses solely on increases or decreases, this comparison reveals which system delivers meaningful progress on your priorities.

Remember, the best budget isn’t the one that saves the most. It’s the one you’ll actually use consistently. Many people find a hybrid approach works best. It combines priority-based automatic transfers for major goals with zero-based tracking for daily spending. Your budget should serve your life, not the other way around.

{kind=link}